You've worked hard to build a life, paid your bills, kept up with your mortgage, maybe even built some equity in your home. But now, as you look into refinancing or tapping into that home equity, a single number keeps coming up in every lender conversation: your debt-to-income ratio, or DTI.

And honestly? It can feel like a mystery. Nobody hands you a rulebook when you're juggling a car payment, a student loan, and a mortgage.

Your DTI ratio is simply the percentage of your monthly income that goes toward paying your debts. That's it. Lenders use it to figure out whether you can comfortably take on a new loan payment without stretching yourself too thin.

What Is a Debt-To-Income Ratio (DTI)?

Think of your DTI ratio as a snapshot of your financial balance; how much of what you earn each month is already spoken for by debt payments.

More precisely, it's the percentage of your gross monthly income (what you earn before taxes) that goes toward your monthly debt obligations. So if you bring home $6,000 a month before taxes and your total debt payments add up to $2,000, your DTI is about 33%.

Lenders look at this number because it tells them something your credit score alone can't: whether you actually have enough breathing room in your monthly budget to handle a new loan payment. A strong credit score shows you've paid your bills on time but a healthy DTI shows you're not already stretched too thin.

Here's something worth knowing: lenders actually look at two types of DTI, not just one.

Front-End DTI only counts your housing costs, your mortgage or rent payment, property taxes, homeowner's insurance, and HOA fees if applicable. Most lenders like to see this stay below 28%.

Back-End DTI is the bigger picture. It includes your housing costs plus every other monthly debt obligation, car loans, student loans, credit card minimum payments, personal loans, child support, or alimony. This is the number most lenders focus on when reviewing your application, and it's what most people mean when they simply say "DTI."

How To Calculate Your DTI Ratio (Step-by-Step)

The good news? You don't need a financial degree to figure out your DTI. A little addition and one simple division is all it takes and knowing your number before you apply puts you miles ahead of most borrowers.

Here's the formula lenders use:

DTI = (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100

Let's break that down into three easy steps.

Step 1: Add Up Your Monthly Debt Payments

Write down every recurring debt obligation you pay each month. This includes:

Mortgage or rent payment

Car loan(s)

Student loans

Credit card minimum payments

Personal loans

Child support or alimony (if applicable)

Important: Don't include everyday living expenses like groceries, utilities, subscriptions, or gas. Only debts money owed to a lender or required by a legal obligation count here.

Step 2: Find Your Gross Monthly Income

This is your income before taxes and deductions are taken out, not what lands in your bank account. If you're salaried, divide your annual salary by 12. If you're self-employed or have variable income, lenders typically average your last two years of tax returns.

Step 3: Divide and Multiply

Now plug your numbers into the formula.

Real-world example:

Monthly debts: $2,000

Gross monthly income: $6,000

DTI = ($2,000 ÷ $6,000) × 100 = 33.3%

That's a DTI most lenders would consider solid.

Two Mistakes That Throw Off Your Calculation

Using your take-home pay instead of gross income is the most common error. Your net (after-tax) income is always lower, which makes your DTI look worse than it actually is by lender standards.

Forgetting smaller recurring debts like a store credit card you barely use or a personal loan you're almost done paying can also skew your number. Include everything, even if the payment feels insignificant.

What Is a Good DTI Ratio for a Mortgage?

Once you know your DTI, the natural next question is: is it good enough? The honest answer is it depends on the type of loan you're applying for. But there are clear benchmarks that most lenders work from, and knowing where you fall gives you a realistic picture before you ever sit down with an underwriter.

Here's a quick look at how lenders generally interpret your DTI:

DTI Range | Lender View | Loan Eligibility |

Below 36% | Excellent | Most conventional & FHA loans |

36% – 43% | Acceptable | Most loans, sometimes with conditions |

43% – 50% | Marginal | Limited options; compensating factors needed |

Above 50% | High Risk | Difficult to qualify with most lenders |

The 43% Rule - And Why It Matters

You'll hear 43% come up a lot in mortgage conversations, and there's a reason for that. Under federal mortgage guidelines, 43% is the standard threshold for a Qualified Mortgage, a loan category that comes with built-in consumer protections and is considered a lower risk for both you and the lender.

Going above 43% doesn't automatically mean a door slams shut, but it does mean lenders will look harder at the rest of your application, your credit score, your savings, your employment history to feel confident you can manage the payment.

