If you're staring at your mortgage statement wondering whether there's a better way forward, you're not alone. Maybe your interest rate feels too high compared to what you're seeing in the news. Or maybe you've hit a rough patch: a job loss, a medical bill, a divorce and keeping up with your payment feels harder every month. Both situations lead people to the same question: should I refinance, or do I need a loan modification?

These two options sound similar, but they solve very different problems. Over the years, I've sat down with homeowners on both sides of this decision, some looking to save money, others trying to keep their home.

What Is Mortgage Refinancing?

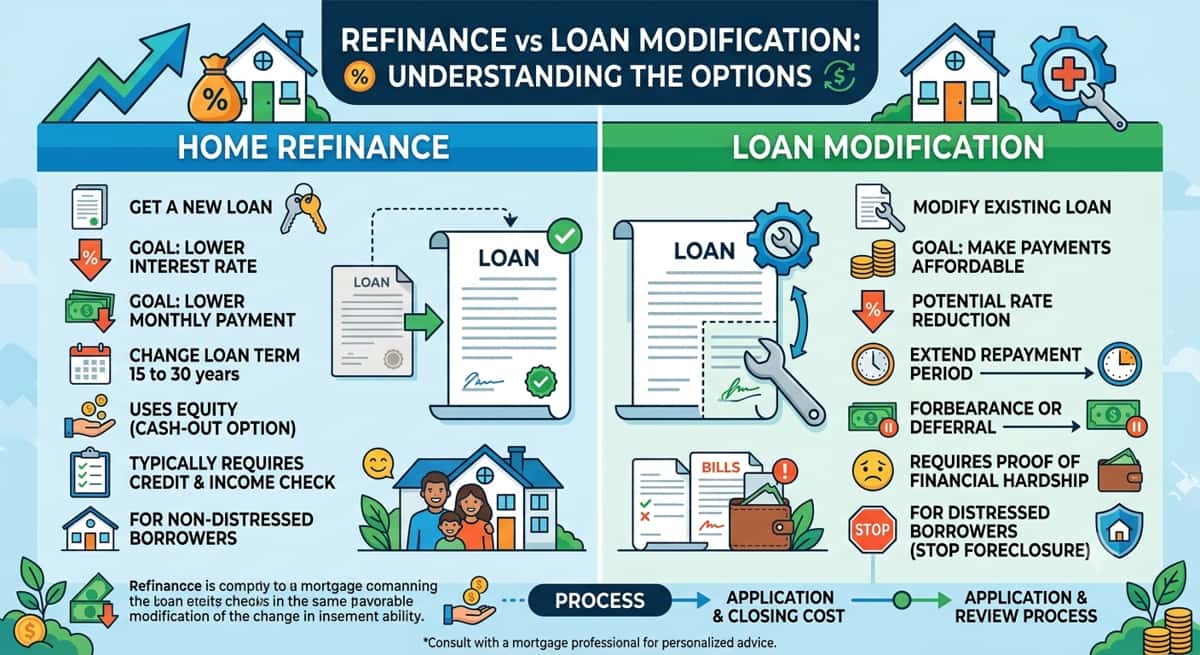

Refinancing simply means replacing your current mortgage with a brand new one. You're not changing your existing loan, you're paying it off completely with a new loan, usually with different terms.

People typically refinance for a few common reasons: to get a lower interest rate and reduce their monthly payment, to pull cash out of their home's equity for things like renovations or debt payoff, to shorten their loan term and pay off the house faster, or to get rid of mortgage insurance once they've built up enough equity.

Think of it like trading in your old car loan for a new one with better terms, same house, fresh start on the loan itself.

What Is a Loan Modification?

A loan modification is different. Instead of replacing your loan, it changes the terms of the loan you already have. Your lender might adjust your interest rate, extend the number of years you have to pay it back, or in some cases reduce the amount you owe.

This option is usually reserved for homeowners going through financial hardship not something you can simply shop around for like a refinance. It typically starts with a conversation with your loan servicer, where you explain your situation and provide documentation showing why you're struggling to keep up with payments.

The goal of a modification isn't to get a better deal. It's to make your current loan more manageable so you can stay in your home.

Key Differences Between Refinancing and Loan Modification

At first glance, these two options might seem like they're solving the same problem but they work in very different ways. Here's a simple breakdown of how they compare:

Refinancing | Loan Modification | |

What it is | A brand new loan that pays off your old one | A change to the terms of your existing loan |

Who qualifies | Homeowners with decent credit and steady income | Homeowners experiencing financial hardship |

Cost | Closing costs (often 2–5% of the loan amount) | Usually little to no cost |

Credit check | Yes, a full credit check is required | Often based on hardship documentation, not credit score |

Timeline | A few weeks to a couple of months | Can take longer, especially with back-and-forth paperwork |

Best for | Improving your rate or terms when finances are stable | Avoiding default or foreclosure during a hardship |

The biggest thing to understand is this: refinancing is something you choose when your finances are in good shape and you want a better deal. A loan modification is something you request when you're struggling and need help making your current loan work.

