As we navigate the 2026 housing market, many homeowners are searching for ways to stabilize their monthly expenses. While interest rates have seen significant shifts over the past few years, the opportunity to reduce your monthly mortgage payment remains a top priority for families across the United States. As a dedicated Mortgage Consultant specializing in home equity and refinancing, I have helped countless homeowners transition from high-interest debt into more manageable, government-backed solutions.

One of the most effective, yet often misunderstood, tools available today is the Streamline Refinance. Unlike traditional refinancing, which can involve mountains of paperwork and expensive appraisals, these government-backed programs (FHA, VA, and USDA) are designed for speed and simplicity. The core "Search Intent" for most homeowners is simple: How can I lower my rate without the headache? A streamline refinance does exactly that: it focuses on providing a tangible financial benefit, such as a lower interest rate or a more stable loan term, with significantly less documentation than a standard loan.

What Is a Streamline Refinance? A Simple Explanation for South Asian Homeowners in the USA

A streamline refinance is a faster, simpler way to get a lower interest rate on your existing government-backed home loan with less paperwork, no income proof in most cases, and often no new home appraisal required.

The Basic Meaning of a Streamline Refinance

If you already have a government-backed mortgage such as an FHA, VA, or USDA loan, a streamline refinance lets you replace it with a better loan without going through the full, lengthy process you experienced when you first bought your home.

Think of it like renewing your phone plan. You are already a trusted customer. The provider does not need to re-verify everything from scratch. Similarly, because you have already proven you can manage your mortgage, the government allows a quicker, less complicated path to refinancing.

The word "streamline" simply refers to the simplified paperwork and approval process not to skipping any real responsibilities.

The Net Tangible Benefit Rule and How It Protects You

Before you qualify for a streamline refinance, your new loan must pass what is called the Net Tangible Benefit test. In plain terms: the new loan must genuinely improve your financial situation.

This usually means one of two things:

Your monthly payment must drop by a specific amount or percentage, OR

You are switching from an adjustable-rate mortgage (ARM) where your payment can go up unpredictably to a fixed-rate mortgage, where your payment stays the same every month.

For many South Asian families in the USA who are balancing multiple financial goals at once, sending remittances back home, saving for children's education, or building a retirement fund, a lower, predictable monthly payment can make a real difference in day-to-day cash flow.

This rule exists to protect you. It ensures that refinancing is truly worth it for you, not just a process that costs you fees without any real benefit.

What a Streamline Refinance Does Not Include

It is easy to assume that "streamline" means you can skip payments or pause your loan obligations for a while. That is not the case.

What it does mean is less documentation. Specifically:

No income verification in most cases you typically do not need to submit recent pay stubs or W-2 forms

No new home appraisal required in most programs this is especially helpful if your home's value has not increased much, or if you live in an area where property prices fluctuate

This is a significant advantage for homeowners who may have bought in a market where values have been uneven. You are not penalized for factors outside your control.

You will still pay for items like mortgage insurance and basic closing costs but the overall goal is straightforward: reduce your interest rate, lower your monthly payment, and make your home more affordable over the long term.

