If you own a home, you are likely sitting on a hidden financial superpower: your equity. Over the last few years, home values across the country have climbed steadily. If you have been watching your home's value rise while your credit card balances grow or your kitchen grows outdated, you might be wondering how to tap into that wealth without selling the roof over your head.

That is exactly where a cash-out refinance comes in.

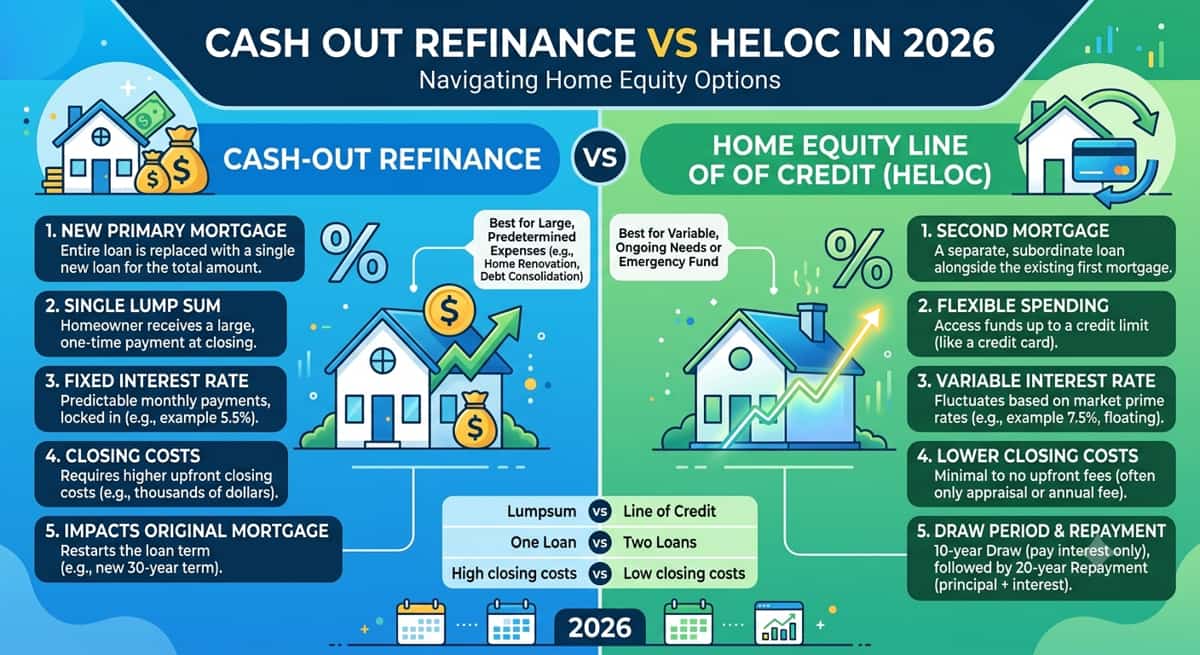

A cash-out refinance is a mortgage refinancing option where you replace your current home loan with a new, larger mortgage, allowing you to take the difference between the two loans in cash.

Essentially, you are rewriting your original mortgage, keeping what you owe on the house, adding an extra amount on top, and walking away with a lump sum of cash at closing.

As a licensed mortgage advisor, my goal isn't just to help you get a loan, it is to make sure your home equity works safely and strategically for your family's long-term financial health. Let’s look at how this works in real life.

How Does a Cash-Out Refinance Work?

The Basic Mechanics: Old Loan Out, New (Bigger) Loan In

Think of it like this: you pay off your current mortgage completely and start a brand-new one but the new one is for more than what you owed. The lender pays off your old loan first, then hands you the leftover amount in cash, usually a few days after closing.

Your new loan comes with its own interest rate, monthly payment, and loan term. That part matters more than people expect, because even if you get a great rate, you're starting the clock over on a 15- or 30-year loan. We'll get into why that's worth thinking through later on.

Where the Extra Cash Actually Comes From: Your Home Equity

The money isn't coming out of thin air, it's coming out of the equity you've already built. Equity is just the gap between what your home is worth and what you still owe on it.

Here's a simple way to picture it. Say your home is worth $400,000 and you owe $200,000 on your current mortgage. That means you have $200,000 in equity. Most lenders will let you borrow up to 80% of your home's value with a conventional loan, which in this case is $320,000. Subtract the $200,000 you still owe, and you'd walk away with around $120,000 in cash, minus closing costs.

The math worked out, but only because they were comfortable with the new, larger monthly payment. That's the part that's easy to overlook when you're focused on the lump sum.

Cash-Out Refinance vs. Other Ways to Tap Home Equity

A cash-out refinance isn't your only option for getting at your equity. Here's how it stacks up against the two most common alternatives.

Cash-Out Refinance vs. Home Equity Loan

A home equity loan is a separate loan on top of your existing mortgage. You keep your current mortgage exactly as it is and take out a second loan against your equity. A cash-out refinance, on the other hand, replaces your mortgage entirely with one new loan.

Cash-Out Refinance vs. HELOC

A HELOC (home equity line of credit) works more like a credit card backed by your home. You get a credit limit you can draw from as needed, rather than a single lump sum, and your original mortgage stays untouched.

Cash-Out Refinance | Home Equity Loan | HELOC | |

How you get the money | One lump sum | One lump sum | Draw as needed, like a credit line |

What happens to your current mortgage | Replaced entirely | Stays in place | Stays in place |

Interest rate type | Usually fixed | Usually fixed | Usually variable |

Best for | Large amounts, especially if you can also lower your rate | A fixed amount with predictable payments | Ongoing or uncertain expenses |

Closing costs | Similar to a full mortgage | Generally lower | Often lower, sometimes minimal |

If you're trying to decide between these, it usually comes down to whether you want one combined payment (cash-out refi) or want to leave your current mortgage rate untouched (home equity loan or HELOC).

