If you are struggling with high-interest debt, you are likely facing a stressful paradox. You know that consolidating your balances into one manageable payment is the best way to save your financial future, yet you hesitate because you’ve heard it might "ruin" your credit score. It feels like you have to choose between getting out of debt and keeping a healthy credit profile. The reality, however, is much more encouraging.

In the world of mortgage planning, debt consolidation isn't just about moving numbers around; it is a strategic tool to improve your financial stability. From a professional advisor's perspective, the most effective way to do this is by leveraging your home. Options like a Cash-out Refinance or a Home Equity Line of Credit (HELOC) allow you to use your home’s value to pay off high-interest credit cards. This replaces "bad debt" with a structured, lower-interest mortgage payment, which significantly lowers your debt-to-income (DTI) ratio, a key factor lenders look at when you apply for any future financing.

Will your score drop? Probably, but only by a few points and only for a short time. When you apply for a new loan, there is a minor FICO score impact due to the credit check. However, once those high-interest credit card balances hit zero, your credit utilization ratio (how much of your limit you are using) plummets. For most homeowners, this results in a much higher credit score within six to twelve months than they ever had while carrying a heavy debt load.

Understanding the "Short-Term Dip": Why Your Score Drops Initially

When you decide to consolidate your debt, it is natural to monitor your credit score closely. You might notice a small, immediate decline in your numbers. While this can be frustrating, it is a standard part of the process and does not mean your financial plan is failing. Understanding why this happens can help you stay the course without unnecessary worry.

The Impact of Hard Inquiries

The first reason for a temporary dip is the hard credit pull. When you apply for a debt consolidation loan or a mortgage refinance, the lender must review your full credit report to determine your eligibility. This is known as a "hard inquiry." Unlike a soft pull which happens when you check your own score a hard inquiry informs credit bureaus that you are seeking new credit applications.

Each hard inquiry typically takes fewer than five points off your score. For most borrowers, this is a minor trade-off. These inquiries remain on your report for two years, but they usually only affect your actual score for the first twelve months. As a mortgage professional, I often remind clients that a single inquiry is a small price to pay for the thousands of dollars in interest they will save by consolidating high-interest credit card debt.

Changes to Your Credit History Length

The second factor is the average age of your accounts. Credit scoring models reward stability and long-term relationships with lenders. When you open a new consolidation loan or a new mortgage, you are essentially adding a "brand new" account to your profile. This reduces the overall average credit history length of all your accounts combined.

Think of it like a grade point average: if you have three older accounts that have been open for ten years and you add one new account, your average age drops. Since "length of credit history" accounts for about 15% of your total FICO score, this change can cause a slight, temporary decrease.

New Debt vs. Old Debt

Finally, your score may react to the fact that you have a new obligation. Credit bureaus see a new loan as a new risk until you prove you can handle the payments. However, this is where the "dip" ends and the recovery begins. As soon as you begin making on-time payments on your new consolidation loan and your old credit card balances are reported as zero, the positive factors will begin to outweigh these initial minor setbacks.

The "Long-Term Win": How Consolidation Boosts Your Score

While the initial drop in your score might catch your attention, the long-term benefits of debt consolidation are far more significant. For most homeowners, consolidating high-interest debt into a single mortgage or home equity loan is one of the fastest ways to rebuild a damaged credit profile. Here is how the transition from many small debts to one structured loan creates a "win" for your credit health.

Improving Your Credit Utilization Ratio

The single most powerful benefit of consolidation is the change to your credit utilization ratio. This term refers to how much of your available credit card limits you are currently using. In the eyes of credit bureaus, carrying high balances on multiple credit cards is a red flag. If your cards are "maxed out" or even half-full, your score will suffer.

When you use a home equity loan or a refinance to pay off those cards, you are shifting your debt from revolving debt to an installment loan. Revolving debt, like credit cards, heavily penalizes high utilization. Installment loans, like a mortgage, do not. By paying off your credit card balances in full, your utilization drops to 0%, which can often result in a massive and rapid increase in your credit score sometimes by dozens of points in just one or two billing cycles.

