Starting a business often feels like a race to find the right fuel. While many entrepreneurs immediately look toward Small Business Administration (SBA) loans or private investors, the most powerful source of startup capital might actually be the roof over your head. Leveraging your home equity and the difference between your home’s market value and your remaining mortgage balance for commercial growth is a strategic move that high-net-worth founders have used for decades to maintain full ownership of their companies.

The current financial landscape has made this path even more attractive. While SBA loans are excellent, they often come with rigorous paperwork, high "goodwill" fees, and lengthy approval wait times that can stall a launch. In contrast, using your home as a financial tool can provide lower interest rates and faster access to cash. As a Mortgage Consultant with years of experience helping homeowners navigate refinancing and equity access, I’ve seen firsthand how a well-structured home equity strategy can provide the "seed money" necessary to turn a side hustle into a primary income stream. By treating your home as a strategic asset rather than just a residence, you can bypass the shark-tank mentality of outside investors and remain the sole pilot of your professional destiny.

Understanding Home Equity: How Much Capital is Hiding in Your House?

Before you can use your home to fund a business, you need to know exactly how much "hidden" money you actually have. Home equity isn't just a buzzword; it is a straightforward calculation of your ownership stake in your property. To find yours, take the current market value of your home and subtract the remaining balance on your mortgage. If your house is worth $500,000 and you owe $300,000, you have $200,000 in equity.

However, having $200,000 in equity doesn't mean you can walk into a bank and withdraw the full amount. Lenders generally follow the "80% Rule." This means they prefer your total debt the old mortgage plus the new loan, to stay under 80% of the home's total value. This is known as your Loan-to-Value (LTV) ratio. Using the same $500,000 home, 80% of the value is $400,000. Since you already owe $300,000, your "usable" equity for a business startup would be $100,000.

To confirm these numbers, a lender will require a professional asset valuation, commonly known as an appraisal. An appraiser will visit your home to ensure the market value is accurate. Once the value is set, the lender acting as a lien holder uses the home as security for the loan. Understanding these limits early helps you set a realistic budget for your new venture without overextending your personal finances.

Comparing Your Options: HELOC vs. Cash-Out Refinance vs. Home Equity Loan

Choosing the right way to access your equity depends on how you plan to spend the money for your business. There are three main paths, each with its own set of rules and benefits.

The HELOC (Home Equity Line of Credit) – Flexibility for Startups

A HELOC works much like a credit card with a high limit. Instead of getting all the money at once, you are given a line of credit that you can draw from whenever you need it. This is perfect for startups that have unpredictable costs, like buying inventory or paying for marketing as needed. You only pay interest on the amount you actually use. Most HELOCs have a "draw period" (usually 10 years) where you might only be required to pay the interest, followed by a "repayment period" where you pay back both the principal and interest. This flexibility can be a lifesaver during the lean first months of a new business.