How DTI Requirements Differ by Loan Type

Not every loan plays by the same rules. Here's what each major loan type generally looks for:

Conventional Loans follow Fannie Mae guidelines, which typically allow a back-end DTI up to 45%, and in some cases up to 50% with strong compensating factors like excellent credit or significant cash reserves.

FHA Loans are more flexible by design; they're built to help more people qualify for homeownership. FHA generally allows a DTI up to 43%, but borrowers with strong credit scores (580+) and solid financial histories may be approved up to 50%.

VA Loans available to eligible veterans and active-duty service members don't set a hard DTI cap, but most VA lenders prefer to see a back-end DTI at or below 41%. The VA also uses a separate "residual income" calculation alongside DTI, which actually makes it a more complete picture of affordability.

USDA Loans, designed for eligible rural and suburban homebuyers, typically cap back-end DTI at 41%, though exceptions can be made with compensating factors.

A Quick but Important Note

The ranges above are general guidelines not guarantees. Every lender weighs DTI alongside your full financial profile: credit score, employment stability, assets, and the size of your down payment or available equity. A DTI that disqualifies you with one lender may be perfectly acceptable with another.

If you're unsure where your DTI lands or what it means for your specific situation, a licensed mortgage advisor can give you a clear, honest answer based on your actual numbers, not just a chart.

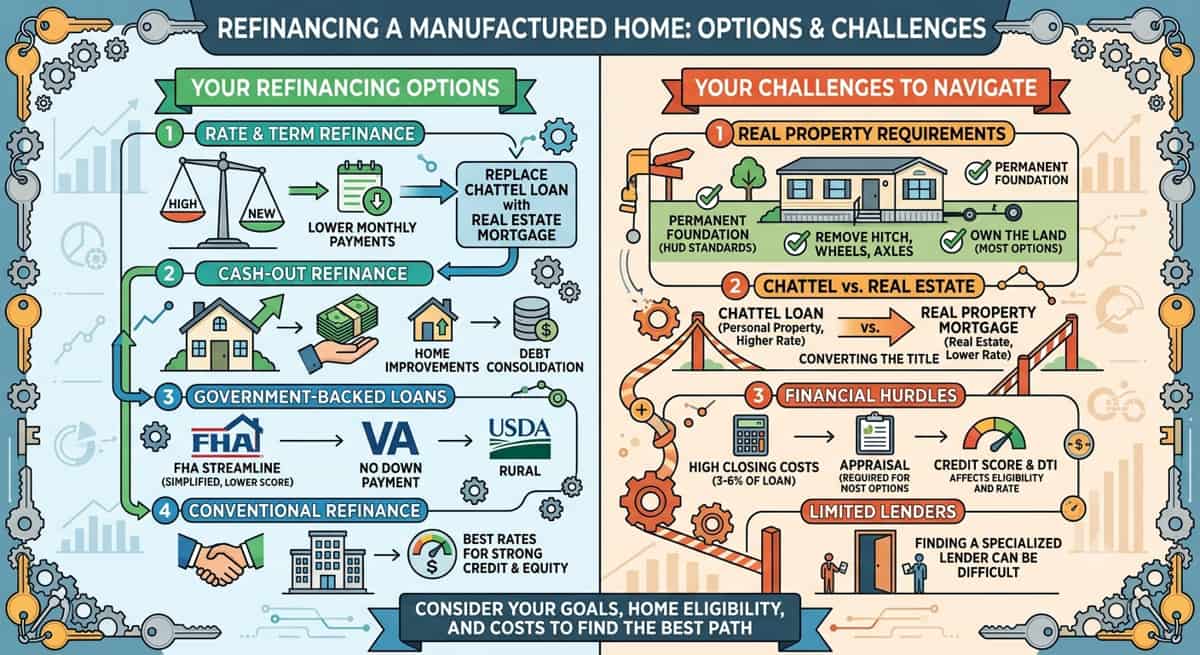

DTI Ratio for Refinancing: What Lenders Expect

Refinancing can be a smart financial move locking in a lower rate, reducing your monthly payment, or pulling out cash for a major expense. But here's something many homeowners don't realize until they're already in the process: refinancing isn't treated as simply modifying your existing loan. In the eyes of the lender, you're applying for a brand-new mortgage. That means your DTI gets a full review, just like when you first bought your home.

Rate-and-Term vs. Cash-Out: Does It Change the DTI Bar?

Rate-and-term refinance is straightforward: you're replacing your current mortgage with a new one at a better rate or different term, without taking any cash out. Because you're not increasing your overall debt load, lenders are generally more flexible. Most conventional lenders are comfortable with a DTI up to 45% for this type of refinance.