Protecting Your Payment History

Your payment consistency is the most important factor in your credit score, accounting for 35% of the total calculation. Managing five, seven, or ten different credit card due dates every month is difficult. It only takes one forgotten payment or one tight month to result in a late fee and a major hit to your credit report. A single payment that is 30 days late can stay on your record for seven years.

By consolidating, you replace those multiple stressors with one predictable monthly payment. Because this new payment is usually much lower than the combined total of your previous bills, it becomes easier to manage within your budget. This simplicity virtually eliminates the risk of accidental late payments, ensuring your history remains spotless and your score continues to climb.

Diversifying Your Credit Mix

Credit scoring models also look at your credit mix. Lenders like to see that you can handle different types of debt responsibly. Many people who struggle with debt only have credit cards on their profile. By adding a structured installment loan especially one tied to home equity you are demonstrating that you can manage a more sophisticated type of credit. This diversity shows financial maturity and can provide a small but steady boost to your overall rating.

In summary, while consolidation moves the debt from one place to another, it changes the character of that debt in the eyes of the credit bureaus. You go from being a "high-risk" borrower with maxed-out cards to a "stable" borrower with a well-managed mortgage and plenty of available credit. Over time, this shift creates a foundation for a much stronger financial future and a credit score that reflects your true stability.

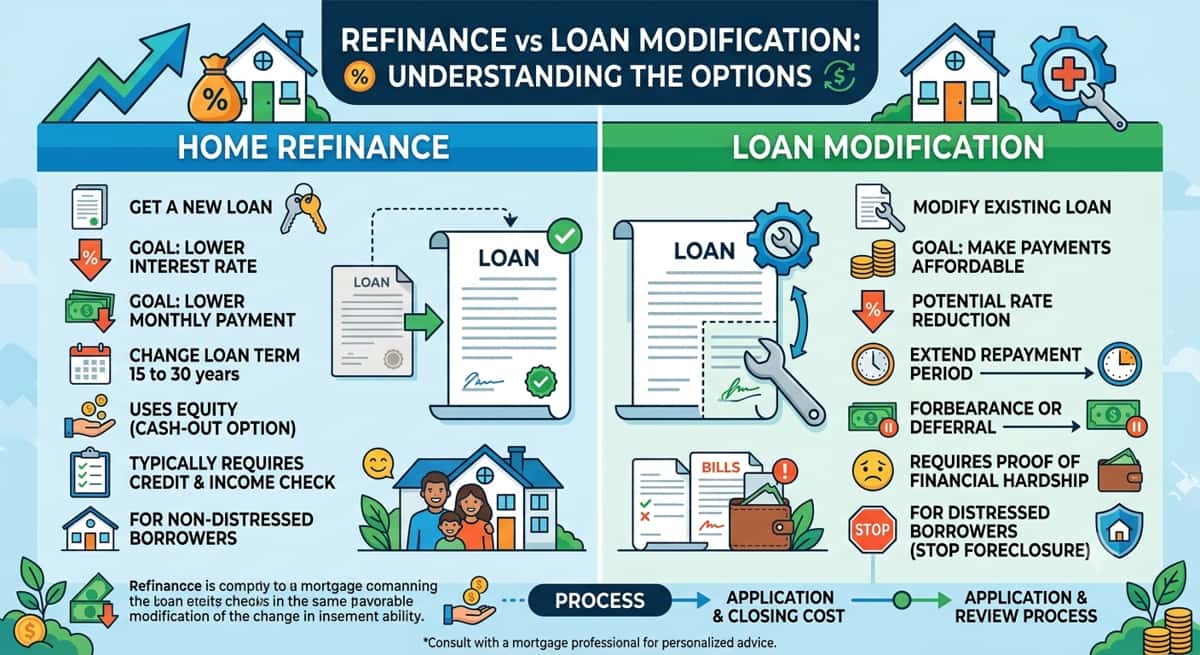

Deep Dive: Home Equity vs. Personal Loans for Consolidation

When you are ready to consolidate your debt, you generally have two main paths: using the equity in your home or taking out an unsecured personal loan. Both options can help simplify your finances, but they operate very differently in terms of risk, cost, and long-term impact on your household budget.

Comparing the Risks: Secured vs. Unsecured

The most critical difference between these two options is collateral. A personal loan is typically "unsecured," meaning it is backed only by your promise to pay. If you miss payments, your credit score will suffer, but your physical assets are not directly at risk.

