Refinancing a HELOC can be a practical way to lower your monthly payments, secure a more predictable interest rate, or better manage your overall debt. Whether your draw period is ending, your variable interest rate has increased, or you're looking for a more affordable repayment option, understanding how HELOC refinancing works is the first step toward making a confident financial decision. The right refinancing strategy can help you improve cash flow, simplify your finances, and potentially save money over the life of your loan.

However, refinancing isn't a one-size-fits-all solution. Depending on your financial goals, home equity, credit score, and current mortgage, you may be able to refinance your HELOC into a new HELOC, roll it into a cash-out refinance, replace it with a home equity loan, or combine it with your existing mortgage. Each option comes with its own advantages, costs, and eligibility requirements, making it important to compare them carefully before moving forward.

What Does It Mean to Refinance a HELOC?

Refinancing a HELOC simply means replacing your current home equity line of credit with a new loan that has different hopefully better terms. Instead of continuing to pay off your existing HELOC under its original agreement, you take out a new loan (or a new HELOC) to pay off the old one.

This is different from just renewing a HELOC, which usually means your lender extends your current draw period without changing much else. Refinancing, on the other hand, gives you a fresh start: a new interest rate, a new repayment structure, and sometimes a completely different type of loan altogether.

To understand why this matters, it helps to remember how a HELOC works in the first place. It has two phases: the draw period, when you can borrow and repay funds as needed, and the repayment period, when you can no longer draw funds and must start paying down the balance often with a bigger monthly payment. Because a HELOC is a form of revolving credit, its rate is usually variable, which means your payment can change over time. Refinancing lets you step out of that structure and into something that fits your situation better.

Why Would You Want to Refinance Your HELOC?

There's rarely just one reason homeowners look into refinancing: it's usually a combination of a few pressures building at once.

The most common trigger is entering the repayment period. When the draw period ends, monthly payments often increase significantly because you're now paying both principal and interest instead of interest-only. That jump can catch people off guard.

Rising interest rates are another big one. Since most HELOCs have variable rates, your payment can climb even if your balance hasn't changed. If you're tired of watching your payment fluctuate, locking in a fixed rate through a refinance can bring some peace of mind.

Other common reasons include wanting access to more available credit than your current HELOC allows, or wanting to roll high-interest debt like credit cards into one more manageable payment. If any of this sounds familiar, refinancing might be worth a closer look.

When Is the Best Time to Refinance a HELOC?

There's no single "perfect" moment to refinance, but a few signs tend to show up when the timing is right.

If your draw period is ending soon, that's often a natural point to explore refinancing before your payment jumps. Similarly, if interest rates have dropped since you first opened your HELOC, refinancing into a lower rate could save you real money over time.

It's also worth checking if your home's value has gone up more equity can open the door to better terms or if your credit score has improved since you took out the original HELOC, which could qualify you for more favorable rates.

On the flip side, if your current payment is becoming genuinely hard to manage, that's a strong signal to start looking at your options sooner rather than later. Rates and home values shift over time, so rather than trying to time the market perfectly, focus on whether refinancing solves a real problem you're facing right now.

