Thinking about tapping into your home’s equity or refinancing your current mortgage can feel like a smart financial move until you think about the paperwork. As a licensed mortgage consultant who has helped hundreds of homeowners navigate this exact path, I completely understand if the thought of digging through old financial statements feels overwhelming.

But here is the good news: getting pre-qualified doesn't require you to have everything perfect on day one. Think of it as a quick, low-stress financial health check. It gives you a clear picture of what you can borrow without hurting your credit score, saving you hours of guesswork down the road.

Whether you want to lower your monthly payments, pay off high-interest debt, or finally start that home remodel, getting organized early is the secret to a smooth, stress-free experience. Let’s look at exactly what you need to gather so you can move forward with total confidence.

What Is Mortgage Pre-Qualification - and Why It Matters Before You Shop

Mortgage pre-qualification is essentially a first look. You share some basic financial information: your income, your debts, your assets and a lender tells you roughly how much you may be able to borrow. It's not a guaranteed loan offer, but it gives you a realistic number to work with before you start seriously shopping.

A lot of people confuse pre-qualification with pre-approval. Think of it this way: pre-qualification is the conversation, pre-approval is the deep dive. Pre-approval involves a full credit check and verified documents. Pre-qualification is faster and gives you a solid starting point.

Here's why it matters: sellers and real estate agents take pre-qualified buyers more seriously. It signals that you've done your homework and you're not just browsing. In a competitive market, that early preparation can be the difference between getting a showing and getting passed over.

And if you're refinancing or exploring a home equity loan, pre-qualification still applies. Lenders want the same foundational picture of your finances before they move forward no matter what type of home loan you're pursuing.

The Complete Mortgage Pre-Qualification Checklist

Lenders are essentially trying to answer one question: can this person reliably repay a loan? To figure that out, they look at five core areas of your financial life. Missing documents in even one of these areas can slow the process down by several days, sometimes longer. So before you pick up the phone or submit an online inquiry, pull these together. It'll make the whole process faster and a lot less stressful.

1. Proof of Identity

Before a lender can look at anything else, they need to confirm who you are. This sounds simple, but it's the step that catches people off guard more than you'd think.

You'll need a government-issued photo ID, a driver's license or passport works. You'll also need to provide your Social Security Number. If you're not a U.S. citizen, a green card, valid visa, or ITIN (Individual Taxpayer Identification Number) will typically be required depending on your loan type.

One thing I always tell clients: make sure the name on your ID matches the name on your financial documents exactly. A nickname on one form and a legal name on another can create unnecessary back-and-forth that delays everything. Get that consistent before you start.

2. Income Verification Documents

This is the section most people underestimate especially if their income doesn't come from a single employer with a straightforward paycheck.

If you're a salaried employee, you'll need your W-2s from the last two years and your two most recent pay stubs. That's the baseline.

If you're self-employed, the bar is a little higher. Lenders will want two years of federal tax returns both personal and business along with a year-to-date profit and loss statement. This is where I see a lot of people run into trouble. Self-employed borrowers often write off a significant amount of business expenses, which is smart for taxes but can lower the income number lenders use to qualify you. It's worth talking to an advisor before you apply so you understand exactly what income figure will show up on paper.

If you earn 1099 income freelance work, contract jobs, gig economy work, gather those forms for the past two years along with your tax returns.

And if part of your income comes from bonuses or commission, lenders will typically average that over two years. One strong bonus year doesn't carry as much weight as consistent earning history does.

3. Asset and Bank Account Statements

Lenders want to see where your money lives and that you actually have enough of it to cover a down payment, closing costs, and ideally a few months of mortgage payments in reserve.

Pull together the last two to three months of statements from every bank account you hold. That includes checking accounts, savings accounts, money market accounts, all of them. If you have retirement accounts like a 401(k) or IRA, bring those statements too. Investment or brokerage account statements are also fair game.

Here's something that trips people up: if you've had a large deposit land in your account recently, say, a few thousand dollars from a family member or the sale of something, lenders will ask where that money came from. They need to verify it's not an undisclosed loan.

If a family member is helping with your down payment, that's completely allowed on most loan types, but you'll need a signed gift letter confirming the money isn't expected to be repaid. Have that ready before it comes up.

4. Employment History

Lenders want to see two years of steady employment history. This doesn't mean you need to have worked at the same company for two years, it means they want to see a consistent pattern of earning income.

