For decades, the path to a home loan in the United States followed a predictable, albeit frustrating, ritual. It involved sitting in a mahogany-paneled bank lobby, clutching a folder of paper tax returns, and waiting for a loan officer to tell you which of their three "in-house" products you qualified for. In this "Old Way," the lender held all the cards, and the borrower was often shoehorned into a mortgage that benefitted the bank’s quarterly margins more than the homeowner’s long-term wealth.

As a Senior Mortgage Consultant specializing in home equity and refinancing strategies, I have seen the friction of this legacy system firsthand. The fundamental problem with traditional retail lenders is their inherent limitation: they are restricted to their own balance sheets. If their specific "Refinance Product A" doesn't suit your unique financial profile perhaps you're self-employed or looking to leverage equity for high-yield investments they rarely have a "Product B" to offer. This lack of agility often leaves homeowners with higher interest rates and missed opportunities to optimize their largest asset.

The "Smart Way" has arrived to disrupt this stagnation. Today, smarter home loans technology has transformed the mortgage landscape from a transactional hurdle into a tool for genuine financial empowerment. We aren't just talking about a digital application or an online portal; we are talking about sophisticated data-driven ecosystems that analyze thousands of loan programs in real-time.

This evolution allows us to move beyond the "one-size-fits-all" mentality. By integrating hyper-personalized shopping algorithms with professional advisory, we can now pinpoint the exact moment your home equity becomes a powerful engine for wealth, ensuring your mortgage works for you not the other way around.

Why Your Current Lender is Stuck in the Past

If you currently have a mortgage with a major retail bank, you might assume they are the natural first choice for your refinance or home equity needs. However, the internal mechanics of large-scale banking often create a significant disadvantage for the consumer. This disconnect stems from institutional bias. A traditional bank is incentivized to sell you its own proprietary products, regardless of whether a better rate or more flexible equity term exists just across the street. Because they operate within a closed ecosystem, their "advice" is frequently limited to a narrow menu of options that prioritize the bank’s profit margins over your specific financial goals.

Furthermore, many traditional lenders are caught in the "One-Size-Fits-All" trap. These institutions rely on rigid, legacy algorithms designed for the "perfect" borrower profile. If your financial life has any nuance such as being a self-employed entrepreneur with complex tax returns, or a homeowner looking to leverage equity in a rapidly appreciating but non-traditional neighborhood these systems often fail. They lack the granularity to assess property values and credit stories with modern precision. In these scenarios, a "no" from a big bank often isn't a reflection of your creditworthiness, but rather a limitation of their outdated software.

Finally, there is the undeniable issue of agility. In a market where interest rates can shift overnight and home equity windows can open and close rapidly, speed is a financial asset. Traditional lenders are often bogged down by multi-layered bureaucracy and manual processing queues that can stretch for weeks or even months.

In contrast, modern fintech-driven advisory models utilize automated data verification and real-time market syncing to move at the speed of the current economy. While a legacy lender is still waiting for a manual review of your paystubs, a smarter, technology-enabled consultant has already scanned dozens of secondary markets to find the most aggressive equity products available. By the time the big bank sends an initial follow-up email, a "smart" borrower is often already halfway to the closing table, securing their financial future with precision and speed.

What is "Smarter Home Loans Technology"?

When we discuss "smarter home loans technology," we are referring to a sophisticated digital infrastructure that replaces guesswork with mathematical certainty. At its core, this technology utilizes Real-Time Data Integration to provide an immediate, transparent snapshot of your financial standing. Gone are the days of waiting two weeks for a physical appraisal just to see if a refinance is viable. Today, we utilize Automated Valuation Models (AVM) that sync with local tax records and recent neighborhood sales data to estimate your current Loan-to-Value (LTV) ratio instantly. This transparency allows homeowners to see exactly how much equity they can access before they even begin a formal application.

Beyond simple data retrieval, the "brains" of modern lending lies in AI-Powered Underwriting. By leveraging natural language processing and machine learning, these systems can analyze complex financial documents like multi-page business tax returns or diverse investment portfolios with a level of speed and accuracy that human processors simply cannot match. This technology identifies potential hurdles in your Debt-to-Income (DTI) ratio early in the process, allowing for proactive adjustments. By reducing human error and automating the verification of employment and assets, the "time to close" is slashed from the industry-standard 45 days to as little as two weeks.

