If your credit isn't perfect and you're wondering whether a HELOC is even worth applying for, here's the short answer: yes, you can still qualify it's just going to look a little different than it would for someone with great credit. Banks tend to get cautious when your credit history has a few dings in it, so you might face a higher interest rate, a smaller credit line, or a "no" from the first lender you try.

But that doesn't mean you're out of options. I've worked with plenty of homeowners who assumed bad credit meant an automatic rejection, only to find out there were lenders credit unions, portfolio lenders, and specialty programs willing to work with them once we looked at the full picture: their home equity, their income, and their recent mortgage payment history, not just their credit score.

What Is a HELOC, in Plain Terms?

A HELOC (home equity line of credit) is basically a credit card that's backed by your house. Instead of a lump sum, you get a credit limit you can borrow from whenever you need it, pay it back, and borrow again up to a set amount, for a set number of years (usually 10).

This is different from a home equity loan, which gives you one lump sum upfront that you pay back in fixed monthly payments, kind of like a second mortgage. A HELOC is more flexible, but it usually comes with a variable interest rate, meaning your payment can go up or down over time.

Both let you tap into the value you've built up in your home. The difference is mostly about how you receive and repay the money.

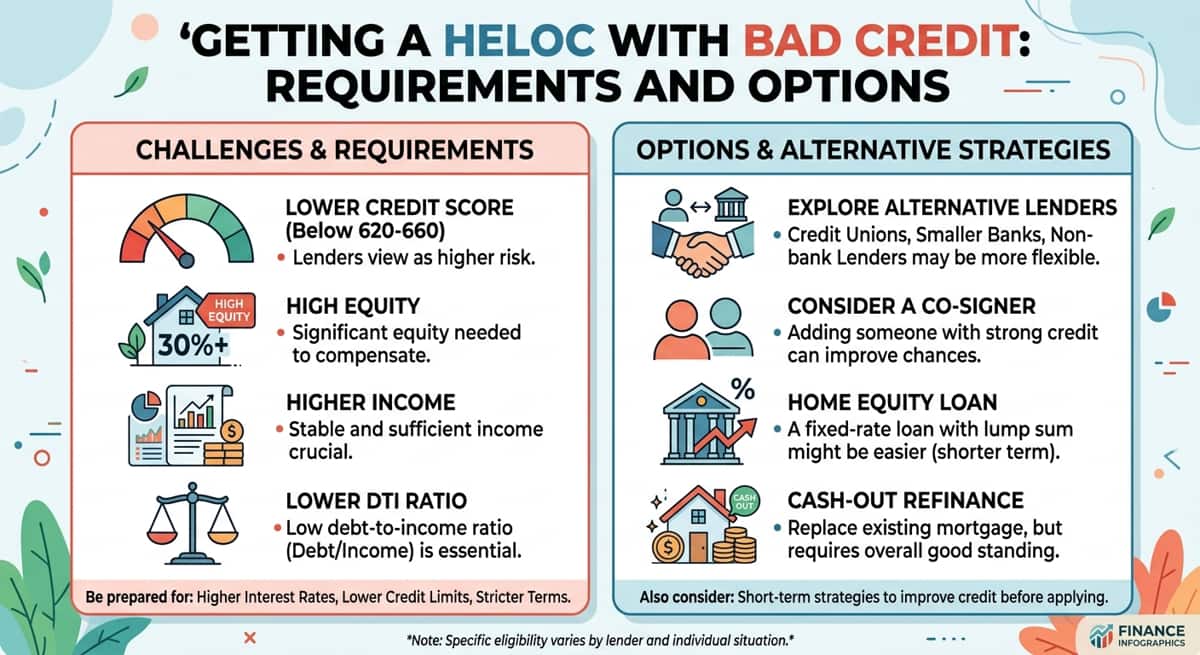

Can You Actually Get a HELOC with Bad Credit?

Yes but let's define "bad credit" first, because it means different things to different lenders. Generally, a FICO score below 620 is considered subprime territory for home equity lending. Below 580, you're in what most lenders call "poor" credit.

Here's the thing people often miss: your credit score is only one piece of the puzzle. Lenders also look at how much equity you have in your home, how much debt you're carrying compared to your income, and whether you've been keeping up with your mortgage payments. If those other numbers are strong, a lower credit score doesn't automatically disqualify you it just changes who's willing to work with you and what the terms look like.

