As we navigate the 2026 mortgage landscape, American homeowners find themselves in a unique position. While the aggressive rate-hike cycles of previous years have cooled, the "lock-in effect" where homeowners are reluctant to part with the ultra-low mortgage rates secured earlier this decade remains a dominant force. This has fundamentally shifted the strategy for accessing tappable equity.

In my decade of experience as a Senior Mortgage Consultant, I’ve seen the industry pivot away from the traditional cash-out refinance. Today, savvy borrowers are increasingly choosing a Home Equity Line of Credit (HELOC). The reason is simple: why refinance your entire primary mortgage at 6% or 7% when your current rate is 3%? A HELOC allows you to preserve that low-interest foundation while accessing the liquidity you need for home improvements or debt consolidation.

However, this strategy introduces a new challenge: the "paralysis of choice." As a mortgage advisor, the most frequent question I receive is whether to opt for the immediate savings of a variable-rate HELOC or the long-term security of a fixed-rate lock. In an era where the Federal Reserve’s "higher for longer" stance can shift into a series of rapid cuts, the cost of a wrong choice can be thousands of dollars in interest.

The following guide draws on current market data and lender-specific nuances to help you determine which equity product aligns with your 2026 financial goals, ensuring you leverage your home’s value without compromising your financial stability.

Defining the Mechanics: How HELOCs Work in 2026

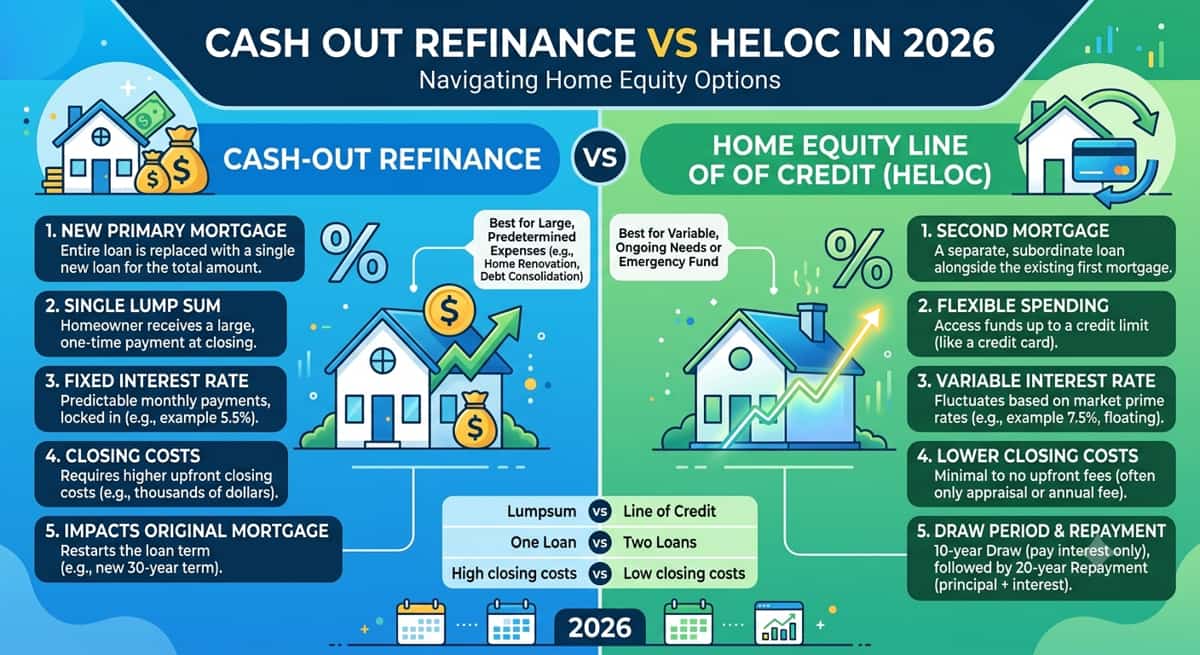

Understanding a Home Equity Line of Credit (HELOC) requires looking at it as a two-phase financial instrument. Unlike a standard loan where you receive a lump sum and begin full repayment immediately, a HELOC functions more like a high-limit credit card secured by your home.

The Draw Period vs. The Repayment Period

Most modern HELOCs in the US are structured with a 10-year draw period followed by a 20-year repayment period.

The Draw Period: During these first 10 years, you can withdraw funds as needed up to your credit limit. The hallmark of this phase is the interest-only payment option. This provides significant monthly cash-flow flexibility, as you aren't required to pay down the principal balance yet.

The Repayment Period: Once the draw period ends, the "window" closes. You can no longer take out money, and your monthly payment will reset to include both principal and interest.

