The American landscape of homeownership is undergoing a massive shift. As housing affordability remains a primary concern for many families, the humble backyard cottage is no longer just a space for a "granny flat" or a hobby workshop. Today, the Accessory Dwelling Unit (ADU) whether it’s a basement suite, a converted garage, or a detached carriage house has evolved into one of the most powerful financial assets a homeowner can own. By leveraging home equity to create these secondary spaces, savvy owners are finding a path toward supplemental income that can significantly offset a monthly mortgage payment.

In my decade of experience as a Mortgage Consultant specializing in high-leverage debt strategies, I have seen firsthand how an ADU can transform a borrower’s financial profile. The traditional struggle of qualifying for a higher loan amount often boils down to a single metric: the Debt-to-Income (DTI) ratio. Many homeowners sit on a goldmine of potential income but aren't aware that modern lending guidelines now allow us to "count" that future or current rent to help you qualify.

Whether you are looking to purchase a property with an existing unit or you are seeking to refinance to build one, understanding the mechanics of ADU rental income mortgage qualification is essential. Transitioning your property from a single-family residence into a multi-generational or income-producing powerhouse requires a strategic approach to financing. In this guide, we will break down the complex world of ADU lending to help you maximize your borrowing power and secure your financial future.

Can You Really Use ADU Income to Qualify?

The short answer is yes but the nuances of how you qualify depend heavily on the type of loan you are seeking and how the unit is classified. Historically, mortgage lenders were hesitant to consider income from a secondary unit on a single-family property, often viewing it as "unreliable." However, in response to the national housing shortage, there has been a significant regulatory shift.

The 2023-2024 Policy Shift

Significant updates from Fannie Mae and Freddie Mac between 2023 and 2024 have changed the game for homeowners. Fannie Mae, in particular, updated its eligibility requirements to allow rental income from an ADU on a one-unit principal residence to be used for qualifying income, even if the borrower doesn't have a prior history of being a landlord. This policy change was specifically designed to support housing affordability and "Missing Middle" housing. Freddie Mac followed suit with its Home Possible and Heritage One programs, recognizing that ADUs are vital for multi-generational living and financial stability.

Boarder Income vs. Rental Income

Understanding the distinction between "Boarder Income" and "Rental Income" is critical for your application's success:

Boarder Income: This typically refers to someone renting a room inside your primary living space. Most conventional guidelines are very restrictive with this, often requiring a long history of documented payments and only allowing it under specific "HomeReady" or "Home Possible" scenarios.

Rental Income: This applies to a distinct, legal ADU. Because an ADU has its own kitchen, bathroom, and entrance, it is treated more like a traditional rental property. This allows lenders to use a percentage of the projected or actual lease to pad your qualifying income.

The Impact on Your Borrowing Power

How much does this actually help? In mortgage underwriting, we look at your Debt-to-Income (DTI) ratio. If you earn $7,000 a month but have $3,500 in monthly debts (including your new mortgage), your DTI is 50% often the absolute ceiling for approval. However, if your ADU generates $1,500 in monthly rent, lenders typically apply a "vacancy factor" (usually 75% of the rent is usable), adding $1,125 to your qualifying income. This lowers your DTI significantly, potentially turning a "denied" application into an "approved" one, or allowing you to qualify for a much higher purchase price or refinance amount.

Understanding Fannie Mae and Freddie Mac ADU Guidelines

When navigating conforming loans, the two primary entities you need to understand are Fannie Mae and Freddie Mac. While both have expanded their criteria to support ADU financing, their specific "rulebooks" vary. As a Mortgage Consultant, I use their Automated Underwriting Systems (AUS)—Desktop Underwriter (DU) for Fannie and Loan Product Advisor (LPA) for Freddie to determine your eligibility instantly.

Fannie Mae: The HomeReady Advantage

Fannie Mae is often the "go-to" for homeowners looking to use ADU income on a 1-unit principal residence. Their HomeReady program is specifically designed for low-to-moderate-income borrowers, but its flexibilities extend to ADUs for all qualifying borrowers under certain conditions.

1-Unit Focus: Fannie Mae allows you to use rental income from an ADU on a one-unit primary residence to help you qualify for a purchase or a limited cash-out refinance.

