If you own a home, there's a good chance you're sitting on more equity than you realize. Across the country, homeowners are holding onto trillions of dollars in tappable equity and a lot of that money is just sitting there, untouched, while life keeps handing out expenses: a leaky roof, a kid heading to college, credit card balances that won't budge.

Two of the most common ways to turn that equity into usable cash are a cash-out refinance and a HELOC (home equity line of credit). They can both get you money. But they work in very different ways, and picking the wrong one for your situation can cost you thousands of dollars over the next several years.

This guide walks through exactly how each option works in 2026, what they actually cost, and how to figure out which one fits your life. Mortgage rates and tax rules have shifted recently, so we'll keep things current and point out where the old advice you might have heard no longer applies.

What Is a Cash-Out Refinance?

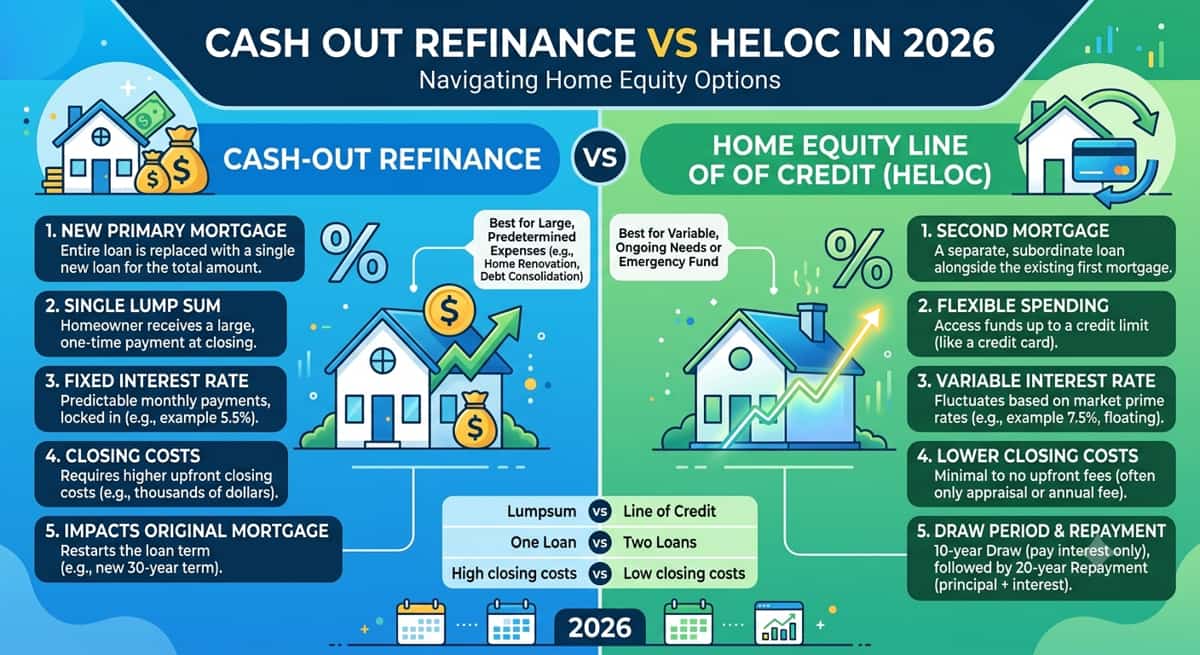

A cash-out refinance replaces your entire current mortgage with a brand-new, bigger one. You pay off your old loan, and you walk away from closing with the difference in cash.

Here's a simple way to picture it. Say you owe $300,000 on your home, and your home is now worth $450,000. You refinance into a new $360,000 loan. That new loan pays off your old $300,000 balance, and you pocket the remaining $60,000 (minus closing costs) as a lump sum.

The important thing to remember is that this isn't just a loan on your $60,000. It's a brand-new mortgage on the entire $360,000, with a new rate and a new term. If your old mortgage had a great rate, you're giving that up and your new rate applies to your whole balance, not just the cash you're pulling out.

What Is a HELOC (Home Equity Line of Credit)?