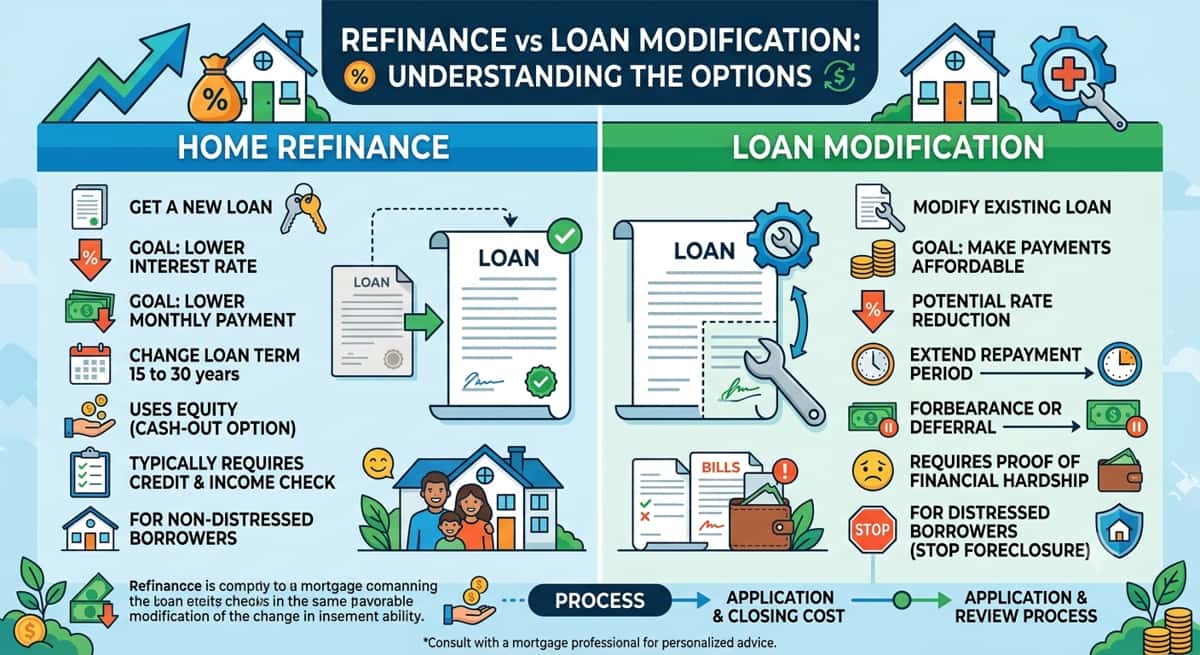

Cash-Out Refinance – Locking in Rates and Consolidating Debt

A cash-out refinance replaces your current mortgage with a completely new, larger one. You pay off your old loan and keep the difference in cash. This is a popular choice if current mortgage interest rates are lower than the rate on your original loan. It allows you to wrap your home and business startup costs into a single monthly payment with a long repayment term, often 30 years. Because the debt is spread out over such a long time, your monthly payments may be more manageable than other types of loans. It’s also an effective way to simplify your finances by having just one lender to deal with.

Home Equity Loan – Fixed Predictability for Lump Sum Costs

If you know exactly how much your business needs such as $50,000 for specialized equipment or a franchise fee a home equity loan is often the best fit. Unlike a HELOC, you receive a single lump sum of cash on day one. These loans usually come with a fixed interest rate, meaning your monthly payment will never change. This predictability makes it much easier to create a business budget because you know exactly what your debt costs will be for the life of the loan. It’s a "set it and forget it" option that protects you from rising interest rates in the future.

Quick Comparison Table

Feature | HELOC | Cash-Out Refinance | Home Equity Loan |

How you get paid | As needed (Credit line) | One-time lump sum | One-time lump sum |

Interest Rate | Usually Variable | Usually Fixed | Usually Fixed |

Monthly Payment | Changes with balance/rate | Stays the same | Stays the same |

Best For | Ongoing expenses | Large capital & lower rates | Single, known startup costs |

Tax Potential | May be deductible* | May be deductible* | May be deductible* |

*Note: Tax deductibility depends on how the funds are used; always check with a tax professional regarding business use of home funds.

The Financial Risks: Is Your Home Worth the Business Risk?

Using your home to fund a business is a bold move that can lead to great success, but it comes with a reality check that every founder must face. When you take out a home equity loan or a HELOC, your house serves as collateral. This means you are giving the lender a legal right to your property to ensure the debt is paid.

The Critical Warning: Foreclosure Risk

The most significant risk is straightforward: if your business struggles and you cannot make your loan payments, you could lose your home. Unlike a standard business loan where a company failure might lead to bankruptcy for the business alone, a home equity-backed venture ties your family’s housing directly to your profit and loss statement. If the business fails to generate enough cash to cover the new mortgage costs, you face the very real possibility of foreclosure.

Recourse vs. Non-Recourse Debt

In the world of lending, most home equity products are considered "recourse" debt. This means that if you default and the sale of the house doesn't cover the full amount you owe, the lender can still come after your other assets or bank accounts to make up the difference. You are essentially providing a personal guarantee with your most valuable asset.

