As a professional Loan Officer specializing in the intricate world of mortgage consulting, I've guided countless clients through financing everything from simple condos to complex cooperative purchases across the USA. My specific expertise lies in navigating the complexities of refinancing and structuring Home Equity loans, areas where precise documentation is not just a formality, but the foundation of a successful transaction.

When you're buying or refinancing a property, the time between loan application and final closing can feel like an eternity. While most borrowers focus on credit checks and interest rates, the single biggest factor that dictates your closing timeline is the proper preparation and approval of documentation. This is especially true when comparing a standard condo closing to a detailed co-op closing.

Real estate finance is inherently a "Your Money or Your Life" (YMYL) subject.1 Mistakes in documentation can lead to costly delays, loss of rate locks, or even the collapse of a deal, impacting your financial stability significantly.

The purpose of this guide is to demystify these two ownership models and shine a light on the specific documentation differences that frequently slow down closings. We will break down key concepts like the standard title report for condos versus the unique requirements for stock certificates and a proprietary lease in a co-op. Understanding these distinctions—and the corresponding lender requirements—is the crucial first step to ensuring your closing proceeds on time and without financial surprises. Let's look beyond the purchase price and focus on the paperwork that actually secures your new home or refinancing terms.

Ownership 101: Legal and Financial Foundations of Co-ops vs. Condos

To understand why the documentation requirements for closing are so vastly different, you must first grasp the core distinction in how these two property types are legally owned. This foundational difference dictates everything that follows, particularly how a lender structures your mortgage or home equity loan.

Condo Ownership: Fee Simple and The Deed

When you purchase a condo, you are buying real property.1 You acquire fee simple ownership—the highest form of property ownership recognized in law—over the specific unit itself, including the airspace and the structural components within the unit’s defined boundaries.

Your ownership is formally established by a Warranty Deed, which is recorded with the county or municipal government. This deed is the most important closing document, as it legally transfers title to you. Additionally, your ownership includes a percentage of the common elements of the building (e.g., lobby, gym, roof).

While you own the physical real property, the community is governed by a Homeowners Association (HOA). Your lender will require review of the Declaration of Condominium, By-laws, and current HOA Documents to ensure the association is financially sound and adheres to federal lending guidelines regarding things like owner-occupancy rates and reserve funds. This ownership structure is straightforward and closely aligns with buying a detached house, making the financing and title process relatively standardized.

Co-op Ownership: Shareholder Status and Proprietary Lease

In contrast, when you "buy" a co-op, you are not buying real property. You are purchasing shares of stock in a private corporation that owns the entire building. Therefore, your ownership is considered personal property.

Your possession of the physical unit is granted via two crucial documents: a Stock Certificate (representing your shares in the corporation) and a Proprietary Lease (a long-term lease that gives you the right to occupy a specific unit). Neither document is recorded in the same manner as a Deed.

Since the corporation holds the deed to the building, your lender's security interest is more complex. The co-op often has an underlying mortgage on the entire property. The lender financing your purchase must have the corporation sign a Recognition Agreement (sometimes called an Aztec Agreement or Lender's Agreement). This document acknowledges the lender’s lien against your shares and lease and outlines the procedures the co-op board must follow if you default. This reliance on the board and corporate structure is the primary source of the unique documentation requirements that slow down the co-op closing process.

The Condo Closing Checklist: Standardization and Speed

The closing process for a condo typically follows a familiar, standardized path, closely resembling that of a single-family home. This established framework contributes significantly to a smoother, faster process compared to co-op closings, making it the benchmark against which the co-op gauntlet is measured.

Standard Title and Appraisal Requirements

Because a condo is considered real property, the legal transfer is governed by traditional real estate procedures. A crucial element of the condo closing checklist is the comprehensive Title Search. This process, executed by a title company, verifies that the seller has the legal right to transfer ownership, identifies any existing liens (mortgages, judgments, unpaid taxes), and ensures the property is free of undisclosed claims. The resulting Title Insurance Commitment guarantees a clear and marketable title, protecting both you and your lender.