A HELOC works completely differently. Instead of replacing your mortgage, it sits on top of it as a second loan, secured by the same house.

Think of it like a credit card that's backed by your home equity. You get approved for a credit limit based on how much equity you have, and then you can draw money from that line whenever you need it. You don't have to take it all at once.

Most HELOCs have two phases:

The draw period (typically around 10 years): you can borrow, repay, and borrow again, and many lenders only require interest-only payments during this stretch.

The repayment period (typically 10 to 20 years): the draw window closes, and you start paying back both principal and interest on whatever balance you have left.

The part homeowners love most: your original mortgage doesn't change at all. Same rate, same balance, same payment. The HELOC is just layered on top.

HELOC vs. Home Equity Loan: Quick Clarification

Home equity loan and HELOC, it's easy to mix the two up. A home equity loan gives you a fixed lump sum upfront, with a fixed rate and a set monthly payment, no draw period, no flexibility. A HELOC, on the other hand, is a revolving line you tap into as needed. Same general idea (borrowing against your equity), very different experience day to day.

Cash-Out Refinance vs. HELOC: 2026 Rate Comparison

Rates are really the heart of this decision, so let's get specific.

As of early-to-mid 2026, cash-out refinance rates are tracking close to the broader 30-year fixed mortgage market generally landing somewhere around 6.8% to 8.5%, with the most qualified borrowers (excellent credit, lower loan-to-value) seeing offers closer to the 6.25%–6.8% range, based on Freddie Mac and Bankrate averages.

HELOC rates are running higher, typically in the 7.5% to 8.5% range, since they're priced off the prime rate plus a margin, and prime rate moves with the Federal Reserve's benchmark rate.

Why does the HELOC carry a higher rate even though it can be smaller? It comes down to risk. A HELOC is a second lien, which means if you ever default, your primary mortgage lender gets paid first. HELOC lenders charge more to offset that added risk.

One more thing worth knowing: the Fed made several rate cuts through late 2025, and most forecasts going into 2026 suggest things are leveling off rather than climbing further though nothing is guaranteed. Because HELOC rates are variable, this matters more for HELOC borrowers than for cash-out refi borrowers, whose rate is locked in for the life of the loan.

Mortgage rates shift weekly, sometimes daily. The numbers above are a snapshot, not a quote. Always check current rates from a few lenders before making a decision.

At a Glance: Cash-Out Refi vs. HELOC

Feature | Cash-Out Refinance | HELOC |

Rate type | Fixed | Usually variable |

Average rate range (2026) | ~6.8%–8.5% | ~7.5%–8.5% |

Lien position | Replaces first mortgage | Second lien |

Payment structure | Single fixed payment | Interest-only during draw, then P&I |

Access to funds | One lump sum | Draw as needed |

Typical closing costs | 2%–5% of loan amount | $0–$500 (often free) |

Funding speed | 3–6 weeks | As fast as a few days |

Minimum credit score | ~620 (740+ for best rates) | 620–680 (720+ for best rates) |

Typical DTI limit | 43%–45% | 43%–45% |

The #1 Factor That Decides Which Option Wins: Your Current Mortgage Rate

If there's one question that matters more than any other, it's this: what rate are you paying on your mortgage right now?

A huge number of homeowners locked in rates somewhere between 2.5% and 5% during 2019 through 2022. If that's you, a cash-out refinance means giving up that rate on your entire balance just to access a portion of your equity. That's often a costly trade.

Here's the simple way to think about it:

If your current rate is lower than today's refinance rates a HELOC usually makes more sense. You keep your cheap first mortgage untouched and only pay the higher rate on the amount you actually borrow.

If your current rate is at or above today's refinance rates a cash-out refinance can work in your favor. You might lower your rate on your whole loan while also pulling out cash essentially solving two problems at once.

As an example (not a guarantee every situation is different): a homeowner with a $400,000 mortgage at 3.5% on a home worth $750,000 would likely come out ahead with a HELOC, since refinancing that 3.5% rate away to access equity would cost far more in the long run than just opening a second loan. Meanwhile, someone carrying a 7.5% mortgage from a couple of years ago might actually improve their situation with a cash-out refi if today's rates are lower than 7.5%.

