Bankruptcy is often viewed as a final chapter, but in the world of real estate, it is frequently a turning point. As a Mortgage Consultant, I have seen firsthand the emotional and financial weight that a filing carries. However, your home remains one of your most powerful tools for financial rehabilitation.

Refinancing after bankruptcy isn't just about swapping one debt for another; it is a strategic move for credit restoration and long-term wealth building. By leveraging your home’s equity, you can access lower mortgage interest rates that reflect your improving financial health rather than your past setbacks. Whether you are looking to lower your monthly payments or consolidate remaining debts, a well-timed refinance serves as a bridge to a stable future. While the road to recovery requires patience and a clear plan, the opportunity to reset your finances and secure your family’s home is closer than you might think.

Understanding the "Waiting Period": Timelines by Loan Type

The most common question I hear is: "How long do I have to wait?" In the mortgage industry, this is known as the seasoning period. This is the mandatory time that must pass between your bankruptcy discharge date (when your debts are legally erased) or dismissal date (if the case was closed without discharge) and the day you are eligible for a new loan. These seasoning requirements vary significantly depending on which type of bankruptcy you filed and which loan program you choose.

Chapter 7 Bankruptcy: The 2-4 Year Rule

Chapter 7 is often called a "liquidation" bankruptcy. Because it wipes out debt quickly, lenders typically require a longer waiting period to ensure you’ve stabilized your finances. For a Conventional loan (Fannie Mae or Freddie Mac), the standard wait is four years from the discharge or dismissal date. However, if you are looking at government-backed options like FHA or VA loans, that timeline is cut in half to just two years. In rare cases involving "extenuating circumstances" like a medical emergency or a sudden job loss some lenders may reduce the FHA wait to just 12 months, though this requires extensive documentation.

Chapter 13 Bankruptcy: The 12-Month Rule

Chapter 13 is viewed more favorably by lenders because it involves a court-ordered repayment plan. Because you are actively paying back creditors, you can often refinance much sooner. In fact, for FHA, VA, and USDA loans, you may be eligible to refinance after just 12 months of on-time payments, even if you haven't finished the full 3-to-5-year plan. This is a unique opportunity to lower your rate while still in the "active" phase of bankruptcy, provided you have written permission from the court trustee.

Conventional vs. Government-Backed Loans

When choosing between loan types, the difference in flexibility is clear. Conventional loans follow strict guidelines and generally require a two-year wait after a Chapter 13 discharge and a four-year wait after Chapter 7.

On the other hand, government-backed programs (FHA, VA, and USDA) are designed to help borrowers recover. They offer the shortest timelines, often just one to two years post-discharge. While conventional loans might offer slightly better terms for those with high credit scores, government-backed loans are the primary path for most homeowners seeking a fresh start shortly after a bankruptcy filing.

Chapter 13 Specifics: Refinancing While Still in Court Repayment

One of the biggest misconceptions in mortgage lending is that you must wait until your bankruptcy is completely finished before you can touch your home equity. In reality, homeowners currently enrolled in a Chapter 13 reorganization plan have a unique opportunity to improve their financial situation through a refinance. Whether your goal is to lower your monthly mortgage payment or pull cash out to pay off your bankruptcy plan early, the process is possible provided you follow the correct legal steps.

Securing Permission from the Court Trustee

Because your finances are technically under the supervision of the bankruptcy court, you cannot take on new debt without official approval. The key figure in this process is your court trustee. To move forward with a refinance, your attorney must file what is known as a motion to borrow or a motion to refinance.

The court wants to see that the new loan is in your best interest. Usually, this means proving the refinance will either:

Lower your monthly living expenses, making it easier to complete your plan.

Provide enough funds to pay off your bankruptcy plan in one lump sum, leading to an earlier discharge.

The Steps to Approval

To get the green light, you generally need to show that you have made at least 12 consecutive months of on-time payments toward your bankruptcy plan. Once you find a lender willing to work with active Chapter 13 cases, they will provide a "pre-approval" or a commitment letter.