Who Qualifies for a Cash-Out Refinance?

Every lender has its own specific rules, but here's what most borrowers need to meet:

Enough equity - Conventional and FHA loans generally cap your new loan at 80% of your home's value, meaning you'll need to keep at least 20% equity. VA loans are more flexible and can go up to 90–100% in some cases.

A qualifying credit score - Conventional loans typically start around 620, though a higher score gets you a better rate. FHA loans tend to be more forgiving of lower scores.

A reasonable debt-to-income (DTI) ratio - Lenders look at how much of your monthly income already goes toward debt payments.

A seasoning period - Most loans require you to have had your current mortgage for at least six to twelve months before you can do a cash-out refinance.

Sufficient income and employment history - Just like your original mortgage, you'll need to show you can comfortably handle the new payment.

These requirements shift depending on whether you go conventional, FHA, or VA, and individual lenders can be stricter than the baseline rules.

What Can You Use a Cash-Out Refinance For?

There's no restriction on how you spend the money once it's in your account, but some uses tend to make more financial sense than others. Common reasons homeowners do this include:

Paying off high-interest debt, like credit cards or personal loans, by rolling it into a lower mortgage rate

Home improvements or repairs, especially ones that maintain or add to the home's value

Education costs, such as tuition for yourself or a family member

A down payment on an investment property or second home

That said, it's worth being honest about the riskier end of the spectrum too: using this money for discretionary spending like vacations or non-essential purchases means you're paying it back, with interest, over potentially 30 years, secured by the house you live in. It's worth pausing on that trade-off before committing.

Pros and Cons of a Cash-Out Refinance

Potential Benefits

Access to a large amount of cash, often at a lower interest rate than credit cards or personal loans

One single, predictable monthly payment instead of juggling multiple debts

Possible mortgage interest tax benefits depending on how the funds are used worth confirming with a tax professional

An opportunity to also improve your mortgage rate or terms if rates have dropped since you bought

Risks and Trade-Offs

You're increasing your total mortgage debt and reducing the equity cushion in your home

Your loan term often resets, which can mean paying more in interest over the life of the loan even if your rate is lower

Closing costs apply just like a regular mortgage, typically 2% to 6% of the loan amount

Because this is a secured loan, falling behind on payments puts your home at risk of foreclosure this isn't unsecured debt like a credit card

This last point is the one I want every homeowner to sit with before moving forward: the equity you're tapping is real money tied to your home, and pulling too much out can leave you with little cushion if your home's value dips or your situation changes.

How Much Does a Cash-Out Refinance Cost?

Closing costs on a cash-out refinance typically run between 2% and 6% of your new loan amount, covering things like the appraisal, title work, lender fees, and origination charges. On a $300,000 loan, that could mean anywhere from roughly $6,000 to $18,000, though many lenders allow you to roll some of these costs into the loan itself rather than paying out of pocket.

You'll also need a new home appraisal, since your loan amount depends on your home's current market value, not what you paid for it. And if your new loan-to-value ratio ends up above 80%, you may face private mortgage insurance (PMI) on a conventional loan, which adds to your monthly cost.

One more thing worth knowing: cash-out refinance rates tend to run slightly higher than a standard rate-and-term refinance, since lenders view the larger loan amount as more risk.

Is a Cash-Out Refinance Right for You?

Before moving forward, it helps to be honest with yourself about a few things:

Can you comfortably afford the new monthly payment not just today, but if your income changed?

Are you using the funds for something that improves your financial position long-term, like eliminating high-interest debt or increasing your home's value, rather than short-term wants?

How long do you plan to stay in the home? If you're moving in a couple of years, the closing costs may not be worth it.

Have you compared this against a home equity loan or HELOC to see which actually costs less for your specific goal?

Does your current mortgage rate matter here? If you have an unusually low rate already, refinancing the entire balance to access a smaller amount of cash might not make sense; a home equity loan could preserve your existing rate.

The homeowners who come out ahead are the ones who treat this as a financial tool with a clear purpose, not just a way to free up cash because it's available. The ones who run into trouble are usually the ones who didn't fully think through the new payment before signing.

How a Mortgage Advisor Can Help You Decide

This is exactly the kind of decision where a second set of eyes pays off. A mortgage advisor can shop your scenario across multiple lenders instead of you applying one at a time, compare what a cash-out refinance actually costs you against a home equity loan or HELOC side by side, and calculate your break-even point meaning how long it takes for the benefits to outweigh the closing costs.

Beyond the math, a good advisor will ask the harder question: does this actually move you toward your goals, or does it just feel good right now? That's the kind of guidance that's hard to get from a calculator alone, and it's the difference between a refinance that helps you and one you regret in three years.

If you're weighing this decision, schedule a free consultation and we can walk through your specific numbers together.

Final Thoughts

A cash-out refinance is one of the most powerful tools you have to take control of your financial future, but it works best when you use it with a clear purpose. Whether you are wiping out high-interest credit cards, funding a dream renovation, or handling life's unexpected expenses, tapping into your home equity can give you the clean slate and breathing room you need.

Because your home is your most important asset, it pays to look at the numbers carefully. Professionals can help you weigh the pros and cons based on your unique situation. Reach out today for a personalized equity assessment, and we will look at your current home value, calculate your exact options, and see how much your equity can do for you.