This is the single biggest factor that separates the two options, and it's worth doing the math on your specific numbers before deciding either way.

Closing Costs and Fees: What You'll Actually Pay

Cost is where these two products really part ways.

A cash-out refinance typically runs 2% to 5% of the new loan amount in closing costs. On a $400,000 loan, that's somewhere between $8,000 and $20,000 covering things like the appraisal, title work, origination fees, and underwriting. You can pay these costs upfront, or roll them into your loan balance.

A HELOC is usually far cheaper to open. Many lenders charge little to nothing somewhere between $0 and $500 and some offer no-closing-cost HELOCs entirely (though these sometimes come with a slightly higher rate margin in exchange).

Here's a trap a lot of people fall into: rolling your refinance closing costs into the loan feels painless at the time, but you end up paying interest on those fees for the entire life of the loan. A $12,000 closing cost rolled into a 30-year loan at 7% doesn't just cost $12,000 by the time you've paid it off, it can cost closer to $28,000 once interest is factored in.

This is also where the idea of a break-even period comes in: how long do you need to stay in your home before the money you save from refinancing outweighs what you paid to get the new loan? If you're not planning to stay put for several years, those upfront costs may never pay for themselves and a HELOC's lower entry cost becomes even more appealing.

Qualification Requirements: Credit Score, DTI, and LTV

Lenders look at similar factors for both products, but the bar is set a little differently.

Cash-out refinance:

Minimum credit score: around 620 for conventional loans, though you'll need 740+ to get the best available rate

Loan-to-value (LTV): capped at 80% for most conventional loans; VA loans can go up to 100% for eligible veterans; FHA cash-out refis also cap around 80%

Debt-to-income (DTI): generally needs to stay under 43%–45%

HELOC:

Minimum credit score: typically 620–680, with 720+ needed for the most competitive rates

Combined loan-to-value (CLTV): usually capped at 80%–85%

DTI: similar range, generally under 43%–45%

If you're a veteran or active-duty service member, VA loan programs can offer more flexibility on the cash-out refinance side. FHA loans have their own specific requirements too. These programs are worth asking about directly with a lender, since eligibility depends on a handful of factors specific to you.

Pros and Cons Side-by-Side

Cash-Out Refinance Pros and Cons

Pros:

Fixed rate means your payment never changes, no surprises

One single loan, one single monthly payment to keep track of

If market rates have dropped since you got your current mortgage, you might improve your rate on your whole balance

You get the full amount of cash at once, which is helpful for big, one-time expenses

Cons:

Resets your loan term if you're 10 years into a 30-year mortgage and refinance into a new 30-year loan, you're extending how long you'll be paying

Closing costs are meaningfully higher

If your current rate is lower than today's rates, your monthly payment could go up, not down

HELOC Pros and Cons

Pros:

Low or zero closing costs in most cases

You only pay interest on what you actually draw, not your full credit limit

Your existing mortgage and its rate stay completely untouched

Funding tends to be much faster sometimes just a matter of days

Cons:

Variable rate means your payment can rise if broader rates rise

When the draw period ends and repayment begins, your payment can jump noticeably this is sometimes called payment shock

Credit score requirements tend to be a bit stricter

Rates run higher than a first mortgage because the lender is in a riskier second position

Which Option Fits Your Situation? 5 Real-World Scenarios

Every homeowner's situation is a little different, but a few patterns come up again and again in conversations with clients. Here are five common ones, think of these as illustrations, not a script to follow exactly. Your numbers might tell a different story.

1. You are locked in at a low rate before 2023 and want to fund a renovation. If you're sitting on a rate under 5%, protecting it is usually worth more than the simplicity of a single loan. A HELOC typically wins here.

2. Your current rate is higher than today's rates, and you need a large sum upfront. This is a case where a cash-out refinance can genuinely help twice over lowering your rate on your full balance while also putting cash in your hands.