Your attorney then presents this letter to the court as part of the permission to incur a debt request. If the trustee and the judge agree that the terms are fair and the new payment is manageable, they will issue a court order. This order is the "golden ticket" that allows your mortgage lender to finalize the loan and head to the closing table.

While this adds an extra layer of paperwork, the results can be life-changing. Successfully refinancing during a Chapter 13 plan can accelerate your financial rehabilitation, helping you exit bankruptcy with more cash flow and a stronger credit profile.

Critical Requirements Beyond the Waiting Period

Meeting the mandatory waiting period is a significant milestone, but it is only the first step toward qualifying for a refinance. Lenders look beyond the bankruptcy filing to evaluate your current financial stability. To secure an approval, you must meet specific standards regarding your credit health, debt levels, and the value of your home.

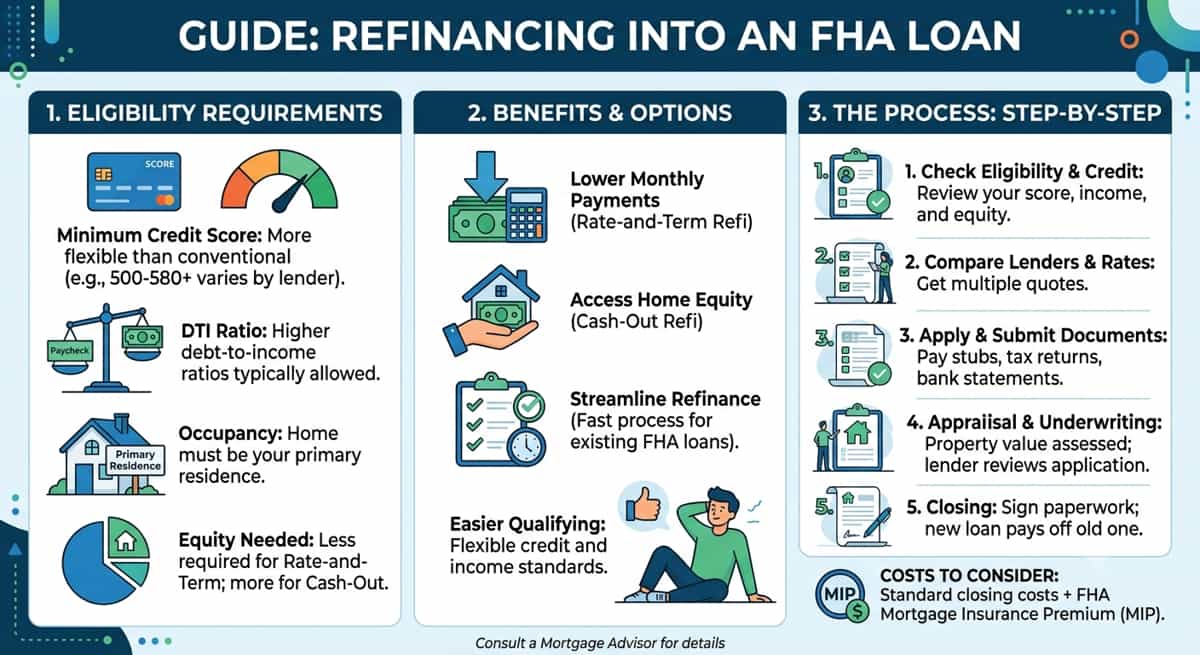

Credit Score Minimums: The FICO Foundation

Your credit score (FICO) is the primary tool lenders use to gauge risk. While bankruptcy causes a significant drop in your score, it begins to rebound the moment your debts are discharged. Most lenders have a "floor" or minimum score requirement for post-bankruptcy borrowers.