In terms of valuation, the appraisal process for a condo is equally standardized. Lenders require an independent valuation prepared by a licensed appraiser using the Uniform Residential Appraisal Report (URAR Form 1004). The appraiser analyzes comparable sales ("comps") within the complex and surrounding market to determine the property's fair market value. The standardization of both the title and appraisal documentation means that your lender's underwriting department can quickly review and approve these packages, avoiding the need for specialized legal or corporate review that often causes co-op delays. This emphasis on standard documentation expedites the entire financing timeline.

The Streamlined Homeowners Association (HOA) Documentation

While the title and mortgage are focused on your specific unit, the lender must also approve the financial health of the community itself. This review focuses on the Homeowners Association (HOA) documentation.

Key HOA documents required for lender review include:

- The current budget and financial statements.

- Confirmation of adequate reserve funds (many lenders have minimum reserve requirements).

- The master insurance policy covering the building's common elements.

A specialized mortgage advisor pays close attention to specific lender requirements regarding the HOA's master policy, such as ensuring that the deductible limits are acceptable. If the policy deductible is too high, it can impact the safety and marketability of the loan. Critically, because an HOA is structured solely to manage the common elements, its documentation is generally less invasive and is handled by the management company rather than an active board vote. This process is typically mechanical and much faster than securing approval from a Co-op Board, which is mandated to review and approve the personal finances of the prospective buyer as a new shareholder.

The Co-op Closing Gauntlet: Documentation Differences That Slow Down Closing

The greatest source of complexity and delay when financing a cooperative unit stems from its corporate structure. Unlike a condo, where the lender primarily evaluates your personal financial health and the property’s value, a co-op closing requires a meticulous, multi-layered approval process involving the co-op board itself. This process often feels like a "gauntlet" and is the central reason why co-op closings take significantly longer than condo closings.

Lender Requirements: The Co-op Questionnaire and Recognition Agreement

When dealing with a co-op, the lender's security interest is not a traditional mortgage on real property, but a lien against your personal property (your shares of stock and proprietary lease). To secure this lien, two mandatory pieces of documentation are required from the co-op corporation itself, and their execution is a primary point of friction and delay:

- The Co-op Questionnaire: This lengthy document, sometimes spanning over 20 pages, must be completed and signed by the co-op management company or board. It demands detailed information about the building's finances, insurance coverage, percentage of owner-occupancy, and whether there is an underlying mortgage on the entire building. Any incomplete or slow responses can halt your loan underwriting instantly, as the lender must ensure the corporation meets specific financing criteria.

- The Recognition Agreement (Aztec/Lender’s Agreement): This is the single most critical document for the lender. It legally binds the corporation and the lender, confirming the bank’s status as a secured creditor. It grants the lender the right to take possession of your shares and proprietary lease if you default on your mortgage, and prevents the co-op from approving a subordinate lien (like a Home Equity Loan) without the first lender’s consent. Waiting for the co-op's attorney to review and sign this agreement is often a bottleneck that independent lenders cannot speed up.

The Board Application and Approval Package

Beyond the lender's requirements, the co-op board has its own exhaustive review process, which focuses strictly on the borrower's personal suitability as a shareholder. The Board Application and Approval Package requires extensive personal documentation, including:

- Multiple years of tax returns and financial statements.

- Detailed letters of explanation for any financial anomalies.

- Permission for the board to run its own credit reports and background checks.

- Numerous personal and professional references.

As a Loan Officer, I advise clients to prepare a "Board-proof" financial package—meticulously organized, accurate, and completely transparent—well before the loan is ready. Even if your financing is fully approved by the bank, the co-op board’s timetable for reviewing this package and conducting the subsequent Board Interview (where applicable) operates entirely independently. This subjective, scheduled, and often slow internal corporate process is a major cause of closing delays, as it can take weeks or even months regardless of how quickly your mortgage is approved.

Unique Co-op Closing Documents: Stock, Lease, and UCC Filings

The actual closing documentation in a co-op is fundamentally different from a condo, where you receive a Deed and Title Insurance.