One more important difference: refinancing gives you a fresh start with a new loan, new terms, and a new closing process. A loan modification keeps your original loan in place, just with adjusted terms layered on top.

When Refinancing Makes Sense

Refinancing tends to be the right move when your overall financial picture is stable; you're just looking for better terms. Here are some situations where it's worth exploring:

Your credit and income are in good shape. If you've been keeping up with payments and your credit score has improved since you first got your mortgage, you may now qualify for a noticeably better rate than before.

Rates have dropped since you bought your home. Even a small drop in your interest rate can add up to real savings over the life of your loan, sometimes hundreds of dollars a month.

You want to tap into your home's equity. If you've built up equity and need funds for a renovation, education costs, or paying off higher-interest debt, a cash-out refinance lets you access that money.

You need to remove a co-borrower. Going through a divorce or buying out a family member from the property? Refinancing lets you take their name off the loan entirely.

Your rate adjusts and you want stability. If you're on an adjustable-rate mortgage and want the predictability of a fixed rate, refinancing can lock that in.

If any of this sounds like your situation, it's worth taking a closer look at refinancing.

When a Loan Modification Makes Sense

A loan modification is built for a different kind of situation, one where you're not looking to get a better deal, but rather trying to get through a difficult time without losing your home.

You're dealing with financial hardship. A job loss, a serious illness, reduced work hours, or a divorce can all throw your budget off balance. If your income has dropped and your current payment no longer fits, a modification can help bring it back in line with what you can actually afford.

You've fallen behind on payments. If you're already a month or two behind or worried you're heading that way a modification can help you get current without facing penalties that make the gap even harder to close.

Refinancing isn't an option for you right now. Maybe your credit took a hit, or your income looks different on paper than it did before. If you wouldn't qualify for a new loan at this point, a modification works with the loan you already have.

You want to avoid foreclosure. If missed payments are starting to pile up, reaching out for a modification early can be the difference between keeping your home and losing it.

This isn't about shopping for a better rate, it's about making your current loan workable again.

How Each Option Affects Your Credit and Finances

It's natural to wonder how either option might impact your credit and your finances down the road so here's a general look at what to expect.

With refinancing, lenders will run a hard credit check as part of the application process, which can cause a small, temporary dip in your score. You'll also be taking on a new loan with its own terms, and closing costs are often rolled into the loan or paid upfront.

With a loan modification, the way it's reported to credit bureaus can vary depending on your lender and your specific situation. It may affect how future lenders view your file if you apply for credit down the road. That said, falling behind on payments or going through foreclosure tends to have a much more lasting impact on your credit and finances than a modification typically does.

Every situation is a little different, so if you're concerned about how either option might affect you specifically, it's worth talking through the details with your lender or a trusted advisor before moving forward.

Pros and Cons at a Glance

Refinancing

Pro: Can lower your monthly payment or interest rate

Pro: Lets you access home equity for cash if needed

Pro: Can switch loan types (like adjustable to fixed) or shorten your term

Con: Comes with closing costs that take time to recoup

Con: Requires good credit and steady income to qualify

Con: Involves a full application and approval process, similar to your original mortgage

Loan Modification

Pro: Can make your payment more manageable during hardship

Pro: Usually little to no upfront cost

Pro: Can help you avoid foreclosure and stay in your home

Con: Not guaranteed approval depends on your lender and situation

Con: May extend how long it takes to pay off your home

Con: Generally only available if you're experiencing genuine financial hardship

Looking at both lists side by side can help make it clearer which option lines up with what you actually need right now.

Which One Should You Choose? How to Decide

If you're still not sure which path fits your situation, try starting with one simple question: are you currently struggling to make your payments, or are you managing fine and just looking to improve your terms?

If you're keeping up with your mortgage without too much stress, and you're curious about a lower rate, accessing equity, or changing your loan type refinancing is likely the better fit. You're in a position of strength, and a refinance is about making a good situation even better.

On the other hand, if you've missed a payment, you're worried about missing one soon, or a recent change in income or expenses has made your current payment feel out of reach, a loan modification is probably the more realistic path. This option exists specifically to help in moments like these.

There's also a middle ground worth mentioning: some homeowners assume they're stuck because their credit has taken a hit, when refinancing might still be possible or assume they need a modification when a smaller adjustment could solve the problem.

This is exactly why it helps to sit down with a and go over your actual numbers. A quick review of your situation can point you toward the option that truly fits.

Steps to Take Before Deciding

Before you settle on a direction, a few simple steps can help bring clarity to your decision.

Start by pulling out your most recent mortgage statements. These show your current rate, remaining balance, and loan terms all things you'll need to compare against other options.

If you're leaning toward refinancing, take a look at today's average mortgage rates and compare them to what you're currently paying. If the difference is significant, it may be worth estimating how long it would take for the savings to cover the closing costs; this is often called your "break-even point."

If you're dealing with a hardship, reach out to your loan servicer directly. They can walk you through what documentation is needed and what modification options might be available based on your situation.

In either case, talking to a licensed mortgage advisor can help. They can look at your full picture and give you a clear, personalized read on which path makes the most sense for you.