You've probably heard the term "adjustable rate mortgage" and wondered is this something I should actually consider, or is it too risky? Maybe your mortgage lender mentioned it during a refinancing conversation, or you've seen lower rates advertised and wondered what the catch is. Those are fair questions, and you're not alone in asking them.

As a licensed mortgage advisor with over a decade of experience helping homeowners across the country refinance smarter and make the most of their home equity, I've seen ARMs work beautifully for some borrowers and cause real stress for others who didn't fully understand how they worked going in.

This guide will walk you through exactly how an adjustable rate mortgage works, when it could genuinely save you money, what the risks look like in real life, and how to decide if it fits your situation whether you're refinancing, tapping your home equity, or buying for the first time.

What Is an Adjustable Rate Mortgage (ARM)?

An adjustable rate mortgage is a home loan that starts with a fixed interest rate for a set number of years then adjusts periodically based on what's happening in the broader market.

Think of it this way: with a fixed-rate mortgage, your rate is locked in for the life of the loan. With an ARM, you get that same stability upfront, but after the initial fixed period ends, your rate can go up or down depending on market conditions.

That initial period is where the naming comes from. A 5/1 ARM means your rate is fixed for 5 years, then adjusts once every year after that. A 7/1 ARM gives you 7 years of stability. A 10/1 ARM gives you 10.

When the adjustment kicks in, your lender calculates your new rate using two things: a benchmark rate called SOFR (the Secured Overnight Financing Rate the standard index used by most lenders today) plus a lender margin, which is a fixed percentage your lender adds on top. Togetheinterest rate capsr, those two numbers make up your new rate.

The good news? There are built-in limits called on how much your rate can move at any one time, which we'll cover in the next section.

How Does an ARM Loan Work? The Adjustment Mechanics Explained

Understanding ARM Loan Structures (5/1, 7/1, 10/1)

The numbers in an ARM's name tell you everything you need to know. The first number is how many years your rate stays fixed. The second number is how often it adjusts after that.

So a 7/1 ARM means your rate is locked for 7 years, then resets once a year going forward. Simple as that.

ARM Type | Fixed Period | Adjusts Every | Best For |

3/1 ARM | 3 years | Annually | Short-term owners, quick resale plans |

5/1 ARM | 5 years | Annually | Homeowners planning to move or refinance within 5 years |

7/1 ARM | 7 years | Annually | Mid-term plans with some flexibility |

10/1 ARM | 10 years | Annually | Longer horizon but want a lower starting rate |

Rate Caps — Your Protection Against Big Jumps

Here's something many borrowers don't realize: your rate can't just skyrocket overnight. ARMs come with caps that limit how much your rate can move.

There are three caps to know:

Initial cap — limits how much the rate can change at the very first adjustment

Periodic cap — limits how much it can move at each adjustment after that

Lifetime cap — the absolute ceiling over the entire life of the loan

A real example makes this click: say you have a 5/1 ARM at 6% with a 2/2/5 cap structure. At the first adjustment, your rate can't go above 8%. At each annual adjustment after that, it can't jump more than 2% at a time. And over the full life of the loan, it can never exceed 11% — no matter what the market does.

That's your worst-case ceiling, and knowing it upfront helps you plan.

What Index Does Your ARM Follow?

When your rate adjusts, your lender doesn't just pick a number out of thin air. It's tied to a publicly tracked benchmark called SOFR the Secured Overnight Financing Rate which is now the standard index used across the mortgage industry.

SOFR moves with broader economic conditions and is influenced by Federal Reserve policy. Your lender then adds their fixed margin on top of whatever SOFR is at the time of adjustment. That combined number becomes your new rate.

The margin is set at closing and never changes; it's the SOFR portion that moves.

ARM vs. Fixed-Rate Mortgage — Which Is Right for You?

The honest answer is: it depends entirely on your current timeline and your long-term financial goals. Neither option is universally better than the other.