What you should expect if your credit isn't great: a higher interest rate than someone with excellent credit, a smaller credit line relative to your home's value, and possibly some extra paperwork to prove you can handle the payments. It's not the friendliest deal on the table, but it's often a real option.

What Credit Score Do You Need for a HELOC?

There's no single magic number it varies by lender but here's a general breakdown of how credit scores tend to affect your HELOC options:

Credit Score | What It Typically Means for You |

720+ | You'll likely qualify with most lenders and get the best rates and largest credit lines. |

680–719 | Still considered strong. You should get approved with competitive terms at most banks. |

620–679 | You can usually still get approved, but expect a higher interest rate and possibly a smaller line. |

Below 620 | Traditional banks will likely say no. Credit unions, portfolio lenders, or non-QM programs become your best bet. |

These ranges come from how FICO scores are generally tiered by lenders and echoed in consumer guidance from the Consumer Financial Protection Bureau. Your actual approval will depend on the specific lender's guidelines, so it's worth shopping around rather than assuming one "no" means the door is closed everywhere.

Beyond Credit Score - Other HELOC Requirements

Your credit score gets a lot of attention, but it's really just one line item on the lender's checklist. Here's what else they're weighing.

Home Equity (Combined Loan-to-Value)

This is the big one. Lenders look at how much of your home you actually own outright called your equity compared to how much you still owe. Most lenders want your total debt against the home (your mortgage plus the new HELOC) to stay under about 80–85% of your home's value. The more equity cushion you have, the more comfortable a lender will feel taking a chance on you, even with so-so credit.

Debt-to-Income Ratio (DTI)

This is how much of your monthly income already goes toward debt payments car loans, credit cards, student loans, your mortgage, and so on. This figure is generally preferred to be below 43–50% of your income. A high DTI suggests you probably can’t take on another monthly payment, making it harder to get approved even with a good credit score.

Income and Employment Verification

Lenders need to know you have a steady, dependable source of income to repay the money you borrow. Expect to provide recent pay stubs, tax returns, or bank statements if you're self-employed. Consistent income can genuinely help offset a weaker credit score in a lender's eyes.

Payment History on Your Existing Mortgage

If you've been paying your current mortgage on time, that carries real weight even if your overall credit score has taken hits elsewhere (say, from a medical bill or an old credit card issue). A clean recent mortgage payment history tells a lender you prioritize your home, which is exactly what they want to see before lending against it.

Why Lenders Weight Credit So Heavily for HELOCs

It helps to understand the lender's side of this. A HELOC is what's called a "second lien" if you were ever unable to pay, your primary mortgage lender gets paid back first, and the HELOC lender is second in line. That extra risk is exactly why HELOC lenders tend to be more cautious about credit than a typical first-time mortgage lender. Combine that with the fact that most HELOCs have variable interest rates, meaning payments can rise over time, and you can see why lenders want reassurance that you can handle payment increases without missing them. It's not personal it's just how the risk math works out on their end.

Your Real Options for Getting a HELOC with Bad Credit

This is the part that actually matters: where do you go if a big national bank turns you down? Here are the paths that tend to work.

Credit Unions and Community Banks

Credit unions and smaller community banks often have more flexibility than large national banks because they keep loans in-house and make decisions based on your whole financial picture, not just a score cutoff. If you already have a relationship with a local credit union even just a checking account that history can work in your favor. It's worth having a real conversation with a loan officer there rather than relying on an online application that auto-rejects based on score alone.

Portfolio Lenders

Some lenders keep the loans they originate on their own books instead of selling them off to investors. Because they're not bound by the strict guidelines that come with selling loans on the secondary market, these "portfolio lenders" can set their own rules and often have more room to approve borrowers with lower credit scores, especially if equity and income look solid. A mortgage advisor who works with a network of lenders (rather than just one bank) can usually point you toward the right portfolio lenders for your situation.

Non-QM and Bank Statement Programs

If your credit issues are tied to being self-employed or having irregular income, non-QM ("non-qualified mortgage") programs are worth a look. These use bank statements or other alternative documentation instead of the strict income and credit requirements of a traditional loan. They tend to come with higher rates, but they exist specifically for people who don't fit the traditional lending box.