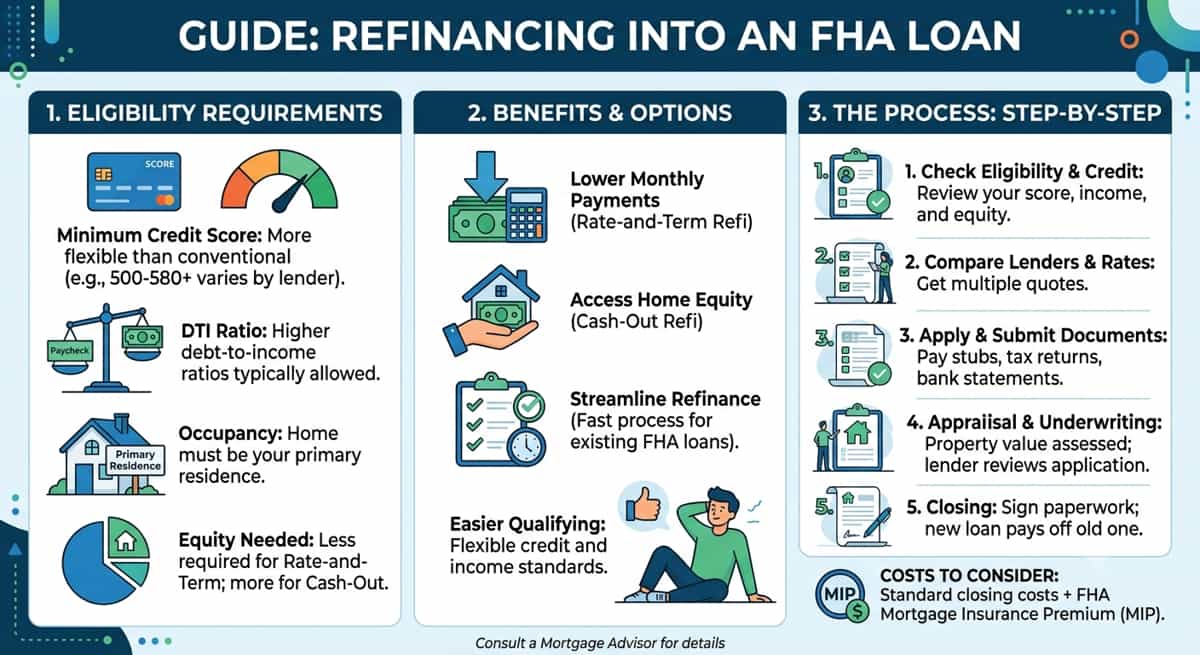

FHA Streamline Refinance - A Simpler Way to Lower Your FHA Loan Payment

If you already have an FHA loan, the FHA Streamline Refinance lets you lower your monthly payment with less paperwork, no income verification in most cases, and no new home appraisal as long as your loan is in good standing and at least 210 days old.

How the FHA Streamline Refinance Works

The FHA Streamline Refinance is designed specifically for homeowners who already have an FHA-insured mortgage. Since the Federal Housing Administration already backs your current loan, they are willing to simplify the process significantly waiving many of the standard requirements to help you reach a more affordable monthly payment faster.

For South Asian homeowners in the USA who took out an FHA loan when buying their first home, this can be a practical way to take advantage of lower interest rates without starting the entire loan process over again.

Eligibility Basics for FHA Borrowers

To qualify, your existing mortgage must be FHA-insured and in good standing. Here is what that means in practice:

No more than one 30-day late payment in the past 12 months

No late payments at all in the last 6 months

Your payment history is the most important factor here. If you have been consistently paying on time even through financially tight months you are likely in a strong position to qualify.

Mortgage Insurance Costs to Expect

The FHA Streamline Refinance does come with mortgage insurance costs, which are worth understanding before you move forward:

Upfront Mortgage Insurance Premium (UFMIP): Typically 1.75% of the new loan amount. The good news is that this can usually be rolled into your new loan, so you do not need to pay it out of pocket at closing.

Annual Mortgage Insurance Premium (MIP): Paid in 12 monthly installments. For most homeowners in 2026, this annual rate is approximately 0.55% noticeably lower than what older FHA loans carried.

Two Paths - Non-Credit Qualifying vs. Credit Qualifying

One practical feature of this program is that it offers two different approval paths depending on your situation:

Non-Credit Qualifying This is the true "streamlined" experience. The lender generally does not verify your income, check your debt-to-income ratio, or pull a full credit report. This path works well for homeowners whose financial picture may have shifted perhaps a job change or a gap in employment but who have kept up with their mortgage payments throughout.

Credit Qualifying This path involves a more traditional review of your credit and income. It is typically required if you are removing a co-borrower from the original loan, or if the new monthly payment will increase by more than 20% for example, if you are shortening your loan term from 30 years to 15 years.

The 210-Day Waiting Period Before You Can Refinance

You cannot refinance right after closing on your home. The FHA requires a seasoning period of a minimum amount of time to confirm the loan is stable before a new one is issued. You must meet both of the following conditions:

You must have made at least six monthly payments on your current FHA loan

At least 210 days must have passed from the closing date of the loan you are refinancing

This waiting period is there for your benefit as well. It encourages refinancing as a thoughtful, long-term decision rather than a quick reaction to short-term market changes.