Cash-out refinance is a different story. You're borrowing more than you currently owe and pocketing the difference which means a larger loan, a potentially higher monthly payment, and more risk from the lender's perspective. As a result, many lenders tighten their DTI requirements for cash-out refinances, often preferring 43% or below, and scrutinizing the rest of your financial profile more closely.

How Rising Interest Rates Affect Your DTI When Refinancing

This is something that catches a lot of homeowners off guard. When interest rates rise, your new mortgage payment may actually be higher than what you're paying now even if you're refinancing into the same loan amount. A higher payment means more of your income goes toward debt, which pushes your DTI up. It's entirely possible to have a DTI that qualified you comfortably two years ago but sits closer to the borderline today, simply because rates have shifted.

This is why timing and planning matter so much with refinancing decisions.

A real example: A homeowner with $3,200 per month in total debt obligations on a $7,500 gross monthly income has a DTI of 42.7%. That's likely within range for a rate-and-term refinance with most conventional lenders but it's borderline for a cash-out refinance, where even a small increase in the monthly payment could push that number past the threshold.

That small difference in DTI can mean the difference between a smooth approval and having to rethink your approach entirely.

Learn more about your refinancing options and what today's rates mean for your situation

What Factors Impact Your DTI Ratio?

Your DTI isn't a fixed number carved in stone. It moves up or down based on what's happening in your financial life. Understanding what pushes it in either direction helps you make smarter decisions, especially in the months leading up to a mortgage application.

Things That Can Lower Your DTI

A raise or promotion directly improves your DTI because your gross monthly income goes up while your debts stay the same. Even a modest salary increase can meaningfully shift your ratio.

Additional income sources like a part-time job, freelance work, or rental income from a property you own can also count toward your gross income. The catch: lenders typically want to see at least a two-year history of that income before they'll include it in the calculation. A side hustle you started three months ago usually won't move the needle yet.

Things That Can Raise Your DTI

Taking on new debt is the fastest way to hurt your DTI before an application. A new car loan, a furniture financing plan, or even a new credit card with a balance can add hundreds of dollars to your monthly obligations overnight. If you're planning to apply for a mortgage or refinance in the near future, this is the time to hold off on any major new purchases on credit.

Student loan payments count in full even if you're on an income-driven repayment plan or in deferment. Lenders have specific rules about how deferred student loans are counted, and it sometimes surprises borrowers to learn those payments are still factored in.

Alimony and child support payments are treated as monthly debt obligations by lenders, the same way a car payment would be. If you're required to make these payments, they go into your DTI calculation.

When Your Income Isn't a Steady Paycheck

If your income fluctuates because you're self-employed, work on commission, pick up seasonal work, or have variable hours, lenders don't just take your word for what you earn. They'll typically average your last two years of tax returns to arrive at a monthly income figure. If your income has been growing steadily year over year, that works in your favor. If it's been inconsistent or declining, it may raise questions.

This is one area where working with an experienced mortgage advisor really pays off someone who knows how to present variable income in the strongest, most accurate light.

How To Lower Your DTI Ratio Before Applying for a Mortgage

If your DTI is sitting higher than you'd like, the good news is that it's one of the most actionable numbers in your financial profile. Unlike your credit history which takes time to rebuild your DTI can shift meaningfully in just a few months with the right moves. Here's where to focus your energy.

Pay Down Credit Cards First

Of all the debts on your list, revolving debt like credit cards gives you the biggest DTI improvement per dollar paid. That's because your minimum payment is directly tied to your balance pay it down, and your required monthly payment drops almost immediately. A car loan or student loan, by contrast, keeps the same fixed monthly payment whether you've paid ahead or not.

If you have multiple credit cards, focus on the one with the highest minimum payment first. Eliminating or significantly reducing that payment can move your DTI more than almost anything else.

Knock Out Smaller Loans Entirely

If you're close to paying off a personal loan, a small store credit account, or any other installment debt, consider pushing hard to close it out completely before you apply. Eliminating a monthly payment entirely, even a modest one removes it from your DTI calculation altogether. A $150 monthly payment that disappears can make a real difference when lenders are reviewing your numbers.

Hold Off on Any New Debt

This one sounds simple, but it's where a lot of borrowers unintentionally hurt themselves. A new car loan, a financed appliance, or even a new credit card opened "just for the sign-up bonus" can add hundreds of dollars to your monthly obligations before you've even filled out a mortgage application. In the three to six months before you plan to apply, treat your DTI like it's already under review because soon, it will be.