Strategies to Lower Your Risk

To protect yourself, it is vital to keep your personal and business finances as separate as possible:

Build a Safety Net: Never use 100% of your available equity. Leave a "buffer" for home repairs or personal emergencies.

Separate Your Credit: As soon as your business has the capital it needs, start building business credit under its own Tax ID (EIN). This helps you eventually move away from relying on personal assets.

Create a Realistic Exit Plan: Know exactly how you will pay back the loan if the business doesn't hit its targets in the first year.

Before signing, ask yourself: If my business takes twice as long to become profitable, can I still afford these monthly payments? If the answer is no, you may want to reconsider the amount you are borrowing.

Step-by-Step: How to Qualify for Equity Financing as a Founder

Getting approved for a home equity loan while starting a business requires proving to a lender that you are a "safe" borrower. Since you are essentially asking for a second mortgage, the bank will put your finances through a rigorous review process known as underwriting. Here is exactly what you need to have ready.

Credit Score Requirements

While you can technically find loans with lower scores, a FICO score of 680 or higher is generally the "magic number" for competitive rates in 2026. Lenders view your credit score as a snapshot of your financial responsibility. If your score is above 720, you’ll likely unlock the lowest interest rates and higher borrowing limits. If your score is on the edge, consider paying down small credit card balances a month before applying to give your numbers a quick boost.

Debt-to-Income (DTI) Ratios

Lenders use your DTI to see if you can handle another monthly payment. They calculate this by adding up all your monthly debt obligations (like your current mortgage, car loans, and credit cards) plus your potential new equity loan payment, and then dividing that by your gross monthly income.

Lenders generally want to see a DTI of 43% or less. If you are still working your "day job" while launching your business, lenders will prioritize that stable income. Most mainstream lenders will not count "projected" business income money you expect the new business to make until you have at least two years of proven earnings from that venture.

Documentation Checklist

To speed up the Verification of Income (VOI), have these documents organized:

Tax Returns: Your last two years of personal and (if applicable) business federal tax returns.

Proof of Income: Your two most recent pay stubs and W-2 forms. If you’ve already started the business, provide 1099s or a year-to-date Profit and Loss (P&L) statement.

Business Plan: While not always required for the loan itself, having a solid plan shows the lender you are a serious founder with a clear path to repayment.

Bank Statements: Usually the last two to three months of statements for all your checking and savings accounts.

Tax Implications for Entrepreneurs (Consult Your CPA)

Understanding how the IRS treats your home equity loan is vital when you are using those funds for a business. While the interest on a standard mortgage is often deductible, the rules for home equity changed significantly with the Tax Cuts and Jobs Act (TCJA). These rules remain in effect through 2026 due to subsequent updates like the One Big Beautiful Bill Act (OBBBA), making it essential to understand the "use of proceeds" rule.

Home Improvements vs. Business Capital

The IRS makes a sharp distinction based on what you do with the money. Under current law, you can only deduct the interest on a home equity loan or HELOC if the funds are used to "buy, build, or substantially improve" the home that secures the loan. If you use the cash to renovate your kitchen, the interest may be deductible. However, if you use that same cash as capital to start a business such as buying inventory, renting an office, or hiring staff the interest is generally not deductible as mortgage interest on your personal tax return.

A Potential Business Deduction

There is a silver lining for entrepreneurs. While you might not be able to claim the interest as a personal mortgage deduction, you may be able to deduct it as a business expense if the loan is used exclusively for your trade or business. This requires meticulous record-keeping and a clear "paper trail" showing that the loan proceeds were deposited into a business account and used for business-only costs.

Expert Note: Tax laws are complex and vary based on your total debt (the current $750,000 limit for combined mortgage debt) and your filing status. This section provides general financial guidance; you should always consult with a qualified CPA or tax professional to see how these rules apply to your specific startup situation.

Case Study: From Equity to Exit

To see how this works in the real world, let’s look at the story of Sarah, a software developer who wanted to turn her side project, a specialized scheduling app for clinics into a full-time business. Sarah owned a home worth $600,000 and owed $350,000 on her mortgage.

Instead of giving up 20% of her company to an outside investor for $100,000, Sarah opened a $100,000 HELOC. Because her credit was strong, her interest rate was 8%.