The 5% Rule - A Simple Way to Check If You Qualify

To meet the Net Tangible Benefit requirement for an FHA Streamline Refinance, your new total monthly payment covering principal, interest, and mortgage insurance must be at least 5% lower than your current total payment.

Here is a quick way to check:

Multiply your current total monthly payment by 0.95. If your new estimated payment is at or below that number, you very likely meet the requirement.

For example, if your current total monthly payment is $1,800, your new payment would need to be $1,710 or less. A straightforward calculation that can save you thousands over the life of your loan.

VA IRRRL - The VA's Streamlined Refinance Option for Veterans and Service Members

The VA Interest Rate Reduction Refinance Loan (IRRRL) lets eligible veterans, active-duty service members, and surviving spouses lower their interest rate on an existing VA loan with no new appraisal, no Certificate of Eligibility needed, and flexible occupancy rules.

What the VA IRRRL Offers and Who It Is For

The IRRRL often pronounced "Earl" is the Department of Veterans Affairs' version of a streamline refinance. It is built exclusively for people who already have a VA-backed mortgage and want to move into a lower interest rate with minimal paperwork and fewer hoops to jump through.

Because the VA already guarantees your current loan, they do not require you to reapply for a Certificate of Eligibility (COE) or get a new home appraisal. This is especially valuable if your home's market value has dropped since you bought it, something that has affected many homeowners in fluctuating real estate markets across the USA.

For South Asian veterans and military families who have served and settled in the United States, this program is one of the most straightforward ways to reduce housing costs without starting the loan process from scratch.

Switching from an Adjustable-Rate to a Fixed-Rate VA Loan

Many homeowners initially chose an Adjustable-Rate Mortgage (ARM) because it offered lower payments at the start. But as interest rates shift, that unpredictability can turn into real financial stress especially when you are managing a household budget, planning for your children's future, or supporting family members.

The IRRRL allows you to switch from a VA ARM to a fixed-rate mortgage with very little friction. Even if the new fixed rate is slightly higher than your current adjustable rate, the VA typically approves this move because locking in a stable, consistent payment is considered a genuine financial benefit in itself. You gain long-term certainty knowing your housing cost will not spike unexpectedly year after year.

Closing Costs, the VA Funding Fee, and No-Cost Options

The IRRRL is designed to be affordable, but there are still some costs to be aware of:

VA Funding Fee: Currently set at 0.5% of the loan amount for an IRRRL. This fee goes directly to the VA to sustain the program for future veterans.

No-Cost Option: Many lenders offer to cover your closing costs in exchange for a slightly higher interest rate. This can be a smart trade-off if you want to avoid upfront expenses.

Roll-In Option: The VA also allows you to bundle all closing costs and the funding fee into your new loan amount. This means you can lower your monthly payment without paying thousands of dollars out of pocket at the closing table.

For families without large cash reserves, a common situation for many first-generation homeowners, this flexibility makes the IRRRL genuinely accessible rather than just theoretically beneficial.

Occupancy Rules - Previous Residence Is Enough to Qualify

Standard VA purchase loans require you to certify that the home is your current primary residence. The IRRRL is more flexible on this point.

To qualify, you only need to certify that you previously lived in the home, not that you live there now. This is a meaningful distinction for:

Service members who have been reassigned to a different base or location

Families who have since moved and converted their first home into a rental property

As long as there is an existing VA loan on the property, you can still use the IRRRL to lower your rate and improve monthly cash flow regardless of where you currently live. For military families spread across different states or even overseas, this rule removes a barrier that would otherwise make refinancing impossible.

USDA Streamline Refinance - A Lower Monthly Payment for Rural and Suburban Homeowners

If you already have a USDA home loan and live in an eligible rural or suburban area, the USDA Streamline Refinance lets you lower your monthly payment with little to no paperwork, no new appraisal and no credit check required in most cases.

How the USDA Streamline Refinance Works

The USDA Streamline Refinance is available to homeowners who already have a USDA Direct or Guaranteed loan. It is offered through the U.S. Department of Agriculture and is designed to make your existing rural home loan more affordable without putting you through the full refinancing process again.

One important rule to know upfront: this must stay a USDA-to-USDA refinance. You cannot use this program to switch to a conventional or FHA loan. This keeps you within the protections and benefits that come with rural development loans while helping you reach a lower monthly payment.