The Role of the Prime Rate and the Index

The interest rate on a variable HELOC isn't arbitrary; it is a mathematical formula: Index + Margin = Your APR.

The Index: Most lenders use the WSJ Prime Rate as their index. This index is directly tethered to the Fed funds rate. When the Federal Reserve meets (as they did in January 2026 to hold rates steady at 3.50%–3.75%), the Prime Rate typically stays in lockstep (currently 6.75%).

The Margin: This is a fixed percentage added by the lender based on your creditworthiness and LTV (Loan-to-Value) ratio. While the index fluctuates with the economy, your margin is set at closing and remains constant.

Because these rates are variable, a shift in the national economy can change your monthly obligation within one to two billing cycles, making it essential to understand your "rate cap" or the maximum interest rate your loan can legally reach.

The Variable-Rate HELOC: High Risk, High Reward?

The variable-rate HELOC is the standard offering in the US mortgage market. Its primary appeal lies in its initial affordability, but as any seasoned mortgage consultant will tell you, that entry-level rate comes with a built-in exposure to the broader economy.

The Mathematical Reality: Index + Margin

As established, your interest rate is a moving target. It is fundamentally tied to the Wall Street Journal (WSJ) Prime Rate. If the Federal Reserve adjusts the Fed funds rate to combat inflation or stimulate growth, your HELOC rate will move in near-perfect lockstep. Most lenders offer a "teaser rate" for the first 6 to 12 months often significantly below the current Prime Rate to attract borrowers. Once that introductory period expires, your rate reverts to the Index (Prime) + Margin (your fixed spread).

The Advantages: Capturing the Downside

The most significant benefit of a variable-rate line is the potential for "rate relief." If you believe that the Federal Reserve will enter a period of monetary easing in the next 18 months, a variable rate allows you to capture those savings automatically without the cost of refinancing. Furthermore, variable-rate HELOCs often feature lower (or zero) closing costs and no "conversion fees" compared to their fixed-rate counterparts. This makes them a highly liquid, low-friction tool for short-term financial needs.

The Disadvantages: The Volatility Tax

The "risk" in this high-reward scenario is monthly payment volatility. Unlike a fixed-rate mortgage, a variable HELOC has no ceiling other than the lifetime "cap" specified in your contract which is often as high as 18%. In a volatile economy, a 1% or 2% jump in the Prime Rate can lead to a substantial increase in your interest-only payments, potentially straining your debt-to-income (DTI) ratio and overall household budget.

Who Is the Ideal Candidate?

The variable-rate HELOC is an excellent strategic tool for specific borrowers. It is best suited for:

The Short-Term Borrower: Homeowners who intend to draw funds and pay them back in full within 12 to 24 months.

The Market Opportunist: Those with high discretionary income who can absorb a $200–$400 monthly payment increase without financial distress.

The Strategic Renovator: Borrowers using the funds for quick-flip projects or repairs that will be reimbursed by an insurance claim or a looming bonus.

For these individuals, the flexibility of the variable rate outweighs the long-term risk of a rate hike. However, if your repayment plan stretches into the next decade, the "reward" may quickly be eclipsed by the "risk."

The Fixed-Rate HELOC: Buying Peace of Mind

In a fluctuating economy, the fixed-rate HELOC stands out as the defensive player in your financial portfolio. While traditional HELOCs are synonymous with variable rates, many modern US lenders now offer a hybrid structure. This feature allows you to enjoy the flexibility of a line of credit while "locking in" specific balances at a predictable interest rate.

The Hybrid Structure: How the "Lock" Works

Unlike a standard Home Equity Loan which is a one-time lump sum a fixed-rate HELOC usually starts as a variable line. However, it gives you the option to convert a portion of your outstanding balance into a fixed-rate segment.

For example, if you draw $50,000 for a kitchen remodel, you can "lock" that $50,000 at today’s fixed rate for a set term (usually 5 to 20 years). The remaining available credit in your line remains variable and ready for use. You effectively create a "loan within a line," allowing for multiple fixed-rate segments under one single mortgage deed.

The Pros: Stability and Inflation Protection

The most compelling reason to choose a fixed rate is budget predictability. In an environment where the Federal funds rate might see unexpected spikes due to global inflation, a fixed-rate lock shields your monthly budget. Your principal and interest payments remain constant, regardless of what happens at the Federal Reserve's next meeting. This "set it and forget it" mentality is invaluable for homeowners on a fixed income or those with a strictly managed monthly cash flow.