Be ready to list your employers for the past two years: company names, addresses, job titles, and the dates you worked there. If there are gaps, don't panic but be prepared to explain them briefly. A period of medical leave, a career transition, or going back to school all have straightforward explanations. What lenders are looking for is context, not perfection.

A recent job change or promotion in the same industry typically isn't a problem. Switching fields entirely right before applying? That can raise questions, so timing matters.

If you're planning a job change, try to wait until after you've closed on your loan. Stability on paper carries real weight at this stage.

5. Debt and Monthly Obligation Overview

This is the piece most people come in least prepared for and it's one of the most important.

Lenders will calculate your debt-to-income ratio, or DTI. In simple terms, that's how much of your monthly gross income goes toward debt payments. They look at two numbers: your housing costs as a percentage of your income, and your total monthly debts as a percentage of your income.

For most conventional loans, lenders prefer a total DTI under 43–45%. FHA loans can sometimes go higher with compensating factors. VA loans tend to be more flexible, but lenders still pay close attention.

Your list of monthly obligations should include car loans, student loans, minimum credit card payments, personal loans, everything. Child support and alimony payments are required disclosures as well.

What Lenders Actually Look At During Pre-Qualification

Once you hand over your information, here's what lenders are actually doing with it.

They're zeroing in on three things: your income, your credit, and your assets. Everything in your checklist feeds into one of those three buckets.

Credit score is a big one. For a conventional loan, most lenders want to see a score of at least 620, though better rates kick in at 740 and above. FHA loans can go as low as 580 with a 3.5% down payment, or even 500 with a larger down payment depending on the lender. The important thing to know at the pre-qualification stage: many lenders run a soft credit pull first, which does not affect your credit score. It's only when you move to full pre-approval that a hard inquiry typically shows up.

Qualifying income is calculated on your gross earnings before taxes averaged over the past two years. If your income has gone up significantly, lenders will often average the two years together rather than use just the most recent year.

DTI benchmarks have two parts. The front-end ratio covers just your housing costs (mortgage payment, taxes, insurance) and should generally stay under 28–31%. The back-end ratio covers all monthly debts combined and should stay under 43–50% depending on loan type.

Knowing these numbers before you apply lets you walk in with realistic expectations.

Special Situations - What to Prepare If Your Scenario Is More Complex

Not every borrower fits the standard two-years-employed, W-2, single-account profile. That's fine. These situations come up all the time, and they're workable; they just need the right documentation from the start.

Recently self-employed (under 2 years): If you've been running your own business for less than two years, conventional lenders may have a harder time qualifying your self-employment income alone. In some cases, if you were previously in the same field as a salaried employee before going independent, lenders will consider that continuity. A strong P&L, clean bank statements, and a year of business tax returns can help fill the gap. It's worth having a direct conversation with an advisor about your options before applying.

Going through a divorce or separation: Lenders will need to see your separation agreement or divorce decree, especially if child support or alimony is involved either as income you receive or as an obligation you pay. If a property is being transferred, a quitclaim deed may be needed. Bring what you have; your advisor can tell you what else is required.

Received a large gift or inheritance recently: This is fine but lenders will want a documentation trail. A gift letter, the transfer record, and bank statements showing when the funds arrived are typically enough.

These aren't deal-breakers. They're paperwork challenges, and most of them have clean solutions.

