July 23, 2026

10 min read

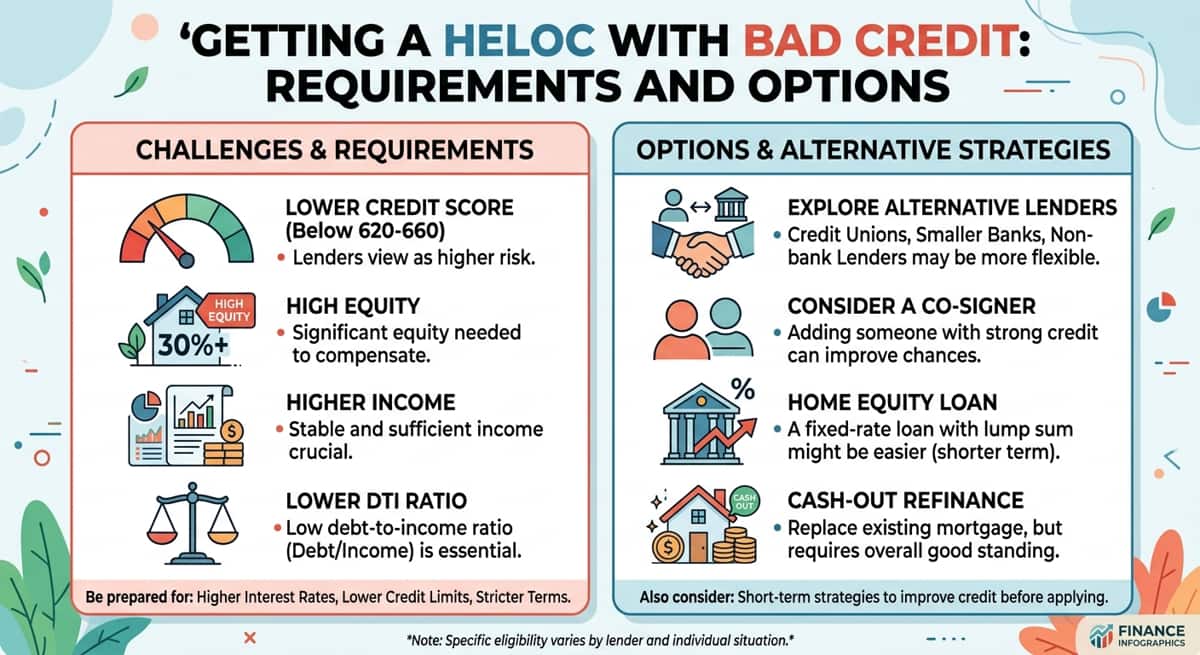

HELOCReverse Mortgage

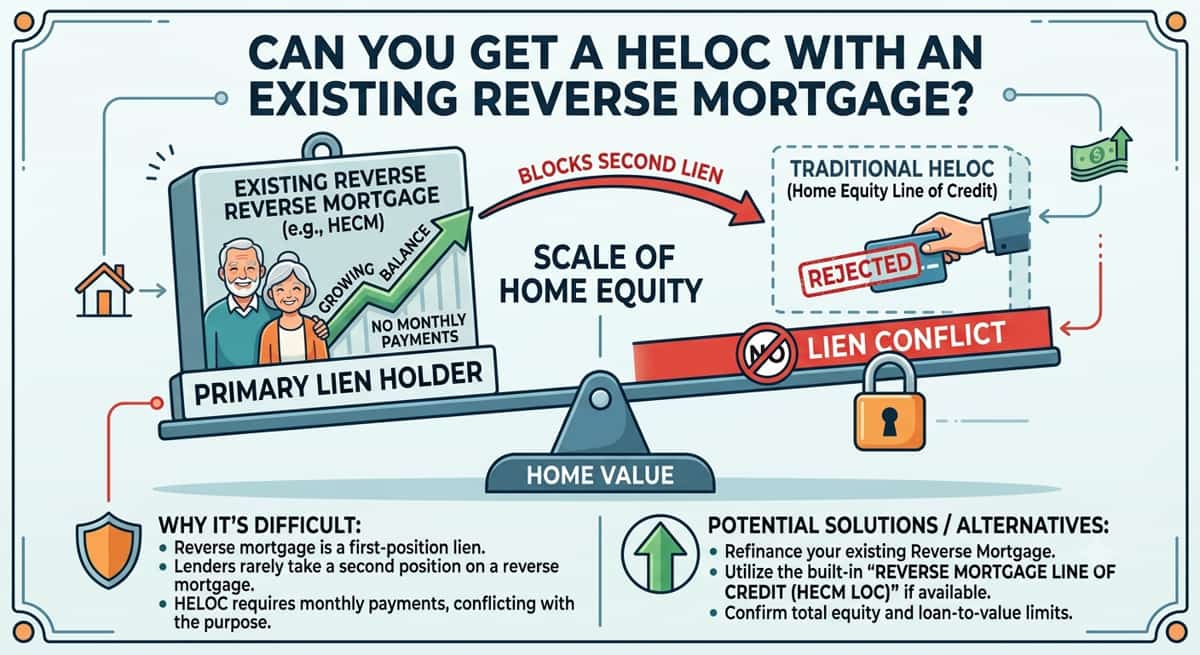

Can You Get a HELOC with an Existing Reverse Mortgage?

You generally cannot get a HELOC with an existing reverse mortgage because reverse mortgages require a first-lien position. Adding an unapproved second lien violates loan terms. Instead, you can tap an existing reverse mortgage line of credit, refinance into a larger loan, downsize, or consider an unsecured personal loan.