In contrast, a HELOC (Home Equity Line of Credit) or a home equity loan is "secured" by your property. This means your home serves as collateral. While this allows lenders to offer much lower interest rates, it also means that failing to make payments could eventually lead to foreclosure. This is a significant responsibility that requires a stable income and a disciplined budget.

The Power of the APR Comparison

The primary reason homeowners choose equity-based consolidation is the massive difference in the APR comparison. As of March 2026, the financial landscape shows a stark divide:

Credit Cards: Average interest rates are hovering between 20% and 25%.

Personal Loans: Unsecured loans for those with good credit typically range from 11% to 15%.

Home Equity Options: Rates for HELOCs and home equity loans are significantly lower, often ranging from 6.5% to 8.5%.

By switching from a 24% credit card to a 7.5% home equity option, you aren't just lowering your payment; you are fundamentally changing how much of your money goes toward the principal balance versus the bank's interest charges.

Refinancing Strategy: The Cash-Out Option

Another powerful tool is the Cash-out refinance. Unlike a HELOC, which sits on top of your existing mortgage as a second payment, a cash-out refinance replaces your current mortgage entirely. You take out a new loan for a larger amount than what you currently owe, receive the difference in cash, and use that cash to pay off your high-interest debts.

This strategy is often preferred by those who want the simplicity of a single monthly housing payment rather than managing a first mortgage and a second equity line. It also allows you to lock in a fixed interest rate for the long term, providing protection against future market fluctuations.

Understanding Equity-to-Value

To qualify for these home-based options, lenders look at your equity-to-value ratio. Most lenders require you to keep at least 15% to 20% of your home's value as a "cushion." For example, if your home is worth $400,000, a lender might allow you to borrow up to a total of $320,000 (80% of the value) between your primary mortgage and your consolidation loan.

Choosing between a personal loan and a home-equity-based solution depends on your comfort level with using your home as a tool. If you have significant equity and a solid plan to stay in your home, the interest savings from a mortgage-based solution are often too large to ignore.

The "Trap" to Avoid: Closing Old Accounts

Once you have successfully consolidated your debt and see a zero balance on your credit cards, your first instinct might be to close those accounts forever. It feels like a symbolic victory a way to ensure you never fall back into the same debt cycle. However, from a credit-scoring perspective, closing those accounts is one of the most common mistakes a borrower can make. Doing so can accidentally reverse the progress you’ve made.

The Impact on Credit Age and Limits

Credit scoring models rely heavily on account longevity. These models favor consumers who have managed credit responsibly over a long period. When you close a credit card that you’ve held for five or ten years, you are essentially telling the credit bureaus to stop counting those years of history toward your average. Over time, this causes the "age" of your credit profile to shrink, which can lead to a sudden drop in your score.

Furthermore, closing an account immediately reduces your total available credit limit. Imagine you have $20,000 in total credit limits across four cards. If you close two of them with $5,000 limits each, your total available credit drops to $10,000. If you ever use a credit card in the future, your "utilization percentage" will look much higher because your total "bucket" of available credit is smaller. Keeping the accounts open provides a safety net that keeps your utilization ratio low and healthy.

Instead of closing the accounts, many financial experts recommend the "Sock Drawer" method. This involves keeping the physical credit card in a safe place at home like a sock drawer rather than in your wallet. By keeping the account open but unused, you maintain your account longevity and your high credit limit without the daily temptation to spend.

To prevent the bank from closing the account due to inactivity, you can set up one small, recurring monthly bill (like a streaming subscription) to be paid by the card, and then set the card to "Auto-Pay" from your checking account. This keeps the account active and reporting positive data to the credit bureaus every month, helping your score grow while you focus on paying down your new consolidation loan.

Case Study: A Real-World Mortgage Refinance Scenario

To understand how debt consolidation works in practice, let’s look at a typical scenario for a homeowner in the United States. Consider "Sarah," a professional who owns a home valued at $450,000 with a $300,000 mortgage balance. Over the last few years, Sarah accumulated $40,000 in high-interest credit card debt across four different cards to cover home repairs and emergency expenses.