For South Asian families who settled in rural or suburban communities drawn by more affordable housing, quieter neighborhoods, or proximity to agricultural work, this program is a practical way to reduce housing costs without disrupting the loan structure that made homeownership possible in the first place.

Streamlined Assist vs. Standard Streamlined - Two Paths to Choose From

The USDA offers two versions of the streamline refinance, and understanding the difference helps you choose the right fit:

Streamlined Assist This is the more popular and simpler of the two. To qualify, your new monthly payment including principal, interest, and fees must be at least $50 lower than what you currently pay. In most cases, no new home appraisal is needed and no credit report is required. If your priority is speed and simplicity, this is the faster path to monthly savings.

Standard Streamlined This version also skips the home appraisal in most cases, but it does include a basic credit review. It is a good fit for homeowners who cannot meet the strict $50 monthly savings requirement of the Assist program but still want to lower their interest rate or adjust their loan term without going through a full traditional refinance.

Income Limits and the DTI Waiver Advantage

Because USDA loans are designed for low-to-moderate-income households, you must still meet the program's income eligibility guidelines. In 2026, these limits are based on your county and household size generally capped at 115% of the area's median income.

However, the Streamlined Assist program offers one standout advantage that sets it apart from nearly every other mortgage product: no debt-to-income (DTI) calculation.

In a standard refinance, lenders look at how much debt you carry compared to your income. If that ratio has gone up perhaps due to a car loan, medical bills, or supporting extended family members it can disqualify you. The Streamlined Assist skips this calculation entirely. As long as you have made your mortgage payments on time for the last 12 months, you can still qualify for a lower rate, regardless of how your overall debt picture has changed.

This is a meaningful relief for many South Asian households where financial responsibilities often extend beyond just the immediate family.

Property Eligibility - Even If Your Area Has Grown Over Time

A common concern among USDA homeowners is whether their property still qualifies if their neighborhood has expanded and no longer looks "rural" on a map. This is a valid worry as many suburban communities around major cities have changed significantly over the past decade.

The USDA addresses this with a built-in protection: as long as your original loan was a USDA loan, your property remains eligible for the Streamline Refinance even if the area is no longer officially designated as rural on the latest census maps.

This means you are not penalized for local development or population growth happening around you. Your path to better loan terms stays open as long as the home remains your primary residence.

Comparing the Options: Which Streamline is Right for You?

Choosing the right streamline program depends entirely on which government entity currently backs your mortgage. Because these are "like-for-like" programs, you cannot jump from an FHA loan to a VA IRRRL. However, understanding how they compare helps you see the unique advantages of your specific loan type.

The most critical factor to consider is the break-even point. This is the moment when the monthly savings from your lower interest rate finally "pay back" the closing costs you spent to get the loan. As a mortgage consultant, I recommend looking for a break-even point of 24 months or less to ensure the move makes long-term financial sense.

Refinance Comparison At-a-Glance

Feature | FHA Streamline | VA IRRRL | USDA Streamlined Assist |

Appraisal Required? | Usually No | No | No |

Credit Check? | Optional (Lender Dependent) | No | No |

Income Verification? | No | No | No |

Upfront Fee | 1.75% (UFMIP) | 0.50% (Funding Fee) | 1.00% (Guarantee Fee) |

Monthly Insurance | Yes (MIP) | No | Yes (Annual Fee) |

Max Loan-to-Value | Unlimited | Unlimited | Unlimited |

Professional Analysis: Finding Your Best Path

For Veterans (VA IRRRL): This is arguably the strongest refinance tool in the US. With no monthly mortgage insurance and the lowest upfront fee (0.50%), veterans often see the fastest break-even point sometimes in as little as 6 to 10 months.

For FHA Borrowers: Your biggest advantage is the MIP Refund. If you refinance your current FHA loan into a new FHA Streamline within three years, you may receive a partial refund of your original upfront mortgage insurance, which can be applied to your new loan's costs.

For USDA Borrowers: The "Streamlined Assist" is unique because it allows for a refinance even if your Debt-to-Income (DTI) ratio has risen significantly, as long as you have a clean payment history.

