Refinancing your mortgage can be a smart way to lower your monthly payment, secure a better interest rate, shorten your loan term, or tap into your home's equity. However, many homeowners are surprised when they discover that refinancing comes with closing costs. These expenses can add up to thousands of dollars, making it seem like the savings from refinancing may not be worth it. The reality is that while refinance closing costs are a standard part of the process, they are not always set in stone. Depending on your lender, loan type, and financial situation, there are several ways to reduce what you pay or avoid paying everything upfront.

Understanding how refinance closing costs work is the first step toward making a confident financial decision. From lender fees and appraisal costs to title services and government charges, knowing what you're paying for can help you identify opportunities to save. In many cases, comparing multiple lenders, negotiating certain fees, or choosing a no-closing-cost refinance can significantly reduce your out-of-pocket expenses.

What Are Refinance Closing Costs, Exactly?

Refinance closing costs are the fees you pay to set up your new loan and replace your existing mortgage. Think of them as the "cost of doing business" with a lender covering everything from processing your paperwork to verifying your home's value. According to the Consumer Financial Protection Bureau, these costs typically run between 2% and 6% of your loan amount, though the exact number depends on your lender, your state, and your loan size.

Some of the most common fees include:

Origination fee – what the lender charges for processing and underwriting your loan

Appraisal fee – covers the cost of having your home professionally valued

Title search and title insurance – protects against ownership disputes or liens on the property

Credit report fee – a small charge for pulling your credit history

Recording fee – paid to your local government to officially record the new loan

Prepaid items – things like property taxes and homeowners insurance that get set aside in escrow

Not every fee applies to every loan, and not every fee is negotiable but understanding what you're being charged for is the first step to lowering the total bill.

Average Refinance Closing Costs in the U.S.

Here's a general breakdown of what homeowners typically pay. Keep in mind these are national averages your actual costs will vary based on your location, loan amount, and lender.

Fee Type | Typical Cost Range | Who Charges It |

Origination fee | 0.5% – 1% of loan amount | Your lender |

Appraisal fee | $400 – $700 | Independent appraiser |

Title search & insurance | $500 – $1,000+ | Title company |

Credit report fee | $30 – $50 | Credit bureau |

Recording fee | $25 – $250 | Local government |

Attorney/closing fee | $200 – $800 (varies by state) | Attorney or closing agent |

Prepaid escrow (taxes/insurance) | Varies widely | Set aside for you, not a "fee" per se |

On a $300,000 refinance, that often adds up to somewhere between $6,000 and $18,000. That's a big number but as you'll see below, there's a lot you can do to bring it down.

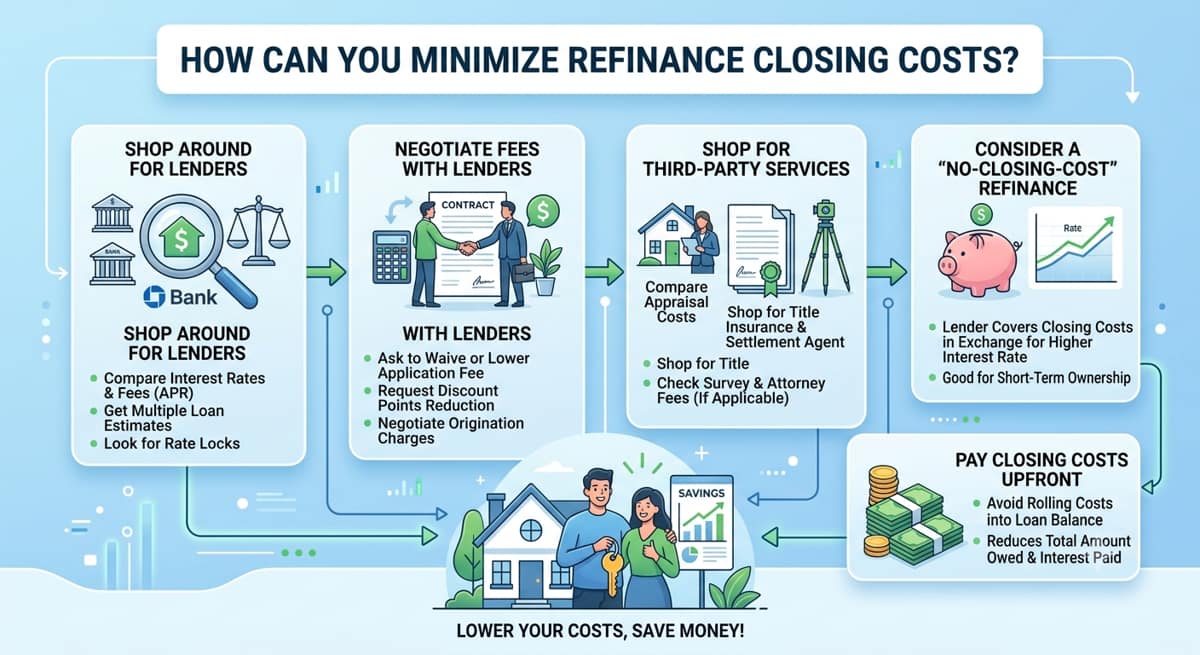

Proven Strategies to Minimize Refinance Closing Costs

The good news is that closing costs aren't a single, unchangeable number. Lenders have some flexibility, some fees can be shopped around, and there are structural choices like how you pay these costs that can make a real difference to your bottom line. Here's where to focus your energy.