Adding a Co-Borrower or Co-Signer

If someone you trust a spouse, family member, or partner has strong credit and is willing to be added to the loan, it can significantly improve your approval odds. Just go in with eyes open: a co-signer is fully responsible for the debt too, so this only makes sense with someone you trust and have talked through the risks with.

Leaning on Higher Equity to Offset Credit Risk

If you've owned your home a while or made a large down payment, you may have significantly more equity than the minimum requirement. A bigger equity cushion gives lenders more confidence, because even in a worst-case scenario, there's more value backing the loan. If your credit is shaky but your equity is strong, say so upfront when you're talking to lenders it's one of your best bargaining chips.

How to Improve Your Approval Odds Before You Apply

If you have a little time before you need the money, a few weeks or months of prep can genuinely change your outcome:

Pay down credit card balances. Lowering how much of your available credit you're using (your credit utilization) can boost your score relatively quickly.

Check your credit report for errors. Mistakes on credit reports are more common than people realize. Dispute anything inaccurate through the credit bureaus.

Hold off on new credit applications. Each new inquiry can ding your score slightly. Avoid opening new cards or loans while you're preparing to apply.

Keep your mortgage payments on time. At least 12 months of on-time payments makes a real difference in how lenders view you.

Gather your documentation early. Pay stubs, tax returns, bank statements, and mortgage statements having these ready speeds up the process and shows you're organized and prepared.

None of these are overnight fixes, but even a 20–30 point score improvement can move you from "denied" to "approved" with certain lenders.

Alternatives to a HELOC If You Have Bad Credit

Sometimes a HELOC just isn't going to work out, at least not right now. Here are other ways to access money without waiting on a credit score to climb.

Cash-Out Refinance

Instead of adding a second loan, you replace your existing mortgage with a new, larger one and take the difference in cash. Since it replaces your first mortgage rather than sitting behind it, some lenders are more flexible on credit here than they are with a HELOC.

Home Equity Loan (Fixed Lump Sum)

Similar approval requirements to a HELOC, but you get one lump sum with a fixed rate and fixed monthly payment. Some borrowers find fixed payments easier to plan around than a HELOC's variable rate.

FHA 203(k) or Renovation Loan

If the money is specifically for home improvements, an FHA-backed renovation loan can be more forgiving on credit than a conventional HELOC, since FHA loans are generally built for borrowers with less-than-perfect credit.

Personal Loan

For smaller amounts, a personal loan doesn't require using your home as collateral at all. Rates are usually higher than a HELOC, but there's no risk to your house if things go sideways, which offers real peace of mind for some borrowers.

Risks to Understand Before Borrowing Against Your Home

Before moving forward with any option that uses your home as collateral, it's worth pausing on this: your house is on the line. If you're unable to keep up with payments, you could face foreclosure the same as if you missed payments on your primary mortgage.

HELOCs also typically come with variable interest rates, which means your payment could increase over time even if you borrowed responsibly at the start. Before you borrow, run the numbers on what your payment would look like if rates went up, and make sure it's a payment you could handle even in a tighter month. A good advisor will walk through this with you honestly, not just push you toward the loan.

How a Mortgage Advisor Can Help You Navigate a Bad-Credit HELOC

This is where working with an advisor rather than applying at a single bank and hoping for the best really pays off. A mortgage advisor isn't tied to one lender's rulebook. Instead, we shop your situation across credit unions, portfolio lenders, and specialty programs to find the ones most likely to say yes, and on the best terms available to you.

We also know how to present your file in the strongest light highlighting your equity, your on-time mortgage history, or your income stability when your credit score alone doesn't tell the full story. If you've been turned down once, that doesn't mean the answer is no everywhere. It often just means you talked to the wrong lender for your situation.

Bottom Line

A lower credit score makes getting a HELOC more challenging, but it doesn't close the door entirely. Between credit unions, portfolio lenders, non-QM programs, and strategies like adding a co-signer or leaning on strong home equity, there are real paths to approval you just need to know where to look and how to present your situation.

If you're not sure where you stand, the best next step is a conversation, not another automatic online application. A licensed mortgage advisor can look at your full picture credit, equity, income, and goals and tell you honestly which options actually make sense for you, and which lenders are most likely to say yes.