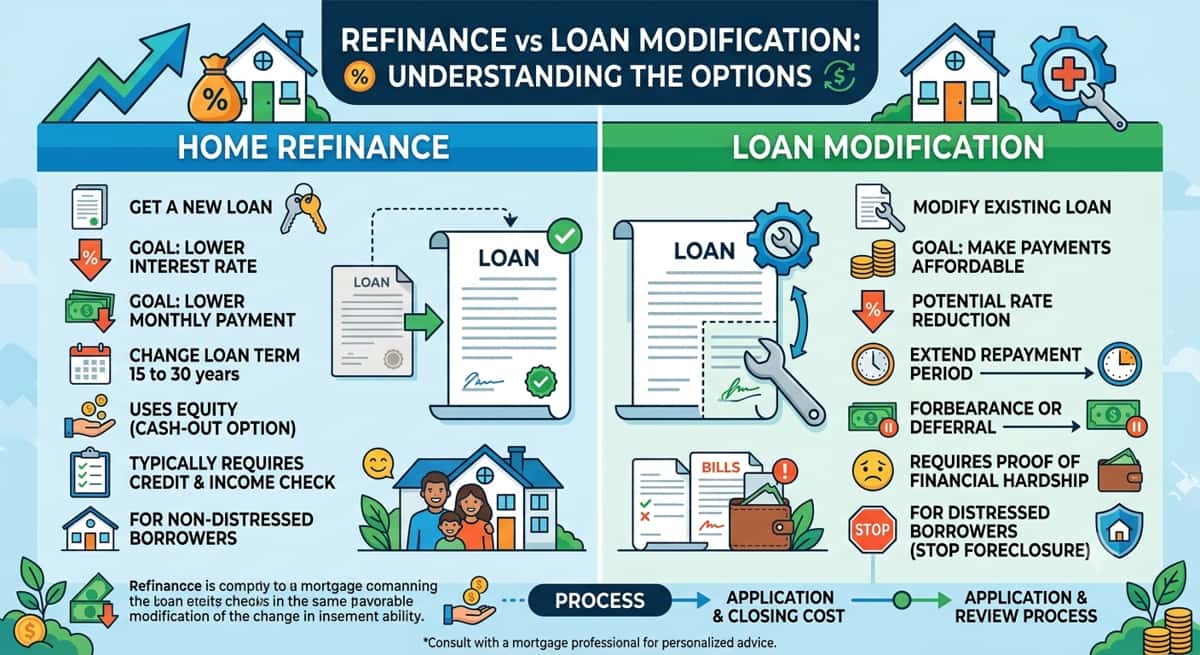

Pre-Qualification for Refinancing or Home Equity - Is It Different?

In most ways, no the core documents are the same. Income, assets, employment history, debts. Lenders need that picture regardless of what you're trying to do.

But there are a few things you'll need to add if you're refinancing or applying for a home equity loan or line of credit.

First, bring your most recent mortgage statement. Lenders want to see your current balance, your interest rate, and your payment history. Late payments on your existing mortgage will come up, so it's better to be upfront about anything in your history.

Second, have your homeowners insurance declarations page and most recent property tax statement ready. These factor into your total housing cost calculation.

Third and this one is specific to home equity products lenders will assess your loan-to-value ratio, or LTV. That's the relationship between what you owe on your home and what it's currently worth. For a HELOC or home equity loan, most lenders want you to have at least 15–20% equity remaining after the loan. For a cash-out refinance, LTV limits vary by loan type.

If you're unsure what your home is currently worth, I can walk you through how lenders typically assess that before ordering a formal appraisal.

Common Mistakes That Delay Pre-Qualification (And How to Avoid Them)

I've seen the same patterns slow people down over and over. Most of them are completely avoidable.

Opening new credit accounts right before applying. A new car loan, a store credit card, a big purchase on financing all of these can change your credit score and your DTI overnight. Try to hold off on any new credit for at least 60–90 days before you plan to apply.

Submitting incomplete or mismatched documents. A missing page from a bank statement, a name spelled differently across forms, or a document that's one month out of date can send your file to the back of the line. Read the document requirements carefully and submit everything at once.

Not disclosing all income or debts. Lenders verify everything. If you have rental income, side business income, or a loan you co-signed, disclose it. Omissions slow things down and can create bigger problems later.

Pulling your own credit report too early, then waiting too long to apply. Soft pulls are fine anytime, but if your lender does a hard pull and then months pass before you actually apply, they'll need to pull credit again.

The most common delay I see? Borrowers who aren't sure which bank accounts to include. When in doubt: include all of them.

How Long Does Pre-Qualification Take?

If your documents are organized and ready to go, pre-qualification can happen the same day, sometimes within a few hours. Most of the time, you're looking at one to three business days.

What slows it down? Missing documents, questions about large deposits, income that doesn't fit the standard mold, or a backlog on the lender's end. Working with a dedicated mortgage advisor tends to move faster than going through a large bank or an automated online system, because there's a real person reviewing your file who can ask you a quick question rather than sending a formal request that takes two days to answer.

In my experience, the borrowers who come in with everything organized using a checklist like this one cut that timeline in half. The preparation does the work before the conversation even starts.

Trust Your Equity with a Licensed Mortgage Advisor

Your home is likely your biggest financial asset, and protecting its equity means making decisions with a trusted professional by your side. As a fully licensed mortgage advisor registered with the Nationwide Multistate Licensing System (NMLS), I am committed to putting your financial well-being first. Navigating the refinancing or home equity process doesn't have to be a solo journey. Let’s sit down for a zero-obligation consultation to review your checklist, answer your questions, and find the right path forward for your specific financial goals. Reach out today to schedule your conversation.