Perhaps the most revolutionary aspect of this technology is Predictive Analytics. Smarter platforms don't just look at where you are today; they monitor mortgage-backed securities (MBS) trends and broader economic indicators to forecast market shifts. For a homeowner, this means your mortgage advisor can provide "active monitoring" of your loan.

Instead of you having to track the news, the technology alerts us when a dip in interest rates intersects perfectly with your equity growth, signaling the "optimal strike zone" for a refinance. This shift from reactive to proactive borrowing ensures that you are never stuck in a high-interest loan when the market offers a better alternative. By blending these high-tech tools with professional oversight, we ensure that your mortgage is a dynamic component of your wealth strategy rather than a static debt.

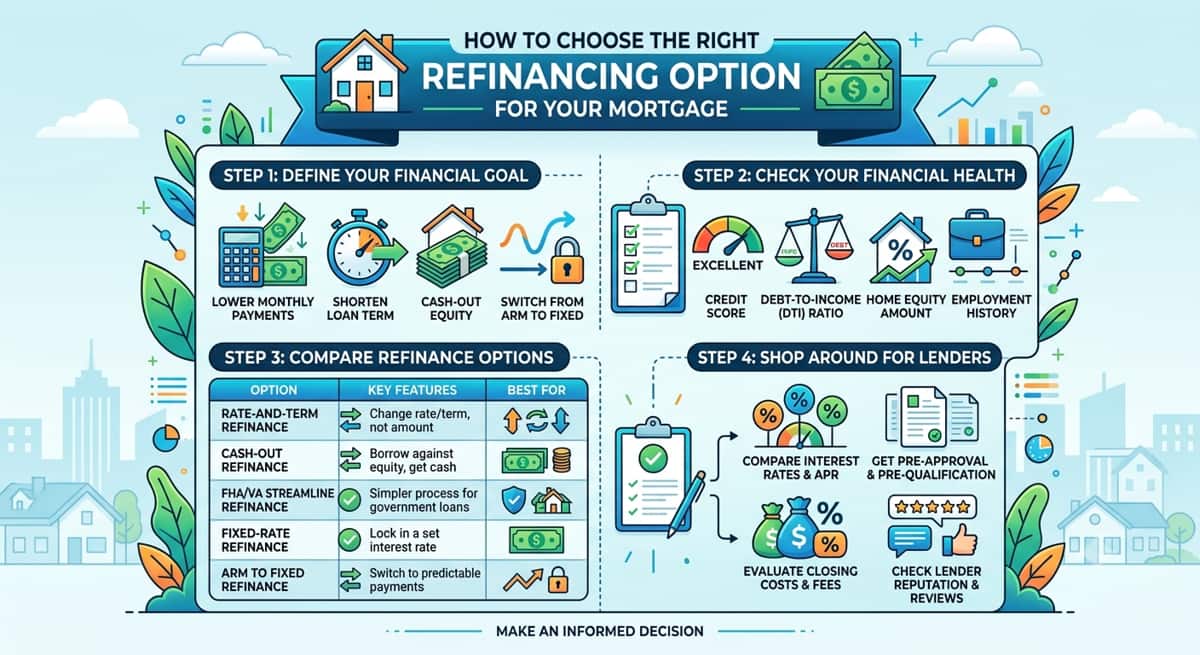

The Power of Personalized Mortgage Shopping for Refinancing

In the traditional lending world, the conversation almost always begins and ends with a single number: the interest rate. However, a smarter approach to refinancing looks far beyond that superficial figure. True personalized mortgage shopping focuses on the total cost of homeownership. This includes analyzing the long-term interest paid over the life of the loan, the impact of mortgage insurance, and how the new debt structure aligns with your retirement or investment goals. By shifting the focus from "what is the rate?" to "what is the net gain?", homeowners can make decisions based on actual wealth accumulation rather than marketing slogans.