3. You're tackling a multi-stage renovation with costs that aren't fully known yet. When you're not sure exactly how much you'll need or when, a HELOC's draw-as-you-go flexibility tends to be far more practical than locking into one lump sum.

4. You're consolidating high-interest credit card debt and your mortgage rate is close to today's market rate. A cash-out refinance can work well here, rolling debt into one fixed payment often builds in the discipline that helps people actually pay it down, rather than running balances back up on a revolving line.

5. You need money fast, within a couple of weeks. HELOCs, especially through lenders offering appraisal waivers on smaller loan amounts, tend to move much faster than a full refinance.

These are starting points, not final answers. The right move depends on your rate, your goals, your timeline, and your comfort with payment variability which is exactly the kind of thing worth running by a licensed advisor with your actual numbers in hand.

Tax Implications: Is the Interest Deductible in 2026?

This is an area where a lot of outdated information is still floating around, so let's clear it up.

For a while, there was an assumption that the stricter tax rules from 2017 were set to expire and revert back to looser rules in 2026. That's no longer accurate. Recent legislation made those stricter rules permanent starting in 2026. Here's what that actually means for you:

The rule that matters: interest is deductible only if the money is used to buy, build, or substantially improve the home that secures the loan. Using the funds for a kitchen remodel or a new roof? That generally qualifies. Using the funds to pay off credit cards, cover medical bills, or fund a vacation? That doesn't qualify for a deduction, even though it's still a perfectly legitimate use of the money.

A few more details to know:

This rule applies the same way to a cash-out refinance and a HELOC. The IRS doesn't care what your lender calls the loan; it only cares what you did with the money.

There's a combined mortgage debt limit of $750,000 for married couples filing jointly ($375,000 if filing separately). This includes your first mortgage plus any home equity debt combined.

You have to itemize your deductions on Schedule A to claim this at all if your itemized total doesn't beat the standard deduction, there's no tax benefit from the interest, regardless of how you used the funds.

Keep your paperwork. The IRS wants to see proof contractor invoices, receipts, and records showing the money actually went toward home improvements (see IRS Publication 936 for the full details).

This is general information, not personalized tax advice. Tax situations vary a lot from person to person, so it's worth talking to a CPA before assuming any deduction applies to you.

Risks to Understand Before You Borrow

Both of these products use your home as collateral, which means the risks deserve real attention, not just a passing mention.

With either option, your home is on the line. If payments aren't made, foreclosure is a real possibility; this isn't unsecured debt like a credit card.

With a HELOC specifically, the variable rate means your payment isn't fixed in stone. And the shift from the draw period into the repayment period can bring a real jump in your monthly payment, sometimes catching borrowers off guard if they haven't planned for it.

With a cash-out refinance specifically, stretching your loan back out to a fresh 30-year term can mean you end up paying more total interest over time, even if your new rate looks lower on paper. It's worth running the full-term math, not just comparing rates side by side.

One safeguard built into both products: most lenders require you to keep at least 15%–20% of your equity in reserve after borrowing. This isn't just a lender rule for their own protection it also helps protect you from ending up owing more than your home is worth if values dip.

How to Decide: A Quick Self-Assessment Checklist

Ask yourself these questions:

Is my current mortgage rate lower than today's refinance rates? Leans HELOC

Do I need all the money at once for a single, defined expense? Leans cash-out refinance

Am I uncertain about exactly how much I'll need or when? Leans HELOC

Do I want one predictable payment instead of a rate that can move? Leans cash-out refinance

Do I need the money within the next couple of weeks? Leans HELOC

If your answers point in different directions, that's normal most real situations involve some trade-offs. That's exactly when running your specific numbers with an advisor makes the biggest difference.

Talk to a Licensed Mortgage Advisor Before You Decide

Every homeowner's numbers tell a different story. Your current rate, how much equity you've built, what you actually need the money for, and how long you plan to stay in your home all change the math sometimes significantly.

I've spent years helping homeowners across the U.S. weigh exactly this decision, comparing real rate quotes against real financial goals rather than guessing from averages. If you'd like a personalized side-by-side comparison based on your actual mortgage and equity position, I'm happy to walk through it with no pressure, just clear numbers.