The Growth Strategy

Sarah didn’t spend the money all at once. Over the first year, she drew $50,000 to hire a part-time salesperson and run targeted digital ads. This investment allowed her to grow her subscriber base from 10 clinics to 150. Her monthly business revenue jumped from $2,000 to $15,000.

Calculating the ROI

Sarah’s "cost of capital" was the 8% interest she paid on the money she borrowed. However, her business was growing at a rate of over 100% per year. By using her home equity, she kept 100% ownership of her company. When she eventually sold the business two years later for $1.2 million, she simply paid off the $100,000 HELOC balance from the sale proceeds.

The Mortgage Professional’s Perspective

What made Sarah's plan work was her discipline. She used a HELOC because she only wanted to pay interest on the money as she needed it, rather than taking a large lump sum and paying interest on the full amount from day one. She also ensured her "day job" covered her basic mortgage payments until the business revenue was high enough to take over the debt service. By leveraging her home, she turned a residential asset into a million-dollar exit.

Alternatives to Using Home Equity

While your home is a powerful financial tool, it isn't the only way to fund a dream. Depending on your risk tolerance and the type of business you are starting, one of these alternatives might be a better fit.

SBA 7(a) Loans

The Small Business Administration (SBA) offers the 7(a) loan program, which is the gold standard for small business financing. These loans are partially guaranteed by the government, which allows banks to offer competitive rates to businesses that might not otherwise qualify. The downside? The paperwork is extensive, and you often still have to provide a personal guarantee, which could include your home anyway.

401(k) Business Financing (ROBS)

A "Rollover for Business Startups" (ROBS) allows you to use your retirement funds to start a business without paying early withdrawal penalties or taxes. You essentially use your 401(k) to buy stock in your own new company. This is a "debt-free" way to start, but you are risking your future retirement savings instead of your current home.

Angel Investors vs. Bootstrapping

If you have a high-growth idea, an angel investor might give you cash in exchange for a piece of your company. You don't have to pay the money back if the business fails, but you do lose a percentage of your future profits. On the other hand, "bootstrapping" means growing slowly using only the money you earn from sales. It’s the safest route, but also the slowest.

Why Equity is Often Cheaper (But Riskier)

Home equity is usually the cheapest capital available because it is secured by real estate, leading to much lower interest rates than unsecured business credit cards or private loans. However, it is also the "riskiest" because it is the only option where a business failure could result in losing your primary residence.

Expert Verdict: When Should You Pull the Trigger?

Deciding to use your home to fund a business is a major milestone. As a mortgage professional, I believe this strategy works best when it is treated as a calculated investment rather than a desperate gamble. Before you move forward, run through this final checklist:

Proven Business Model: Do you already have customers or a clear, tested plan? Using equity is ideal for scaling a business that already shows promise, rather than just testing an unproven idea.

Low Debt-to-Income (DTI) Ratio: Can you comfortably afford the new monthly payment even if the business has a slow month? A safety cushion in your monthly budget is essential.

Strong Housing Market: Is your local real estate market stable? Having extra equity "left over" in your home provides a safety net if property values dip.

From a mortgage advisor’s perspective, leveraging your home is one of the most cost-effective ways to access large amounts of capital. It allows you to maintain full control of your company without the pressure of outside partners. However, the goal is always to use the house as a launcher, not a crutch. If you have a solid credit score and a clear path to revenue, your home equity can be the ultimate tool to bridge the gap between where your business is and where it needs to go.

Taking the Next Step Toward Your Business Goals

Using your home equity is one of the smartest ways to secure low-cost capital while keeping 100% ownership of your new venture. By choosing the right tool—whether it’s the flexibility of a HELOC, the stability of a home equity loan, or the long-term structure of a cash-out refinance you can give your business the financial foundation it needs to thrive. Your home is more than just a place to live; it is a powerful asset that can fund your future.

Ready to see how much capital you can access? Schedule a Strategy Call with a Mortgage Consultant to Review Your Equity today and get a personalized plan for your startup journey.