Document Every Source of Income

Lowering your debt is only half the equation. Raising your documented income works just as well mathematically. If you've received a raise, taken on a second job, started earning rental income, or have consistent freelance earnings with a two-year track record, make sure those income sources are properly documented. A higher gross monthly income means a lower DTI even if your debts stay exactly the same.

Consider Debt Consolidation - Carefully

A debt consolidation loan can roll multiple monthly payments into one, sometimes at a lower interest rate and with a reduced combined monthly payment. When it works, it's a straightforward way to lower your DTI and simplify your finances at the same time. Just be cautious: consolidating debt only helps your DTI if the new single payment is genuinely lower than the sum of what you were paying before. Run the numbers before you commit.

In my experience working with homeowners across the U.S., I often recommend targeting at least a 3–5% DTI reduction before reapplying after a decline. It sounds small, but that shift is frequently enough to move a file from the "needs review" pile to an approval. Small, deliberate changes add up faster than most people expect.

Common DTI Myths - Debunked

There's a lot of half-true information floating around about DTI, and believing the wrong thing can lead you to either panic unnecessarily or walk into an application unprepared. Let's clear up the most common ones.

"My credit score matters more than my DTI so DTI isn't a big deal."

Your credit score and your DTI are two separate conversations in a lender's mind. A strong credit score shows you pay your bills reliably. A healthy DTI shows you have the monthly breathing room to take on a new payment. Lenders need to feel confident about both one cancels out the other. Plenty of borrowers with excellent credit scores have been surprised by a denial rooted in a DTI that was too high.

"DTI includes my monthly bills like utilities, groceries, and car insurance."

It doesn't. Your DTI only counts formal debt obligations, loans, credit cards, and legally required payments like child support or alimony. Your electric bill, your phone plan, your Netflix subscription none of that factors in. This actually works in your favor, because your real monthly expenses are almost certainly higher than your DTI suggests.

"If my DTI looks good, I'm basically approved."

DTI is one important piece of the puzzle, but lenders are also looking at your credit score, your employment history, how much equity or down payment you have, your cash reserves, and your loan-to-value ratio all at the same time. A strong DTI improves your position significantly, but it doesn't guarantee approval on its own.

"Every lender uses the same DTI cutoff."

They don't. DTI thresholds vary by loan type, by lender, and sometimes by the strength of the rest of your application. One lender's hard stop at 43% is another lender's starting point for a conversation. This is exactly why shopping around or working with a mortgage advisor who knows multiple lending options can make a real difference.

When To Talk to a Mortgage Advisor About Your DTI

Calculating your DTI is something you can absolutely do on your own and now you know how. But understanding what your number means for your specific situation, your goals, and the loan you're trying to get? That's where having an experienced advisor in your corner makes a real difference.

Here are some situations where a conversation is genuinely worth your time:

You're not sure if your DTI qualifies for a refinance or home equity loan. The benchmarks in this guide are a solid starting point, but your full financial picture credit, equity, income stability, loan type determines what's actually possible for you.

You've already been declined and weren't given a clear explanation. A denial doesn't always mean the door is closed. Sometimes it means the approach needs adjusting. Understanding exactly why your application was declined is the first step toward fixing it.

You want a realistic paydown plan before you apply. Rather than guessing which debts to tackle first, a mortgage advisor can look at your actual numbers and tell you the most efficient path to the DTI you need so you're not spending months on changes that won't move the needle.

Your income isn't a simple salary. If you're self-employed, work on commission, have rental income, or earn money from multiple sources, DTI calculations get more nuanced. Lenders handle variable income differently, and knowing how to document and present it correctly can significantly change your outcome.

The Bottom Line on DTI

Your debt-to-income ratio is one of the most revealing numbers in your mortgage application and now you understand exactly what it means, how to calculate it, and what lenders are looking for when they review it.

To recap what matters most:

DTI measures how much of your gross monthly income goes toward debt payments

Below 43% is where most loan approvals become realistic below 36% is where you're in genuinely strong territory

Different loans have different thresholds FHA, VA, conventional, and home equity products all play by slightly different rules

You can improve your DTI by paying down revolving debt, eliminating smaller loans, and properly documenting all your income sources

That said, DTI is just one part of the story. Lenders are also weighing your credit, your equity, your employment history, and more all at once. A number that looks borderline on paper can still lead to an approval when the full picture is strong.

Understanding your DTI is the first step. Knowing how to use it strategically and how it fits into your broader financial profile is where talking with the right mortgage advisor truly makes a difference.