The right choice between ARM vs. Fixed-Rate Mortgage comes down to a few practical questions: How long do you plan to stay in your home? How much does monthly payment predictability matter to your family’s budget?

Ultimately, your decision should align with what you are trying to accomplish right now whether that means refinancing to lower your rate, accessing your home equity for a major expense, or simply keeping your monthly costs as manageable as possible.

Here's a straightforward side-by-side look:

ARM | Fixed-Rate | |

Starting Rate | Typically lower | Typically higher |

Payment Predictability | Changes after fixed period | Same for the life of the loan |

Best Horizon | Short to mid-term (3–10 years) | Long-term (10+ years) |

Risk Level | Moderate — rate can rise | Low — no surprises |

Refinancing Flexibility | Often a smart pairing | Works well long-term |

An ARM tends to make sense if you:

Plan to sell or refinance within 5 to 10 years

Expect your income to grow and can handle a higher payment later if needed

Want lower initial payments to free up cash flow now

Are tapping home equity and plan to pay it down relatively quickly

A fixed rate tends to make more sense if you:

Plan to stay in the home for 10 or more years

Want to know exactly what your payment will be every single month

Prefer to avoid any financial uncertainty, even if it costs a little more upfront

Neither choice is wrong; they just serve different situations. If you're not sure which camp you fall into, that's exactly the kind of conversation worth having with a mortgage advisor before you commit.

Refinancing Into an ARM — When It Makes Strategic Sense

Refinancing into an ARM might sound counterintuitive especially if you've always associated adjustable rates with risk. But in the right situation, it can be one of the smartest moves a homeowner makes.

The most common scenario: you're currently locked into a high fixed rate, you don't plan to stay in the home much longer, and ARM rates are meaningfully lower right now. If you refinance into a 7/1 ARM and sell or refinance again before those 7 years are up, you capture the savings without ever facing an adjustment.