- Instead of a Deed, you receive the Stock Certificate and the fully executed Proprietary Lease.

- Instead of standard real estate Title Insurance (which covers real property liens), your lender protects its interest by filing a financing statement, known as a UCC-1 (Uniform Commercial Code) filing, with the appropriate state or county authority. This filing serves as a public notice of the lender’s lien against your shares of stock.

These unique documents require specialized attorneys and title agents familiar with personal property transfers, which can sometimes lead to additional closing complexities and slower scheduling when compared to the universal process of recording a deed.

The Mortgage Advisor's Perspective: Financing Pitfalls

As your Mortgage Advisor, my job is to anticipate the financial roadblocks that traditional lenders might miss, especially when dealing with the unique structures of co-ops and complex condos. For clients seeking to tap into their equity through Home Equity loans or Refinancing, the documentation pitfalls are magnified because the lender is re-entering a relationship with both the borrower and the corporation.

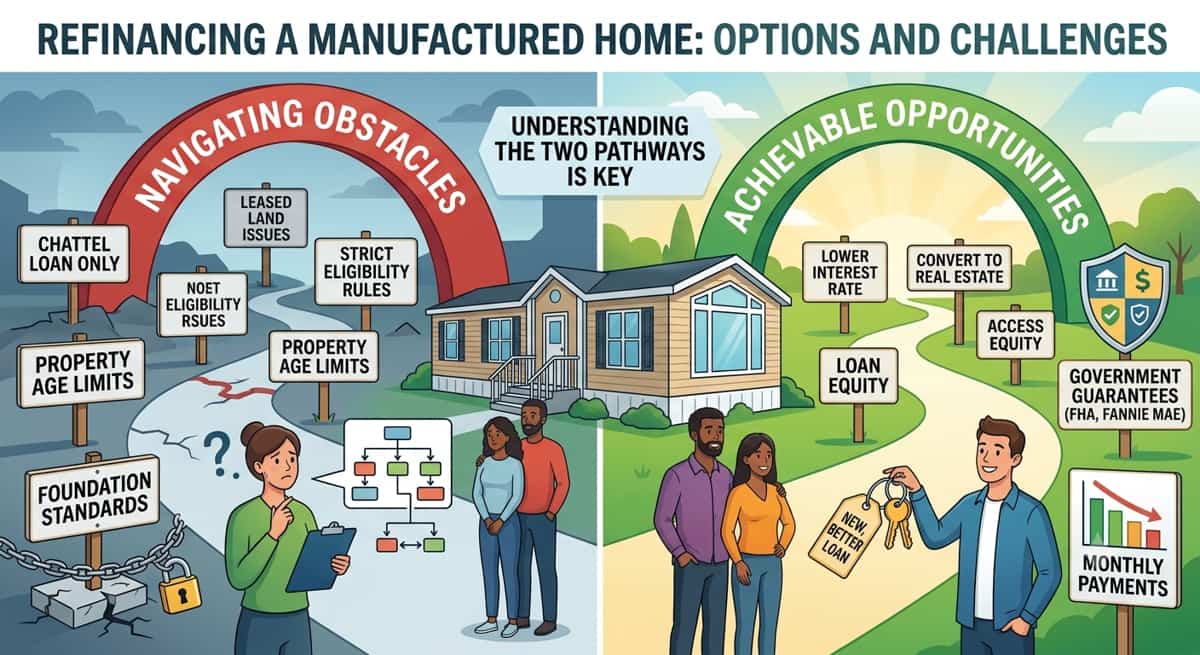

Refinancing a Co-op: Why the Documentation Clock Starts Over

The most surprising hurdle for current co-op owners seeking to refinance is that the entire documentation clock effectively resets. You are required to submit a full new loan application, and the bank must re-establish its legal standing. This means obtaining a new Co-op Questionnaire and executing a brand-new Recognition Agreement with the board. Even more surprising, the co-op board may require you to submit a fresh application or an abbreviated review package, ensuring your current financial health meets their standards before they allow the new lender to place its lien.

