A Home Equity Line of Credit (HELOC) can be a flexible way to borrow against the equity you've built in your home. Homeowners often use it to finance renovations, consolidate higher-interest debt, cover education costs, or handle unexpected expenses. But once you start making payments, one important question usually comes up: Is HELOC interest tax deductible? The answer isn't as straightforward as many people expect. While HELOC interest can still qualify for a tax deduction in certain situations, it isn't automatically deductible simply because the loan is secured by your home.

Current tax laws set specific conditions on how the borrowed funds must be used, and misunderstanding those rules could lead to costly mistakes when filing your tax return. That's why it's important to separate outdated information from the rules that apply today. In this guide, you'll learn when HELOC interest is tax deductible, when it isn't, the IRS requirements you need to meet, and the records you should keep to support your claim. Whether you already have a HELOC or you're considering applying for one, understanding these tax rules can help you maximize potential savings while staying compliant with current regulations. By the end, you'll have a clear understanding of what qualifies and what doesn't before tax season arrives.

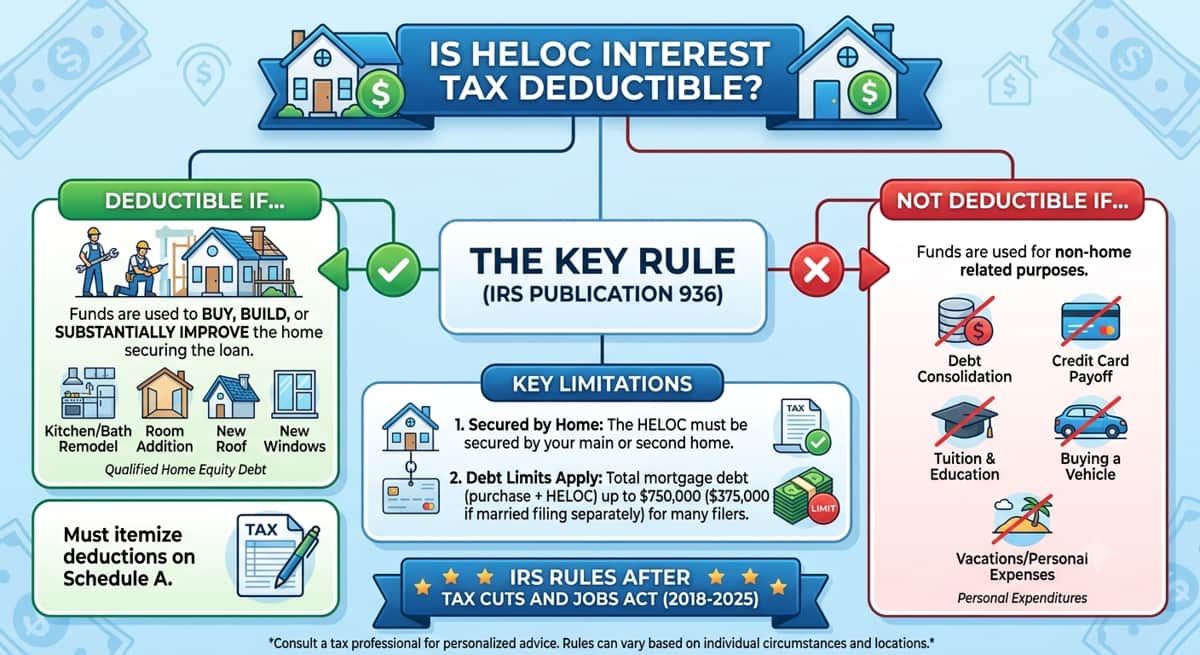

Is HELOC Interest Tax Deductible?

HELOC interest can be tax deductible, but only under specific conditions. If you used your home equity line of credit to buy, build, or substantially improve the home that secures the loan, you may be able to deduct the interest you paid. If you used it for something else, like paying off credit cards or covering everyday expenses, that interest generally won't qualify.

I get this question a lot from homeowners who assume that because a HELOC is secured by their house, the interest automatically counts as a tax break. It doesn't work that way anymore. What you did with the money matters more than the loan itself.

What Counts as "Buy, Build, or Substantially Improve"

This is the part that trips people up the most, so let's break it down with real examples.

Qualifying projects are ones that genuinely add value to your home, extend how long it will last, or adapt it for a new purpose. Think along these lines:

A kitchen or bathroom remodel

Adding a bedroom, office, or other livable space

Replacing a roof or foundation repair

Upgrading major systems, like a new HVAC unit or full electrical rewiring

Building a garage, deck, or in-law suite

I had a client last year who used $60,000 from a HELOC to gut and rebuild an outdated kitchen, new cabinets, plumbing, the works. That interest qualifies, because the project clearly improved the home's value and usefulness. Compare that to another homeowner who used a smaller draw to repaint a few rooms and fix a leaky faucet. Those are maintenance items, not improvements, so that interest wouldn't count.

The general test I walk clients through is this: does the project change the home in a meaningful way, or is it just upkeep? If it's upkeep, it almost certainly doesn't qualify.

What Doesn't Qualify

To be clear about what falls outside the rule, here's what typically won't get you a deduction:

Paying off credit card debt

Covering medical bills

Funding a vacation

Paying for college tuition

Buying a car

General living expenses

None of these change the home itself, so even though the loan is secured by your house, the IRS doesn't treat the interest as connected to the property.