The Cons: The Cost of Certainty

Peace of mind is rarely free. Fixed-rate HELOCs typically come with a higher initial APR compared to the "teaser" rates found on variable lines. You are essentially paying a premium for the lender to take on the interest rate risk. Furthermore, some institutions charge a "conversion fee" or a "lock fee" (ranging from $50 to $150) every time you move a balance from variable to fixed. Additionally, if market rates drop significantly, you are stuck at your higher fixed rate unless you pay a fee to unlock or refinance the segment.

Who Is the Ideal Candidate?

The fixed-rate option is a strategic move for the long-haul borrower. It is best suited for:

The Debt Consolidator: If you are rolling $30,000 of high-interest credit card debt into your home equity, a fixed rate ensures you can mathematically map out your path to a $0 balance over 5 or 10 years.

The Major Renovator: For structural additions or "forever home" upgrades where the repayment will likely span the full life of the loan.

The Risk-Averse Homeowner: Anyone who prioritizes the security of a guaranteed monthly payment over the potential but not certain savings of a variable rate.

Comparative Analysis: Side-by-Side Comparison

When deciding between a variable and fixed-rate HELOC, the choice often comes down to your tolerance for market fluctuations versus your desire for long-term savings. While a variable rate might offer the lowest entry point, the fixed-rate "lock" functions as a hedge against future inflation.

To simplify the decision-making process, the following table breaks down the core differences based on current 2026 lending standards.

HELOC Rate Structure Comparison

Feature | Variable-Rate HELOC | Fixed-Rate HELOC (Lock) |

Rate Type | Index (Prime) + Margin | Set APR for a specific term |

Monthly Consistency | High Volatility; payments can change monthly | Guaranteed Stability; payment never changes |

Initial APR | Lower (Often includes 6–12 month teaser) | Higher (Premium for price protection) |

Total Interest Cost | Unpredictable; depends on Fed funds rate | Predictable; calculated at time of lock |

Flexibility | Maximum; no fees to maintain variable status | Moderate; may involve "lock-in" fees |

Best For | Short-term draws (1–2 years) | Long-term repayment (5+ years) |

As a mortgage consultant, I often advise clients to look at their Debt-to-Income (DTI) ratio when reviewing this table. If a 2% increase in the variable rate would push your DTI above 43%, the fixed-rate option isn't just a preference, it's a necessary safeguard for your financial health.

Financial Implications: When to Choose Which?

In my role as a mortgage consultant, I’ve found that the "best" rate is secondary to the "best" timeline. To make the right choice, you must align your borrowing strategy with your specific financial objective. In 2026, two primary scenarios dominate the US market.

Scenario A: Home Renovations (The Short-Term Play)

If you are tapping into your equity for a kitchen remodel, a new roof, or a basement finish, a variable-rate HELOC is often the superior tool.

The Strategy: Renovations often involve "staged" expenses. You don't need all $50,000 on day one; you need $10,000 for materials, then $15,000 for labor a month later.

Why Variable Works: Because you only pay interest on what you actually draw, the lower initial "teaser" rates found in variable lines minimize your carrying costs during the project. If you plan to pay off the balance with an annual bonus or by selling another asset within 12–24 months, the risk of a long-term rate spike is negligible.

NLP Focus: Maintaining a healthy LTV (Loan-to-Value) ratio typically below 80% ensures you retain a "buffer" in case local property values shift during your renovation.

Scenario B: Consolidating High-Interest Debt (The Long-Term Play)

For homeowners looking to pay off $40,000 in credit card debt or high-interest personal loans, the fixed-rate lock is the safer, more strategic path.

The Strategy: Debt consolidation is a marathon, not a sprint. Most borrowers require 3 to 5 years to fully amortize a large consolidation balance.

Why Fixed Works: Credit card interest rates in 2026 remain significantly higher than home equity rates. By locking in a fixed HELOC rate, you eliminate the "moving target" of variable interest. This allows you to calculate exactly how much principal you are retiring each month.

The DTI Factor: Using a fixed rate protects your DTI (Debt-to-Income) ratio. If you chose a variable rate and market interest spiked, your required monthly payment could rise, potentially making it harder to qualify for other financing (like an auto loan) in the future.

The Credit Score Impact

Regardless of the scenario, how you use the line matters. A common misconception is that a HELOC is "just another mortgage." In reality, FICO models often treat a HELOC similarly to a revolving credit card.

NLP Focus: If you "max out" your line (e.g., drawing $45,000 on a $50,000 limit), your credit utilization climbs, which can cause a temporary dip in your credit score.

Advisor Tip: To minimize credit score impact, try to keep your balance below 30% of the total line limit, or use the fixed-rate lock feature, which some scoring models view more favorably as an "installment-style" debt.