For government-backed loans like FHA or VA, you can often qualify with a score as low as 580 to 620. Conventional lenders (Fannie Mae and Freddie Mac) are typically stricter, often requiring a score of 620 to 660 or higher. It is important to note that while you might meet the minimum, a higher score will always secure a better interest rate, which is the ultimate goal of refinancing.

Re-established Credit: Proving Reliability

Lenders aren't just looking at a number; they are looking for a pattern of behavior. This is known as re-established credit. After your filing, you need to show that you can manage debt responsibly. Most programs require 12 to 24 months of "clean" payment history immediately preceding your application.

This means zero late payments on any new credit cards, auto loans, or your current mortgage since the bankruptcy was filed. Even a single 30-day late payment during this window can lead to an automatic denial, as it suggests that the financial instability that led to the bankruptcy hasn't been fully resolved.

The Equity Hurdle: Loan-to-Value (LTV) Standards

The final critical requirement is the amount of equity you hold in your home, measured by the Loan-to-Value (LTV) ratio. Equity is the difference between what your home is worth today and what you owe on your mortgage.

For a standard "rate-and-term" refinance (lowering your interest rate), you typically need at least 3% to 5% equity. However, if you are looking for a "cash-out" refinance to consolidate debt or pay off a Chapter 13 plan, lenders usually require you to leave at least 20% equity in the home. This means your new loan cannot exceed 80% of the home's appraised value. Because property values have risen significantly in many areas, many homeowners find they have crossed this "equity hurdle" sooner than they expected.

Meeting these three pillars score, history, and equity proves to the lender that you are a low-risk candidate ready for a second chance.

Home Equity Strategies: Cash-Out vs. Rate-and-Term

Once you have met the waiting period and credit requirements, you need to decide which refinancing strategy best fits your recovery goals. Your home equity the portion of the property you truly own is a versatile financial asset. Depending on your needs, you can use a refinance to either lower your monthly costs or access liquidity to clean up your balance sheet.

Using Cash-Out to Consolidate High-Interest Debt

A cash-out refinance allows you to take out a new mortgage for more than you currently owe and receive the difference in a lump sum. For someone recovering from bankruptcy, this is a powerful tool for debt consolidation.

After a bankruptcy filing, any new credit you obtain (like a subprime auto loan or a secured credit card) often comes with high interest rates. By using your home’s equity, you can pay off these expensive debts and replace them with a single mortgage payment at a much lower rate. This move simplifies your monthly obligations and significantly reduces the total interest you pay over time. It effectively uses your home as a low-interest engine to drive the rest of your financial recovery, providing the cash flow needed to build an emergency fund and avoid future debt cycles.

Refinancing to Remove Private Mortgage Insurance (PMI)

If your goal is purely interest rate reduction and lowering your monthly overhead, a "rate-and-term" refinance is the standard choice. One of the most effective ways this increase in monthly cash flow occurs is through the removal of Private Mortgage Insurance (PMI).

Many homeowners who bought with a low down payment are required to pay PMI, which can add hundreds of dollars to a monthly mortgage bill. If your home has increased in value since your bankruptcy filing, or if you have paid down the balance significantly, you may now own more than 20% of your home. By refinancing into a new loan without PMI, you instantly lower your housing costs without even necessarily needing a lower interest rate. This extra savings can then be redirected toward retirement accounts or personal savings, further strengthening your financial foundation.

Whether you choose to pull cash out or simply lower your payment, the goal is the same: making your home work for you as you build a stable, post-bankruptcy life.

Expert Strategies to Improve Your Approval Odds

Securing a mortgage after bankruptcy requires more than just meeting the basic criteria; it requires telling your story in a way that satisfies a lender's risk department. As an "insider" in the mortgage industry, I have found that the following three strategies are often the difference between a denial and an approval.