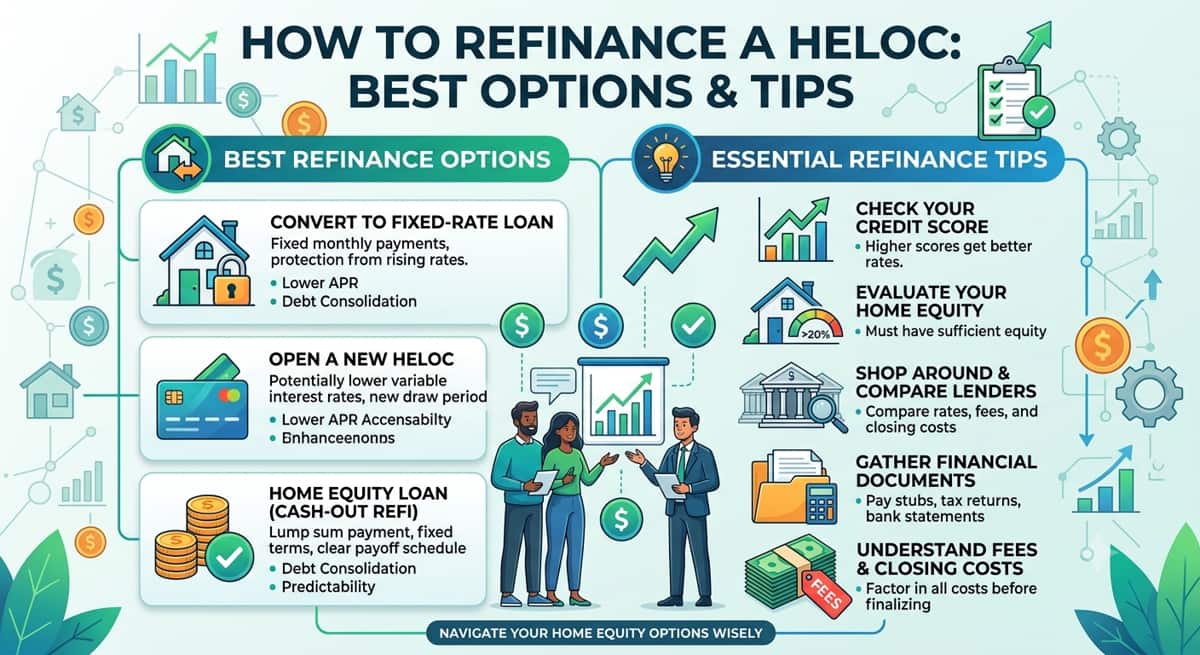

What Are the Best Options for Refinancing a HELOC?

There isn't a one-size-fits-all answer here; the right option depends on your goals, your equity, and how you want your payments to look going forward. Here are the four most common paths.

Refinance Into a New HELOC This makes sense if you still want the flexibility of a revolving line of credit but want better terms: a lower rate, a longer draw period, or a higher credit limit. It's a good fit if your original HELOC is ending its draw period but you still want ongoing access to funds.

Cash-Out Refinance This option replaces both your first mortgage and your HELOC with one new, larger mortgage. You get a single monthly payment instead of two, and depending on rates, it can simplify your finances significantly. It works well if you want to consolidate everything into one predictable loan.

Home Equity Loan Unlike a HELOC, a home equity loan gives you a lump sum with a fixed rate and fixed monthly payments. This is a solid choice if you want predictability and you're not planning to borrow more in the future, you just want to pay off what you owe on more stable terms.

Traditional Mortgage Refinance This means refinancing your primary mortgage and using part of the funds to pay off your HELOC, essentially rolling everything into one new mortgage. It's worth exploring if your first mortgage rate is also outdated and you'd benefit from refinancing both at once.

Option | Rate Type | Best For |

New HELOC | Usually variable | Wanting continued flexible access to funds |

Cash-Out Refinance | Usually fixed | Combining mortgage + HELOC into one payment |

Home Equity Loan | Fixed | Predictable payments, no more borrowing needed |

Traditional Mortgage Refinance | Fixed or variable | Improving your first mortgage rate too |

How Do You Refinance a HELOC Step by Step?

Refinancing might sound complicated, but it generally breaks down into five manageable steps.

Review your current HELOC. Look at your remaining balance, your current rate, and when your draw period ends. This gives you a clear starting point.

Check your home equity. Get an idea of your home's current value versus what you owe. This determines what refinancing options are realistically available to you.

Compare lenders and rates. Don't just go with your current lender by default shop around. Rates, fees, and terms can vary quite a bit between lenders.

Gather required documents. Most lenders will ask for proof of income, tax returns, current mortgage statements, and information about your debts.

Apply and close the new loan. Once you've chosen a lender and option, you'll go through underwriting and closing, similar to your original mortgage process.

Taking it one step at a time makes the whole process feel a lot less overwhelming.

What Requirements Do You Need to Refinance a HELOC?

Every lender has its own specific criteria, but most will look at a similar set of factors.

Credit score: Higher scores generally unlock better rates with credit score, though exact thresholds vary by lender. Even if your credit isn't perfect, you may still have options.

Home equity: Lenders typically want to see a healthy amount of equity in your home, often expressed as a loan-to-value ratio how much you owe compared to what your home is worth.

Debt-to-income ratio: This compares your monthly debt payments to your income. A lower ratio generally makes approval easier.

Income verification: Be ready to show pay stubs, tax returns, or other proof of steady income.

These are general guidelines actual requirements vary from lender to lender, so it's worth having a conversation with a mortgage advisor about where you personally stand.