One of the most potent tools in a modern advisor’s arsenal is the ability to model Cash-Out Refinance Strategies with surgical precision. Using smarter technology, we can calculate the exact Return on Investment (ROI) for accessing your equity. For example, if you are carrying high-interest credit card debt at 22%, using your home equity to consolidate that debt into a mortgage at a fraction of that rate can save you thousands in monthly cash flow. Similarly, the technology can help determine if refinancing to fund a kitchen remodel will increase your home's value enough to offset the cost of the loan. We use data to move from "I think this is a good idea" to "The numbers prove this is a good idea."

This level of precision is made possible by the Comparison Engine. Unlike a retail bank that is limited to its own internal rate sheet, a modern mortgage advisor utilizes a platform that acts as a "broker advantage" hub. This technology allows us to shop your specific scenario across 50+ different wholesale lenders simultaneously. This competition forces lenders to bid for your business, ensuring you receive the most aggressive pricing and flexible terms available in the entire U.S. market.

However, a smart financial move must always be tempered with transparency. Refinancing is a powerful tool, but it is not without costs. It is vital to consider the "break-even point" the moment where the monthly savings from your new rate finally cover the closing costs associated with the loan. Additionally, one must be cautious about "resetting the clock." If you have 20 years left on a 30-year mortgage and you refinance into a new 30-year term, you may lower your monthly payment but significantly increase the total interest paid over time. A personalized shopping experience ensures that these variables are clearly mapped out, so you aren't just getting a "deal," but a sustainable financial improvement.

Unlocking Home Equity: Smarter Ways to Use Your Wealth

In the modern financial landscape, your home is more than a shelter; it is a sophisticated wealth-building vehicle. However, many homeowners leave their equity "trapped" in the walls of their house because they aren't sure which tool is best for extraction. When we look at smarter ways to use your wealth, two primary products dominate the conversation: the Home Equity Loan and the Home Equity Line of Credit (HELOC).

HELOC vs. Home Equity Loan: A Strategic Breakdown

Choosing between these products depends entirely on your financial objective. A Home Equity Loan is an installment loan that provides a one-time lump sum at a fixed interest rate. This is the "smart" choice for predictable, one-time expenses like debt consolidation or a specific home renovation project where the costs are known upfront. Because the rate is locked, you are protected from future market volatility.

Conversely, a HELOC functions more like a credit card secured by your home. It provides a revolving line of credit that you can draw from, repay, and draw from again during a set "draw period" (typically 10 years). This is the ideal tool for ongoing or unpredictable costs, such as "pay-as-you-go" home improvements or a business startup fund. While HELOCs usually feature variable interest rates, they offer unparalleled flexibility, as you only pay interest on the specific amount you have borrowed at any given time.

Real-Time Equity Tracking

Smarter technology now allows us to move beyond the once-a-decade appraisal. Modern advisors use integrated platforms that provide real-time equity tracking. By syncing your current mortgage balance with live market data and local appreciation trends, we can monitor your Combined Loan-to-Value (CLTV) ratio every month. This data-driven approach allows you to treat your equity like a liquid investment account, enabling you to pivot your financial strategy the moment your property hits a specific value milestone.

The Impact of Tax Implications

While the primary goal of leveraging equity is often wealth building, the "smart" borrower also considers the tax advantages. Under current IRS guidelines, interest paid on home equity debt may be deductible if the funds are used specifically to "buy, build, or substantially improve" the home that secures the loan.

For instance, using a HELOC to add a bedroom could provide a tax benefit, whereas using it to pay off credit card debt while still a sound move for cash flow typically would not. Because tax laws are subject to change and vary based on individual income, it is essential to consult with a qualified CPA to understand how these deductions apply to your specific tax bracket. By combining this professional tax advice with smarter loan technology, you ensure that every dollar of equity is optimized for your long-term net worth.

Human Expertise + AI: Why the Advisor Still Matters

While "Smarter Home Loans Technology" provides the engine for modern lending, the human advisor remains the navigator. We have entered an era of "Push Button" mortgages, but a common pitfall for many borrowers is believing that an algorithm can handle the nuances of a complex financial life. This is known as the "Algorithm Gap." Standard automated systems are designed for linear, "cookie-cutter" scenarios. If you are a self-employed professional with fluctuating seasonal income, or if you are looking to refinance a unique property with limited comparable sales, a rigid algorithm will often default to a denial. A human expert, however, knows how to package and present your "financial story" to the right lender, translating complex data into a format that technology can then process successfully.