Writing a Winning Letter of Explanation

A Letter of Explanation (LOE) is your chance to speak directly to the person deciding on your loan the underwriter. This document should be concise, factual, and forward-looking. Rather than focusing on the past, use the LOE to explain what caused the bankruptcy and, more importantly, what has changed since then. For example, if your bankruptcy was caused by a specific event, state that clearly and then highlight your current stable income and new savings habits. Underwriters look for a "disregarded event," meaning a situation that is unlikely to happen again. A well-written LOE provides the context that a credit report cannot.

Extenuating Circumstances vs. Financial Mismanagement

Lenders distinguish between "financial mismanagement" and extenuating circumstances. If your bankruptcy was the result of things beyond your control such as a major medical emergency, the death of a primary wage earner, or a documented job loss due to a company-wide layoff you are viewed as a much lower risk.

Proving these circumstances with third-party documentation (like medical records or layoff notices) can often shorten your waiting period. Conversely, if the filing was due to overspending or poor credit management, you will likely need to wait the full seasoning period and show a more extensive history of perfect credit to prove you have learned from the experience.

The Value of a Manual Underwrite

Most modern mortgage applications are processed by an Automated Underwriting System (AUS), a computer program that gives a "Yes" or "No" based on data. However, bankruptcy files are complex and often get a "Refer" or "Rejected" status from the computer.

This is where manual underwriting becomes invaluable. In a manual underwrite, a human underwriter personally reviews every aspect of your file. They have the authority to look at the "big picture" your steady job, your significant home equity, and your clean payment history to override the computer's hesitation. If you have a unique situation, specifically ask your mortgage advisor if they offer manual underwriting for government-backed loans, as this is often the most reliable path to a "Clear to Close."

Common Pitfalls and Red Flags to Avoid

As you move closer to qualifying for a refinance, the final stretch is often where the most avoidable mistakes happen. Lenders are hypersensitive to any signs of financial instability during the post-bankruptcy period. Avoiding these common "red flags" will keep your application on track and protect your growing credit score.

Steer Clear of Predatory Lending

When you are in the "waiting period," you may receive "pre-approved" offers from companies specializing in subprime loans or "hard money" lending. These lenders often market specifically to people with recent bankruptcies, offering "no credit check" loans with extremely high interest rates and hidden fees.

While these offers may seem like a quick fix for liquidity, they are often predatory lending traps that can lead to a second cycle of debt. Taking on one of these high-cost loans can actually hurt your chances of a traditional refinance later, as mortgage underwriters may see it as a sign that you are still struggling to manage your finances.

The Danger of New Debt and Hard Inquiries

One of the most frequent mistakes homeowners make is taking out a new car loan or opening several retail credit cards just months before applying for a refinance. Every time you apply for credit, it triggers hard credit inquiries, which can cause your credit score to dip temporarily.

More importantly, new debt increases your debt-to-income ratio. Even if you can afford the monthly payment, a new $500 car payment could be the factor that pushes your debt levels too high for mortgage approval. It is best to keep your credit "frozen" in its current state making on-time payments on existing accounts without adding anything new until your mortgage refinance is officially closed. By keeping your financial profile stable and quiet, you demonstrate the discipline that lenders are looking for in a post-bankruptcy borrower.

Your Financial Fresh Start

Bankruptcy is a challenging experience, but it is important to remember that it is a speed bump on your financial journey, not a dead end. Your home remains a powerful engine for recovery, and with the right strategy, you can turn your existing equity into a platform for long-term stability. Whether your goal is to eliminate high-interest debt, lower your monthly overhead, or simply move past the restrictions of a court-ordered plan, the opportunity for a reset is well within reach.

Because every bankruptcy filing and recovery timeline is unique, the best first step is to obtain a personalized Home Equity Review. This assessment looks at your specific discharge dates, current property value, and credit goals to determine exactly when and how you can qualify for the best possible terms.

As a Mortgage Advisor specializing in complex credit scenarios and refinancing, I am here to help you navigate these guidelines with confidence. Don't let the paperwork of the past prevent you from securing your future. Contact me today to discuss your options and take the first step toward your financial fresh start.