Shop and Compare Multiple Loan Estimates

Every lender is legally required to give you a Loan Estimate within three business days of applying. This document breaks your costs into clear sections, so you can compare offers side by side instead of guessing.

Pay close attention to Section A (origination charges) and Section B (services you can't shop for) versus Section C (services you can shop for, like title insurance in some states). Getting Loan Estimates from three or four lenders, banks, credit unions, and independent mortgage advisors often reveals a surprising range in fees for the exact same loan. It only takes a day or two to request these, and the savings can easily be worth the effort.

Negotiate Lender Fees and Ask About Credits

Here's something many homeowners don't realize: lender fees aren't always set in stone. Origination charges, application fees, and processing fees are often negotiable, especially if you have strong credit or you're comparing offers from a competitor. It never hurts to simply ask, "Is there any flexibility here?"

You can also ask your lender about lender credits where the lender covers part of your closing costs in exchange for a slightly higher interest rate. This won't make sense for everyone, but it's worth asking about, especially if you're short on cash right now.

Consider a No-Closing-Cost Refinance

A "no-closing-cost" refinance doesn't mean the costs disappear, it means they're rolled into your loan balance or covered through a higher interest rate instead of being paid upfront.

Pros:

No large out-of-pocket payment at closing

Useful if you don't plan to stay in the home long term

Frees up cash for other needs

Cons:

You'll likely pay a higher interest rate over the life of the loan

Total interest paid over time can be more than if you'd paid costs upfront

Not ideal if you plan to stay in your home for many years

This option comes down to your timeline. If you expect to sell or refinance again within a few years, it can make a lot of sense. If you're planning to stay put for the long haul, paying costs upfront usually saves more money overall.

Improve Your Credit Score Before Applying

Your credit score doesn't just affect your interest rate it also affects certain loan-level pricing adjustments that lenders build into your costs. Generally speaking, the higher your score, the lower your fees and rate tend to be. Paying down credit card balances, correcting any errors on your credit report, and avoiding new debt in the months before you apply can meaningfully lower what you're charged. Even a jump of 20–30 points can move you into a better pricing tier.

Time Your Refinance and Consider Discount Points

Interest rates move daily, and locking in at the right time can save you money on both your rate and, indirectly, your closing costs. You can also choose to pay discount points and an upfront fee that buys down your interest rate. This adds to your closing costs today but lowers your monthly payment going forward.

Whether points make sense depends on how long you plan to keep the loan. If you'll be in the home long enough to recoup the upfront cost through lower payments, points can be a smart trade. If not, skip them.

Roll Closing Costs Into the Loan vs. Paying Upfront

You generally have two choices: pay closing costs out of pocket at signing, or roll them into your loan balance. Here's a simple way to think about it.

Say your closing costs are $8,000. If you pay upfront, your loan balance stays the same, and you keep your monthly payment as low as possible. If you roll that $8,000 into a $300,000 loan, your new balance becomes $308,000 meaning you'll pay interest on that extra amount for the life of the loan, which can add up to more than $8,000 over 30 years.

Rolling in costs makes sense if cash flow is tight right now. Paying upfront makes sense if you have the funds available and want to minimize long-term interest.

Ask About Fee Waivers and Discounts

Many homeowners leave savings on the table simply because they don't ask. Some credit unions waive certain fees for members. Veterans and active-duty service members may qualify for VA funding fee exemptions. Some lenders offer discounts for first responders, teachers, or existing customers. A quick conversation with your lender or advisor about what you might qualify for can lead to real savings.

Calculate Your Break-Even Point Before Deciding

Before committing to any refinance, it's worth doing this simple math: divide your total closing costs by your monthly savings. That tells you how many months it will take to "break even" on the cost of refinancing.

For example, if your closing costs are $6,000 and refinancing saves you $150 a month, your break-even point is 40 months a little over three years. If you plan to stay in your home longer than that, the refinance is likely worth it. If you're planning to move sooner, it may not pay off.

Common Mistakes That Increase Refinance Closing Costs

Only getting one quote – Comparing just one lender means you have no way of knowing if you're overpaying.

Ignoring the Loan Estimate details – Skimming past the fee breakdown means missed opportunities to question or negotiate charges.

Not asking about lender credits or waivers – These savings are rarely offered automatically; you usually have to ask.

Choosing based on interest rate alone – A slightly lower rate with much higher fees can cost more overall.

Rushing the appraisal or title process – Delays and rush fees can add unnecessary costs.

Not checking your credit before applying – Errors or fixable issues on your credit report can quietly push your costs up.

When Does Refinancing Actually Make Sense?

Minimizing closing costs matters, but it's only one piece of the bigger decision. Refinancing tends to make the most sense when you can lower your interest rate by at least half a percent to one percent, when you plan to stay in your home past your break-even point, or when you need to tap into home equity for a specific goal, like consolidating debt or funding a renovation. If you're planning to move in the next year or two, or your current rate is already competitive, it may be worth holding off. A quick conversation with an advisor can help you see the full picture, not just the closing cost line item.

How a Mortgage Advisor Helps You Save on Closing Costs

This is where working with an advisor, rather than going it alone, tends to pay off. A mortgage advisor can pull Loan Estimates from multiple lenders on your behalf, flag fees that are unusually high or negotiable, and help you understand which credits, waivers, or point options actually make sense for your situation. Because advisors work with many lenders rather than just one, they often have visibility into where costs can be trimmed that an individual homeowner comparing one or two offers simply wouldn't see. The goal isn't to push you toward refinancing, it's to make sure that if you do, you're doing it in the way that saves you the most money, both at closing and over the life of the loan.