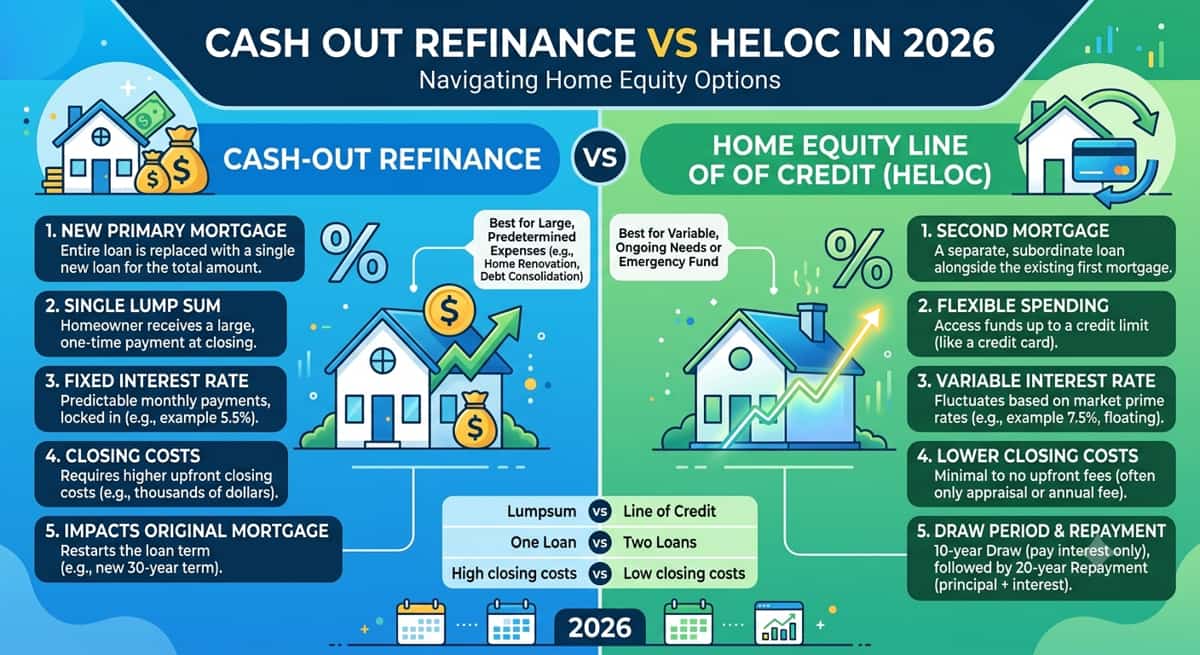

There are two main types of refinances to consider here. A rate-and-term refinance simply replaces your existing loan with better terms, lower rate, different loan length, or both. A cash-out refinance lets you tap your home equity at the same time, pulling out a portion of what you've built up as cash. Both can be done with an ARM, though the right choice depends on your goals.

One thing I always walk clients through is the break-even point of how long it takes for your monthly savings to outweigh the closing costs of refinancing. If you're saving $200 a month and closing costs are $4,000, you break even in 20 months. If you plan to move in two years, the numbers may still work in your favor.

Before I'd recommend an ARM refinance to anyone, I'd want to know:

How long do you realistically plan to stay in this home?

How would you handle a higher payment if rates rise after the fixed period?

Is your income likely to grow over the next several years?

Are you trying to preserve your home equity, or access it?

Those four questions shape everything.

Pros and Cons of Adjustable Rate Mortgages

Like any financial product, an ARM has real advantages and real drawbacks. Here's an honest look at both.

What works in your favor:

Lower starting rate. One of the biggest advantages of an ARM is that the initial rate it's typically lower than what you'd get with a fixed loan, which means a lower monthly payment right out of the gate.

Real savings potential. If you sell or refinance before the fixed period ends, you may never see a rate adjustment at all and pocket the difference in the meantime.

Breathing room each month. Many homeowners find that the lower payment frees up cash flow for other priorities, whether that's paying down debt, building savings, or handling home repairs.

On the downside:

Payment uncertainty. Once the fixed period ends, your payment can change and that unpredictability is genuinely stressful for some borrowers.

Rates can climb. Depending on where the index moves, your rate could increase meaningfully, especially in a rising-rate environment.

It takes more to understand. Unlike a fixed mortgage, there are more moving parts caps, indexes, margins which can feel overwhelming without good guidance.

Refinancing isn't free. If you decide to refinance out of an ARM later, closing costs apply all over again.

Neither list is meant to scare you off or sell you on anything. It's just the full picture.

ARM Mortgage Rates in 2025 — What the Market Looks Like

ARM rates in 2025 have remained noticeably lower than 30-year fixed rates and that gap matters more than people realize.

When there's a meaningful spread between a 5/1 ARM and a 30-year fixed loan, even half a percentage point translates into real monthly savings. On a $400,000 mortgage, that difference can mean $100 to $200 less per month at the start money that stays in your pocket during the fixed period.

The Federal Reserve's rate decisions directly influence where ARM index rates land. When the Fed raises rates, SOFR tends to follow, which eventually works its way into ARM adjustments. When the Fed cuts, borrowers with ARMs can actually benefit at adjustment time.

Pull the current 5/1 ARM rate and 30-year fixed rate from the Freddie Mac weekly survey at time of publication and insert specific figures in the first paragraph for accuracy and freshness.

Is an Adjustable Rate Mortgage Right for You?

An ARM isn't for everyone but for the right borrower, it can be a genuinely smart financial move. If you have a clear timeline, a specific goal around refinancing or home equity, and a realistic picture of what you can handle if rates rise, it's absolutely worth considering.The key is going in with eyes open, not guessing.

Every situation is different: your income, your home equity, how long you plan to stay, what you're trying to accomplish. Those details change the math entirely, and they're exactly what a licensed mortgage advisor works through with you before recommending anything.You don't have to figure this out alone.

Explore whether an ARM or refinance makes sense for your situation.