Regardless of the program, these options share one powerful trait: they ignore your Loan-to-Value (LTV) ratio. Even if your home equity has decreased due to market shifts, you can still qualify for a lower rate because no new appraisal is required to prove the home's value.

Navigating Home Equity: Can You Cash Out During a Streamline?

A common question many homeowners ask is whether they can tap into their home equity while performing a streamline refinance. Because the process is so fast and efficient, it is natural to want to use that speed to access cash for home improvements or debt consolidation. However, it is vital to understand the "Streamline" rules to avoid a surprise at the closing table.

By definition, a streamline refinance does not allow for a "cash-out" option. These programs are strictly designed to lower your interest rate or change your loan term. In fact, most government-backed streamline programs limit the amount of cash you can receive back at closing to no more than $500. If your goal is to walk away with a check to pay off credit cards or renovate your kitchen, a streamline refinance will not meet that specific need.

The Difference: Streamline vs. Cash-Out Refi

If you need to access your equity, you would instead look at a Traditional Cash-Out Refinance. Here is how the two paths differ:

Appraisal Requirements: A streamline refinance typically ignores your home's current value. A cash-out refinance always requires a fresh appraisal to determine exactly how much equity you have available.

Income Verification: While streamlines often waive income checks, a cash-out loan requires a full review of your debt-to-income (DTI) ratio to ensure you can handle the larger loan balance.

Cost and Time: Because a cash-out refi involves more risk for the lender, the interest rates are often slightly higher, and the paperwork is more extensive.

As your advisor, my goal is to help you choose the path that matches your 2026 financial goals. If your priority is a lower monthly payment with zero hassle, the streamline is your best bet. If you need capital to invest back into your home, we should discuss a traditional refinance instead.

The Step-by-Step Refinancing Process with a Mortgage Advisor

Navigating a refinance, even a "streamlined" one is a significant financial decision. While the paperwork is lighter than a standard loan, the impact on your long-term savings is substantial. Working with a licensed Mortgage Consultant ensures you aren't just getting a new loan, but a strategic financial upgrade. A professional advisor helps you cut through the noise of "bait-and-switch" offers that often hide high fees behind seemingly low interest rates.

Here is what you can expect when we work together:

Step 1: Initial Consultation & Net Tangible Benefit Test

Our first conversation isn't about filling out forms; it's about checking the math. We perform a "Net Tangible Benefit" test to ensure the refinance actually saves you money. We will look at your current interest rate, your remaining loan term, and any mortgage insurance you are paying. If the math doesn't result in a clear, long-term gain for you, a reputable advisor will tell you to stay with your current loan.

Step 2: Documentation Gathering

"Streamlined" doesn't mean "document-free." While we usually won't need your tax returns or a home appraisal, we still need to verify the basics. You will typically provide:

A copy of your most recent mortgage statement.

Your current homeowners insurance declaration page.

Basic identification (such as a Driver’s License).

Your most recent pay stub (in some cases, just to verify active employment).

By organizing these early, we can often move from application to approval in a fraction of the time a traditional loan requires.

Step 3: The Closing Process

Once your loan is approved, we move to the closing. This is where you sign the final documents. Unlike a home purchase, you don't necessarily have to meet at a title office; many streamline refinances can be closed in your own home with a mobile notary.

Because these are government-backed loans, you also benefit from a "right of rescission" on primary residences, which gives you a three-day window after signing to cancel the loan if you change your mind. My role as your consultant is to ensure every line item on that final disclosure matches exactly what we discussed during our initial consultation.

Conclusion: Securing Your Financial Future

Taking advantage of a streamline refinance is more than just a way to lower a monthly bill; it is a strategic move to strengthen your overall financial health. Whether you are a veteran looking to capitalize on your VA benefits, a rural homeowner utilizing USDA options, or a family lowering FHA costs, these programs offer a rare path to savings with minimal stress. By reducing your interest rate and stabilizing your monthly housing costs, you free up resources for other life goals be it retirement savings, education, or simply more breathing room in your monthly budget.

The mortgage landscape in 2026 offers unique opportunities, but they require a careful, expert eye to navigate successfully. Don't leave your financial future to chance or automated "one-size-fits-all" calculators. Reach out today for a personalized consultation. We will run the numbers together to ensure a streamline refinance is the right move for your home and your family.