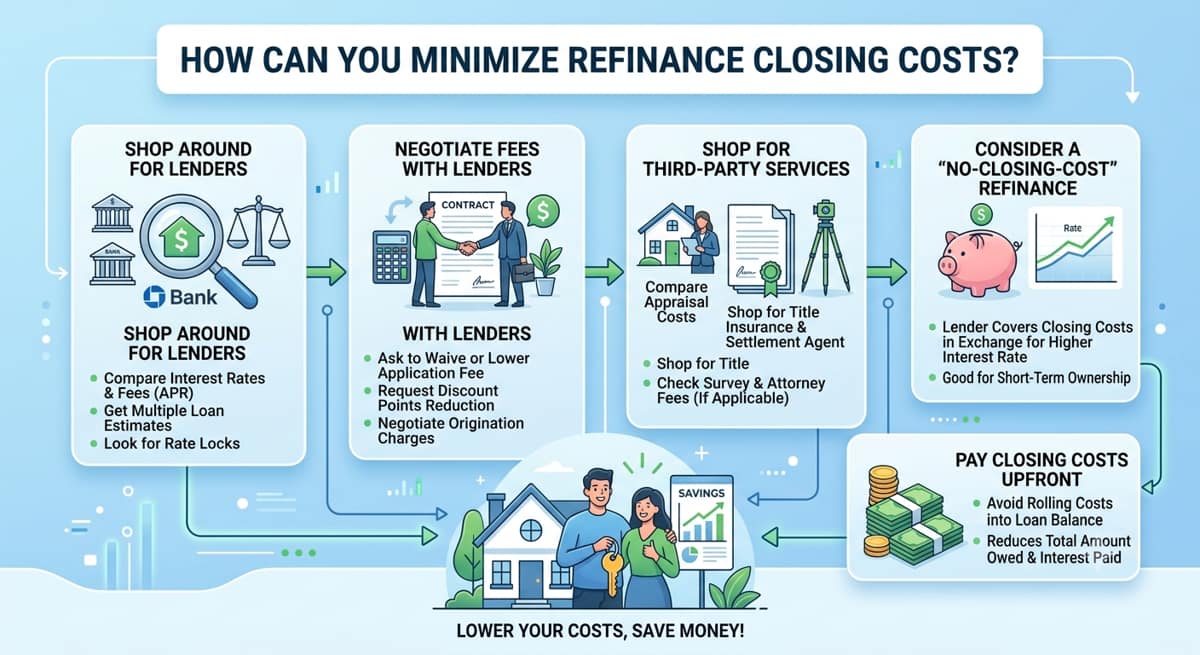

How Much Does It Cost to Refinance a HELOC?

Refinancing isn't free, so it's worth understanding the costs before you commit.

Closing costs typically run as a percentage of the loan amount, and they can include a variety of fees bundled together. Appraisal fees are common too, since the lender needs to confirm your home's current value. On top of that, you may see other lender fees, such as origination fees or title fees.

Exact costs vary quite a bit depending on your lender, your location, and your loan amount, so it's best to get a detailed quote from a few different lenders rather than relying on a single number. A good advisor can walk you through exactly what you're being charged and why.

What Are the Pros and Cons of Refinancing a HELOC?

Like most financial decisions, refinancing has upsides and trade-offs worth weighing honestly.

Benefits:

Potentially lower interest rate

Predictable, fixed monthly payments (depending on the option you choose)

Ability to consolidate debt into one payment

Access to more available credit if needed

Potential drawbacks:

Closing costs can add up

You may be resetting your loan term, meaning more years of payments overall

There's a risk of borrowing more than you actually need

Your home remains the collateral, so missed payments carry real consequences

Weighing both sides honestly rather than only focusing on the potential savings helps you make a decision you'll feel good about later.

What Mistakes Should You Avoid When Refinancing a HELOC?

A few common missteps can turn what should be a smart financial move into a frustrating one.

Choosing based only on interest rates. A low rate with high fees might cost more overall than a slightly higher rate with lower fees.

Ignoring fees. Closing costs, appraisal fees, and origination fees all add up make sure you understand the full picture before signing anything.

Borrowing more than necessary. Just because you're approved for a certain amount doesn't mean you should take all of it.

Not comparing multiple lenders. Sticking with your current lender out of convenience can mean leaving better terms on the table elsewhere.

Taking a little extra time upfront to avoid these mistakes can save you real money down the road.

Can You Refinance a HELOC With Bad Credit?

If your credit isn't where you'd like it to be, refinancing can feel out of reach but it's often still possible. It's an understandably stressful situation, and you're not the only one facing it.

Some homeowners find success through credit unions, which sometimes offer more flexible underwriting than larger banks. Portfolio lenders who keep loans in-house rather than selling them may also have more room to work with borrowers who don't fit a standard box. Adding a co-signer with stronger credit is another path some homeowners explore.

That said, expect to see higher rates and a likely need for more equity as a cushion. Rather than assuming refinancing isn't an option, it's worth having an honest conversation with a mortgage advisor who can walk you through what's realistically available based on your full financial picture not just your credit score.

Is Refinancing a HELOC Worth It?

This ultimately comes down to your own numbers and plans, not a generic rule of thumb.

Start by figuring out your break-even point how long it will take for your monthly savings to outweigh the closing costs. Then think about how long you plan to stay in your home; if you're moving in a year or two, refinancing may not pay off in time. Finally, look at how much your rate would actually improve a small difference may not be worth the hassle, while a larger one often is.

If the math works in your favor and your monthly payment situation is genuinely improving, refinancing is usually worth it. When in doubt, a licensed mortgage advisor can run these numbers with you and help you see the full picture clearly.

Final Thoughts

Refinancing a HELOC isn't about chasing the lowest possible rate it's about finding the option that actually fits your life, your goals, and your budget. Whether that's a new HELOC, a cash-out refinance, a home equity loan, or rolling everything into your primary mortgage, the right choice depends on your specific numbers and plans.

If you're not sure where to start, that's exactly what a mortgage advisor is for. Reach out to discuss your situation and get a clear, personalized look at what refinancing could mean for you.