The homebuying process is exciting, but mortgage sourcing often feels complicated. Among the most common decisions home buyers must make is between a traditional 30-year fixed-rate mortgage or an adjustable-rate mortgage (ARM). On one hand these options may look like a good line of attack to me. A 30-year fixed mortgage loan gives you a reliable amount to budget towards each month for many, many years but an ARM typically has the lowest initial interest rate which lowers your monthly housing costs. The trick is figuring out which option fits your financial strategy, timeframe and risk tolerance.

The correct decision involves lots of criteria apart from interest rates in October 2023. This means you'll need to think about your intended stay in the house, how likely it is that your finances will change, and how much of a buffer your budget has if rates rise later. What saves you money in the early years can cost more over the life of the loan, while a fixed-rate mortgage with a higher monthly payment might give some peace of mind that could be worth its weight in dollars.

What Is a 30-Year Fixed-Rate Mortgage?

A 30-year fixed mortgage is exactly that; you borrow money for 30 years by loan, and the interest rate you lock in on day one doesn't change over the life of the loan. It will not change your principal and interest payment if five years from now the market crashes or twenty-five years later when it rises.

This is the loan that most Americans envision when they hear "getting a mortgage," and there are good answers as to why it's so familiar. It's predictable. This makes it considerably easier to build a household budget around, as you know exactly how much is owed every month.

Pros of a 30-Year Fixed Mortgage

The biggest advantage is peace of mind. Your payment today is your payment in year 20, so there's no guessing game if interest rates climb. That predictability makes it easier to plan for other goals, like saving for retirement or your kids' education, without worrying that your housing cost will suddenly jump. It's also a smart hedge if you plan to stay in your home long-term, since you're protected no matter what the broader rate environment does.

Cons of a 30-Year Fixed Mortgage

That stability comes at a price. Fixed rates typically start higher than the introductory rate on an adjustable loan, so your initial payment may be more than it would be with an ARM. You'll also build equity a little more slowly in the early years, since more of each payment goes toward interest rather than principal at the start of the loan.

What Is an Adjustable-Rate Mortgage (ARM)?

With an adjustable-rate mortgage, the mortgage is fixed for a period of time under an introductory rate before it adjusts periodically after that (and in relation to the market). They are often referred to as 5/1, 7/1 or 10/1 ARMs. The first number indicates how long that rate is fixed, while the second number explains how often it can be adjusted afterwards. A 7/1 ARM, for instance, locks your rate in for seven years then can adjust once every 12 months thereafter.

After this introductory period expires, your new rate will be based on a financial index plus a specified margin and is often characterized by rate caps that can delineate how much it may rise at one time or during the duration of the loan.

Pros of an ARM

The main appeal is a lower starting rate, which means a lower monthly payment in those early years compared to a fixed loan. That can free up cash flow for other priorities, or simply make homeownership more affordable right now. ARMs tend to make the most sense for people who know they won't be in the home long-term, like a family expecting to relocate for work in five years, since they may sell or refinance before the rate ever adjusts.

Cons of an ARM

The trade-off is uncertainty. Once the fixed period ends, your payment can go up, sometimes by a noticeable amount, depending on where rates are at the time. Even with rate caps in place, that kind of payment shock can strain a budget if you're not prepared for it. ARMs also come with more moving parts, like understanding your index, margin, and adjustment caps, which makes them a bit harder to plan around than a simple fixed rate.