The Dollar Limits You Need to Know

Even if your project qualifies, there's a cap on how much debt the deduction applies to. For loans taken out after December 15, 2017, you can deduct interest on a combined total of up to $750,000 in mortgage debt if you're married filing jointly or filing as a single taxpayer. That drops to $375,000 if you're married filing separately.

Here's the key detail people miss: this isn't a separate limit just for your HELOC. It's a combined limit that includes your primary mortgage plus any home equity debt on top of it.

Let's say you have a $700,000 mortgage balance and you take out a $100,000 HELOC to renovate your kitchen. Your combined debt is $800,000, which is $50,000 over the limit. In that case, only the interest on the first $50,000 of your HELOC would be deductible, not the full amount. The remaining $50,000 of HELOC debt sits above the cap, so interest on that portion doesn't qualify no matter how the money was used.

If you're anywhere near that $750,000 combined mark, it's worth running the numbers with a tax professional before you borrow, so you know exactly what portion of the interest you can actually count on.

Do You Need to Itemize to Claim This Deduction?

Qualifying for the deduction is only half the equation. You also have to itemize your deductions on your tax return instead of taking the standard deduction, and for a lot of households, that's where the math gets less exciting.

For the 2025 tax year, the standard deduction is around $15,750 for single filers and roughly $31,500 for married couples filing jointly. Your itemized deductions, which would include your mortgage interest, HELOC interest, and things like charitable giving, need to add up to more than that standard amount before itemizing actually saves you money.

Don't assume a HELOC automatically comes with a tax perk just because the interest can technically qualify. If your total mortgage interest is already close to or under the standard deduction, adding HELOC interest on top might not push you into itemizing territory at all. Run the numbers with your CPA before you count on any tax savings. A lot of homeowners are surprised to find the deduction doesn't move the needle much for their actual return.

How to Document Your HELOC for the Deduction

If you do qualify, good recordkeeping is what makes the deduction usable. The IRS puts the burden of proof on you, the taxpayer, so you'll want a clear paper trail from the day you draw the funds to the day you pay the contractor.

Here's what to keep on hand:

Form 1098 from your lender, which reports the total interest you paid on the HELOC during the year. You should receive this by the end of January.

Contractor invoices, receipts, and permits that show exactly what the money was spent on.

Bank statements showing the draw from your HELOC and the payment going out to the contractor or supplier.

When it's time to file, the deduction gets claimed on Schedule A of your tax return, on the line for home mortgage interest.

One tip that saves my clients a lot of headaches later: open a separate account just for your HELOC funds, and only use it for the qualifying project. If you mix qualifying home improvement spending with personal expenses in the same account, you end up having to prove which dollars went where, and that gets messy fast. I've seen clients spend hundreds of dollars in accounting fees just to reconstruct months of mixed transactions. A dedicated account solves that before it becomes a problem.

What If My HELOC Is Used for a Rental or Second Home?

If you're using a HELOC in connection with a rental property or second home, the rules shift a bit. Interest tied to a rental property is often handled as a business expense rather than under the personal residence rules we've covered here, and the requirements for tracing the funds get stricter.

Basically, you need to be able to show, dollar for dollar, that the borrowed funds went toward that specific property. If the money gets mixed with funds used elsewhere, it complicates your ability to claim anything.

Rental and multi-property situations are where I always recommend looping in both a mortgage advisor and a CPA. The mortgage side and the tax side need to line up, and getting one without the other can leave money on the table or create problems down the road.

Common Mistakes Homeowners Make With HELOC Deductions

Over the years, I've seen the same handful of mistakes come up again and again:

Assuming all HELOC interest is deductible simply because the loan is secured by the house. It isn't; the use of the funds is what matters.

Forgetting the debt limit is combined, not a separate allowance for the HELOC on top of the mortgage.

Deducting interest on routine repairs, like painting or fixing appliances, instead of true capital improvements.

Not keeping documentation, then scrambling to piece together receipts and bank records if the IRS asks questions.

Borrowing mainly to chase the tax break, rather than because the project or the debt makes sense on its own.

That last one is worth sitting with for a second, because it leads into how I'd encourage you to think about this whole decision.

Should Tax Deductibility Influence Your HELOC Decision?

Here's my honest take after years of doing this: the tax deduction should be a bonus, not the reason you take out a HELOC in the first place.

I'd rather see a client borrow because a project genuinely needs funding and the numbers work for their budget, than borrow $50,000 hoping to save a few thousand dollars in taxes. The interest you pay on the loan itself is real money out of pocket every month, and a partial deduction doesn't erase that cost.

Before you open a HELOC, think through the basics first: can you comfortably handle the payments, does the project add real value to your home or your life, and does this fit your broader financial picture? If the answer is yes to those questions, a potential tax deduction is a nice add-on. If you're leaning on the tax angle to justify a loan that doesn't otherwise make sense, that's usually a sign to slow down and reconsider.

Talk to a Mortgage Advisor Before You Borrow

If you're weighing a HELOC for a renovation, an addition, or any other home project, I'm happy to walk through your options and help you figure out what makes sense for your situation. This article is meant to give you a clear, general picture of how HELOC interest deductions work, but it isn't personalized tax advice. For guidance specific to your return, it's always worth checking in with a CPA or tax professional before you file.

Reach out anytime you want to talk through your HELOC options or refinancing strategy. I'm here to help you borrow with a clear picture of what to expect, taxes included.