Expert Insights: What the "Fine Print" Doesn't Tell You

In my years as a mortgage consultant, I’ve seen that the true cost of a HELOC isn’t always found in the APR. While the choice between variable and fixed rates is the primary focus, the "fine print" in your loan agreement can drastically alter your financial outcome.

The Danger of Balloon Payments

Some variable-rate HELOCs, particularly those offered by smaller credit unions or regional banks, may include a balloon payment clause. This means that at the end of your 10-year draw period, the entire remaining balance becomes due in a single lump sum. If you aren't prepared to pay off the balance or refinance into a new mortgage, you could face a sudden liquidity crisis. Always confirm whether your HELOC "fully amortizes" during the repayment period or if a balloon payment is lurking in the terms.

The "Inactivity" and "Early Closure" Fees

Lenders make money when you carry a balance. If you open a HELOC "just in case" but never draw from it, you might be hit with an annual inactivity fee (typically $50–$100). Furthermore, many US lenders include an early closure fee (or "recapture fee") if you close the line within the first 24 to 36 months. If you plan on selling your home soon, this could eat into your net proceeds at the closing table.

Leveraging the Fixed-Rate Loan Option (FRLO)

One of the most underutilized tools in 2026 is the Fixed-Rate Loan Option (FRLO). As a mortgage advisor, I often recommend this "hybrid" approach to clients who are unsure of future market directions. This allows you to keep the majority of your line variable for emergency access while carving out a $20,000 or $30,000 "slice" to be paid back at a fixed rate. It offers the best of both worlds: the agility of a line of credit with the disciplined repayment of a term loan.

A Critical Warning: Your Home is the Collateral

It is vital to remember that a HELOC is a secured debt. Unlike a credit card or a personal loan, your home is the collateral. If a sudden job loss or medical emergency prevents you from making payments especially if your variable rate has spiked the lender has the legal right to initiate foreclosure proceedings.

Before tapping into your equity, ensure you have an "exit strategy." Whether that is an emergency fund or a clear plan to sell the asset, never borrow more than your household budget can sustain under a "worst-case" interest rate scenario.

State-Specific Nuances & Tax Considerations

Deciding between a fixed or variable rate is a major step, but as a mortgage professional, I always remind my clients that the "true cost" of a HELOC is heavily influenced by where you live and how you use the funds. In 2026, two factors: the IRS and your local property market play a decisive role in your final return on investment.

Tax Deductibility: The "Substantial Improvement" Rule

Many homeowners assume HELOC interest is always deductible because it’s a mortgage product. However, under current 2026 IRS guidelines, interest is only deductible if the funds are used to "buy, build, or substantially improve" the home that secures the loan.

Qualifying: A kitchen gut-remodel, a new roof, or adding a bedroom suite.

Non-Qualifying: Consolidating credit card debt, paying for a wedding, or routine maintenance like repainting a fence.

If you use a variable-rate HELOC for debt consolidation, you lose the tax break, making the fixed-rate stability even more attractive to ensure your costs don't spiral.

Geography: Florida vs. Texas

Your location also dictates your tappable equity. In 2026, we see a massive divergence in appraisal values.

Florida: With rising insurance premiums affecting market velocity, lenders may be more conservative with Automated Valuation Models (AVMs), potentially requiring a full physical appraisal to hit your desired LTV.

Texas: Because Texas has strict "Homestead" laws (Article XVI, Section 50), you are generally capped at an 80% Combined Loan-to-Value (CLTV) for all home-secured debt. This means Texas homeowners often have less "wiggle room" and may prefer a fixed-rate lock to ensure they never exceed their repayment capacity in a tighter equity market.

Conclusion: Assessing Your Personal Risk Tolerance

Ultimately, the choice between a variable-rate and a fixed-rate HELOC isn’t about finding a "winner" in the market, it's about matching a financial product to your personal risk tolerance and repayment timeline.

If your goal is a quick home flip or a minor repair that you can pay off within 18 months, the variable-rate HELOC and its lower initial costs are likely your best strategic move. However, if you are consolidating high-interest debt or embarking on a major multi-year renovation, the fixed-rate lock provides the "sleep-well-at-night" factor that keeps your monthly budget shielded from the whims of the Federal Reserve.

As a final expert thought: tapping into your home’s equity is one of the most significant financial moves you can make. When you push your Combined Loan-to-Value (CLTV) ratio toward 80% or higher, your margin for error narrows. In these high-leverage situations, market volatility becomes a much larger threat. Before signing on the dotted line, I strongly recommend consulting with a professional mortgage advisor. We can run "stress test" scenarios on your budget to ensure that even if rates hit a 20-year high, your home and your financial future remains secure.