This is especially crucial for Home Equity Loans (HELOCs). Because the co-op structure has an underlying mortgage on the entire building and the first mortgage lender has specific rights via the Recognition Agreement, getting approval for a second loan (a subordinate lien) can be exceptionally challenging, and sometimes structurally impossible, depending on the co-op's by-laws. Furthermore, when structuring any co-op loan, we must strictly adhere to the lender's Loan-to-Value (LTV) and building reserve requirements—if the co-op's cash reserves have dropped since your last closing, your refinancing may be denied, regardless of your personal finances.

The Appraisal Trap: Comparables and Lender Compliance

The valuation process often presents a significant documentation trap, especially for co-ops. While a condo appraisal relies on the sales price of comparable units (real property), a co-op appraisal must assess the value of shares, which is not always directly comparable. Co-op appraisers must use sales data that reflects the value of the stock and proprietary lease, often creating a more limited pool of reliable comparables and potentially requiring more documentation to justify the final valuation.

I regularly counsel clients on navigating lender compliance issues related to the building structure itself. Lenders have strict conforming and non-conforming standards for co-op buildings. These often relate to the percentage of units rented out (investor ratios), the amount of commercial space in the building (e.g., ground-floor retail), or pending litigation against the co-op. If the building’s documents show non-compliance with these rules, the lender will deny the mortgage or Home Equity application, even if the unit is perfect. This due diligence on the building's corporate documents is a non-negotiable step that slows the process but is vital for financial security.

Expert Strategies for a Smooth Closing: How to Mitigate Delays

The most successful real estate closings, particularly those involving the complex documentation of a co-op or a refinance, are characterized by proactive strategy. By understanding the potential bottlenecks, you can take immediate action to mitigate delays and move towards a smooth, on-time closing.

Pre-Emptive Document Gathering

The greatest delay in any co-op or condo closing is often the wait time for third-party documentation. Smart buyers and refinancers must operate on dual tracks:

- For Buyers: Do not wait for your loan pre-approval to begin securing the co-op board application and gathering the required personal financial documents (tax returns, reference letters, bank statements). Submitting the complete board package simultaneously with your loan application shaves weeks off the process.

- For Sellers/Refinancers: If you currently own a co-op, ensure your original Stock Certificate and Proprietary Lease are readily accessible. Having your existing documentation in hand allows the title/closing agent to start their review immediately, preventing delays while tracking down old documents. Organization is your most powerful tool against closing bottlenecks.

Selecting the Right Board-Approved Lender

Choosing a lender who is simply able to finance a co-op is not enough; you need one with deep, established experience in the local market. Many co-op corporations maintain relationships with "preferred counsel" or lenders who have financed numerous units in the building. A lender who is familiar with a building's specific management company and often-requested documentation can offer a streamlined closing process. They will already have the correct contacts, know the unique building requirements, and can anticipate the demands of the Recognition Agreement, avoiding errors that can cost valuable time.

Due Diligence on the Building's Financial Health

Before you spend money on a commitment letter or a board application, your advisor must conduct thorough due diligence on the building's financial health. This involves meticulously reviewing the co-op's annual budget, balance sheet, and financial statements. We must confirm that the building meets the lender’s stringent underwriting requirements for reserves and overall financial stability. A financially distressed co-op or a building with pending major litigation will not be approved by the lender, regardless of how strong your personal financial profile is. Addressing these red flags early prevents you from wasting time and money on a property that is unfinanceable.

Conclusion: Your Next Step to a Clear Closing

The fundamental difference between closing on a condo and closing on a co-op boils down to one factor: the documentation required by the co-op corporation. While condo closings are expedited by standardized title searches and HOA reviews, co-op closings are uniquely slowed by the necessity of obtaining the board's personal Board Approval and securing the critical Recognition Agreement for the lender. These corporate hurdles are the primary source of delays. Navigating these requirements demands specialized knowledge. If you are a USA-based homeowner seeking to leverage your assets through Home Equity or planning a complex Refinancing in a cooperative market, consulting a specialized Mortgage Advisor is your best strategy. We ensure your documentation is flawless from day one, turning a potential gauntlet into a clear path to closing.