Beyond just getting a loan approved, a professional mortgage consultant uses technology for Strategic Planning. A digital app can tell you what your monthly payment will be today, but it cannot build a 5-to-10-year financial roadmap. As your advisor, I use these advanced tools to stress-test your mortgage against various future scenarios. Will you be better off with a 15-year fixed rate if you plan to retire in a decade? Or does a 30-year term with an aggressive side-investment strategy yield a higher net worth? We use data to answer these questions, ensuring that your home loan is a tactical component of your broader wealth strategy.

Finally, there is the indispensable element of Trust and Industry Experience. The mortgage market is governed by "overlays" internal rules that lenders add on top of standard federal guidelines. One lender might be incredibly strict regarding credit inquiries, while another might be very lenient for borrowers with significant cash reserves.

Having spent years in the trenches of the U.S. mortgage market, I know which lenders have "soft" overlays and which are better suited for specific borrower profiles. This insider knowledge saves you time, prevents unnecessary credit hits, and ensures that you aren't just getting any loan, but the right loan. Technology provides speed, but human experience provides safety and strategy.

How to Spot a Truly "Smart" Mortgage Experience

In a marketplace crowded with flashy advertising, it can be difficult to distinguish between a lender that is truly "smart" and one that simply has a modern website. A genuine smarter home loan experience is defined by three pillars: transparency, speed, and customization.

First, evaluate the level of transparency. A technology-forward lender doesn't keep you in the dark. They provide a dedicated digital dashboard where you can see exactly where your loan sits in the pipeline—from "Initial Disclosure" to "Clear to Close." You should have real-time access to the same data your advisor sees, including live interest rate fluctuations and current equity valuations. If you have to call and leave a voicemail just to get a status update, you are working with a legacy system.

Next, consider Speed. In today’s competitive real-time economy, a manual pre-approval process is a liability. A smart lender uses automated asset and income verification (day-one certainty), allowing for a pre-approval that is backed by verified data in minutes rather than days. This speed is critical when you are trying to lock in a rate during a sudden market dip.

Finally, look for Customization. Is the lender acting as an "order taker," simply asking what loan you want? Or are they engaged in Mortgage Planning? A smart experience involves analyzing your debt structure, tax position, and long-term goals to recommend a specific financial path.

The "Obsolete Lender" Checklist

To determine if your current bank is falling behind, ask them these five questions:

Do you offer automated income and asset verification, or will I need to manually upload months of PDFs and bank statements?

Can you shop my loan across multiple wholesale investors, or am I limited only to your bank’s internal rates?

Do you provide a real-time digital dashboard that tracks my loan's progress 24/7?

Do you use Automated Valuation Models (AVMs) to provide an instant estimate of my home equity before I pay for an appraisal?

Can you show me a 5-year total cost analysis comparing different loan structures side-by-side?

If the answer to more than two of these is "No," your lender's technology and your financial potential is likely stuck in the past.

Conclusion: Your Home is Your Largest Asset - Treat it That Way

For the average American, a home is not just a place to live; it is the cornerstone of their financial portfolio. Entrusting such a significant asset to an outdated, "one-size-fits-all" banking system is no longer a necessity, it's a risk. As we have explored, smarter home loans technology has dismantled the traditional barriers to entry, providing the transparency and speed that modern borrowers deserve. However, it is vital to remember that while technology is the tool that facilitates the process, a personalized strategy remains the driver of true wealth.

The future of the mortgage landscape is shifting decidedly toward the consumer. We are moving into an era where data-driven insights will allow for hyper-dynamic lending, where your mortgage adjusts as your life and the markets evolve. The days of "set it and forget it" debt are over.

The most important takeaway is this: waiting for your current bank to call you with a better deal is a losing strategy. Large institutions thrive on borrower inertia. By the time a traditional lender reaches out to offer a refinance, the market’s best opportunities have often already passed. Taking a proactive, tech-enabled approach to your mortgage ensures that you are always positioned to capture equity and maximize your net worth. Treat your home like the powerhouse asset it is, and use the smartest tools available to manage it.