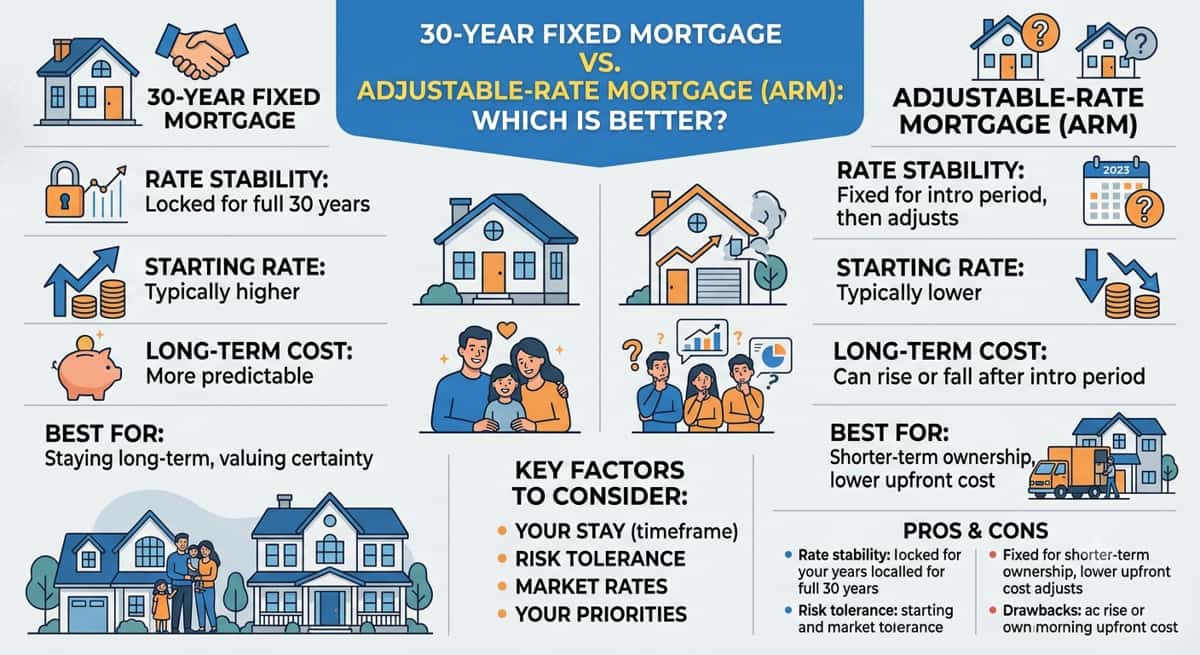

30-Year Fixed vs. ARM: Side-by-Side Comparison

Feature | 30-Year Fixed | Adjustable-Rate Mortgage (ARM) |

Rate stability | Locked for the full 30 years | Fixed for an intro period, then adjusts |

Starting rate | Typically higher | Typically lower |

Long-term cost | More predictable | Can rise or fall after intro period |

Best for | Staying long-term, valuing certainty | Shorter-term ownership, lower upfront cost |

Refinance flexibility | Can refinance anytime rates improve | Often refinanced before adjustment period ends |

Risk level | Low | Moderate to higher, depending on rate caps |

In plain terms: a fixed-rate mortgage offers a steady, unchanging payment for the life of the loan, while an ARM offers a lower payment now in exchange for the possibility of a higher one later. Neither is automatically "better." It depends on how long you plan to stay put and how much uncertainty you're comfortable carrying.

How Each Option Affects Refinancing and Home Equity Plans

Your mortgage type doesn't just affect your monthly payment, it also shapes your options down the road, especially if refinancing or borrowing against your home's equity is part of your longer-term plan.

If you have a fixed-rate mortgage, refinancing is usually straightforward: you can look at refinancing whenever rates drop enough to make it worthwhile, without worrying about a ticking clock. A cash-out refinance, where you tap into your equity for renovations, debt consolidation, or other big expenses, tends to be simpler to evaluate too, since your baseline payment has been steady and predictable.

With an ARM, timing matters more. Many borrowers plan to refinance before their adjustment period kicks in, especially if rates are expected to rise. If you're also considering a home equity loan on top of your mortgage, keep in mind that HELOCs typically carry variable rates of their own, so pairing one with an ARM means more of your overall debt is exposed to rate changes at once.

When Refinancing from an ARM to a Fixed Rate Makes Sense

If your introductory period is ending soon and current fixed rates look reasonable, locking in that certainty can protect you from an unpredictable jump. This move tends to make the most sense if your plans have changed, say, you originally expected to move but now plan to stay long-term, or if you'd simply rather stop watching rate forecasts and settle into a stable payment.

When Refinancing from a Fixed Rate Into an ARM Makes Sense

This is less common, but it does happen. Some homeowners refinance from a fixed rate into an ARM if they need to lower their monthly payment in the near term, perhaps due to a temporary income change, and they're confident they'll sell or refinance again before the adjustable period begins. It's a strategy that works best with a clear, realistic exit plan.

Which Is Better for You? Key Factors to Consider

There's no universal winner here, but a few questions can help point you in the right direction.

How long do you plan to stay in the home? If you're settling in for the long haul, the certainty of a fixed rate often outweighs the short-term savings of an ARM. If you know you'll move within a handful of years, an ARM's lower starting payment could work in your favor.

How much risk can you comfortably handle? If a future payment increase would seriously stretch your budget, that's an important signal. A fixed rate removes that variable entirely.

What's happening with rates right now? The current rate environment matters, but it shouldn't be the only factor. A mortgage advisor can help you look at where rates stand today and what that means for your specific numbers, rather than relying on headlines alone.

Are you optimizing for the lowest payment today, or the most predictable payment over time? Both are valid goals. The right loan is the one that matches what actually matters most to you and your household.

Common Mistakes Borrowers Make When Choosing Between Fixed and ARM Loans

A few missteps come up again and again. The most common is not being realistic about how long you'll actually stay in the home; plans change, and "we'll definitely move in five years" doesn't always hold up. Another is focusing only on that attractive introductory ARM rate without looking at the rate caps and understanding what the worst-case payment could look like.

Some borrowers also compare loans based on the first year's payment alone, rather than the total cost over the years they expect to hold the loan. And perhaps the biggest mistake is skipping a conversation with a mortgage advisor before signing anything. A quick review of your specific numbers can catch issues a rate quote alone won't show you.

Talk to a Licensed Mortgage Advisor Before You Decide

Selecting a mortgage is one of the most significant financial decisions you will likely make, and which option works best for you rests on your income, goals, budget and outlook. We can use online calculators and general advice to get an understanding, but they never take into account your personal situation. A licensed mortgage advisor can walk you through your unique situation, lay out possible options for a loan, compare rates/terms as well as the long-term costs associated with each choice. They also spot opportunities that you may not have otherwise identified, whether you're a first-time home buyer, refinancing your current property or investing in real estate. If you take a minute to speak with a professional before signing any loan paperwork it could help you avoid costly pitfalls and make a better overall decision. Now having a specialist guiding you, you will not only know for sure that the mortgage you pick actually helps your needs now and in the future but can also rest assured knowing that every step of the home financing process is being handled by an expert.