The "Before" Picture

Sarah was struggling with a combined monthly credit card payment of $1,200. Because her interest rates averaged 22%, very little of that money was actually reducing her balances. Her credit cards were nearly maxed out, which kept her credit score stuck at 660. She felt like she was treading water, unable to save for the future because her monthly cash flow was entirely consumed by interest.

The Strategy: Cash-Out Refinance

Sarah worked with a mortgage advisor to perform a Cash-out Refinance. She took out a new mortgage for $350,000 at a 6.8% interest rate. This new loan paid off her old $300,000 mortgage and provided $50,000 in cash. She used $40,000 to wipe out her credit cards completely and kept $10,000 as an emergency fund to ensure she wouldn't need to use those cards again.

The "After" Picture: Monthly Cash Flow

By folding her high-interest debt into her mortgage, Sarah’s total monthly housing payment increased by about $350. However, she no longer had to pay the $1,200 in credit card bills.

Monthly Savings: $850 in immediate cash flow.

Interest Savings: She went from paying roughly $8,800 a year in credit card interest to approximately $2,700 in additional mortgage interest, a massive annual gain.

FICO Score Progression

The impact on Sarah’s credit score was dramatic.

Month 1: Her score dipped to 655 due to the hard credit inquiry and the new loan account.

Month 3: Once the credit bureaus reported her credit card balances at $0, her score jumped to 715.

Month 12: After a year of consistent, on-time mortgage payments and keeping her credit card balances at zero, her score reached 740.

It is important to remember that Sarah’s results are a snapshot. While this scenario is common, individual results will vary based on your starting score, your specific home equity, and your ability to maintain healthy financial habits after the consolidation is complete. Using your home as a tool requires a long-term commitment to staying debt-free.

Strategic Checklist: Is Consolidation Right for You?

Deciding to consolidate your debt using your home is a major financial move. While the math often makes perfect sense, success depends on more than just interest rates. Before moving forward, use this checklist to determine if this strategy aligns with your current situation and long-term goals.

Criteria for a Successful Consolidation

Sufficient Home Equity: Most lenders look at your loan-to-value (LTV) ratio. To qualify for the best rates, you generally need to have at least 20% equity remaining in your home after the new loan is taken out.

Stable Monthly Income: Because you are moving unsecured debt (credit cards) into a secured loan (your mortgage), you must be certain you can meet the new monthly payment. Lenders will verify this by checking your debt-to-income requirements to ensure you aren't overextending yourself.

A Solid Credit Foundation: While you don't need perfect credit to consolidate, having a score in the mid-600s or higher will help you secure a lower interest rate that makes the math work in your favor.

When You Should Wait

Consolidation is a tool to manage debt, not a cure for overspending. You should reconsider or delay consolidation if:

The Habits Haven't Changed: If the debt was caused by lifestyle spending rather than an emergency or one-time expense, consolidation might only provide a temporary fix. Without financial discipline, there is a high risk of running the credit card balances back up while still owing the new consolidation loan.

Short-Term Moving Plans: If you plan to sell your home in the next year or two, the closing costs associated with a refinance might outweigh the interest savings you would gain in that short window.

Ultimately, the goal is to use your home's value to create a fresh start. If you have the equity and the discipline to keep your credit cards at zero, consolidation can be the bridge to a debt-free life.

Conclusion & The Path Forward

Managing debt is one of the most significant hurdles to long-term financial freedom, but it is a hurdle you can clear. It is important to remember that credit scores are resilient. While the transition to a consolidation loan might cause a minor, temporary dip, your score is designed to bounce back stronger as your overall debt burden decreases.

Consolidating high-interest debt into your home equity is more than just a quick fix for monthly stress; it is a strategic tool for long-term wealth building. By drastically reducing the amount of money you pay in interest every month, you free up cash that can be redirected toward savings, retirement, or paying down your home faster. You are essentially taking control of your financial narrative and putting your home’s value to work for your future.

The best way to see how these numbers apply to your specific situation is to speak with a professional. Every homeowner’s equity and credit profile are unique. If you are ready to explore how a tailored consolidation plan can raise your score and lower your monthly expenses, consider scheduling a Credit Strategy Session. A Mortgage Advisor can help you compare your equity options and map out a clear, predictable path to a debt-free life.