Income Caps: A key technicality is that the qualifying rental income from the ADU cannot exceed 30% of the total monthly income used to qualify.

Experience Requirements: Unlike traditional investment properties, Fannie Mae does not always require a history of property management, making this accessible for first-time "house hackers."

Freddie Mac: Home Possible & Beyond

Freddie Mac’s guidelines are equally robust, particularly through the Home Possible mortgage. They have been pioneers in allowing ADU income to support a borrower’s Debt-to-Income (DTI) ratio.

Property Flexibility: Freddie Mac allows ADUs on 1-, 2-, and 3-unit properties. This is a significant distinction if you are looking at a duplex that also has a carriage house.

Zoning Requirements: Freddie Mac is often more flexible with "legal non-conforming" units. If the ADU was built legally but zoning laws have since changed, Freddie Mac may still allow the income if the appraiser confirms the unit is typical for the area.

Loan-to-Value (LTV) Ratios: Both agencies allow high LTV ratios (up to 97% for some programs), meaning you can qualify with as little as 3% down while using the projected rent to bolster your application.

Comparison at a Glance

Feature | Fannie Mae (HomeReady/Standard) | Freddie Mac (Home Possible/Standard) |

Max Units | 1-Unit Principal Residence | 1-, 2-, or 3-Unit Properties |

Income Limit | Rent max 30% of total qualifying income | Rent max 30% of total qualifying income |

Appraisal Form | Form 1004 + Form 1007 | Form 70 + Form 1000 |

Zoning | Must be legal (some exceptions for 1-unit) | Legal, legal non-conforming, or "illegal" with caveats |

By understanding these technical nuances, we can choose the specific "path of least resistance" for your loan. If one system flags a high DTI, the other’s specific treatment of conforming loan limits or rental vacancy factors might provide the approval we need.

Essential Requirements for Qualification: The "ADU Checklist"

Navigating the mortgage process with an ADU requires more than just a tenant and a lease. Lenders look for specific physical and legal characteristics to ensure the unit is a viable income-producing asset. To help my clients prepare, I’ve developed this "ADU Checklist" based on current federal underwriting standards.

The Physical Anatomy of a Qualified ADU

For a lender to recognize a space as an Accessory Dwelling Unit rather than just a "finished room," it must meet specific NLP-defined criteria:

Independent Entrance: The unit must have a separate entrance from the primary dwelling.

Kitchen Requirements: It must contain a permanent kitchen with a stove/range (or at least the hookups), a sink, and a refrigerator.

Bathroom Facilities: A full bathroom dedicated exclusively to the unit is required.

Living/Sleeping Area: There must be a designated space for living and sleeping that complies with local building codes.

The Documentation Trail: Proving the Income

When we submit your file to underwriting, the income isn't just "stated"—it must be documented. The requirements differ depending on whether the unit is already rented or if you are buying a home with a vacant ADU.

Lease Agreements: If the unit is currently occupied, you will need a fully executed lease agreement. If the unit is vacant, lenders will often accept a "projected" lease based on market data.

Appraisal Form 1004 & The Rental Addendum: This is the most critical document. The appraiser will complete Form 1004 (Uniform Residential Appraisal Report) but must also include Form 1007 (Single-Family Comparable Rent Schedule). This addendum confirms to the lender that the rent you're claiming is consistent with other "comps" in your specific neighborhood.

Proof of History vs. Projected Income: If you already own the home and are refinancing, we typically look for a 12-month history of rental income on your tax returns (Schedule E). However, if you've just finished the ADU, we can often use the projected income from the appraisal to qualify you immediately.

The "Legal" Factor: Zoning and Permits

Perhaps the biggest hurdle in ADU qualification is the Certificate of Occupancy. Lenders prioritize "Legal" units. This means the structure must comply with local zoning laws and have been built with the proper permits.

Permitted Units: These are the easiest to finance. They have a paper trail and meet all safety codes.

Unpermitted Units: If an ADU was built "off the books," it generally cannot be used for income qualification. In fact, an unpermitted ADU can sometimes hinder a loan if the appraiser notes it as a safety hazard or a violation of local zoning.

Legal Non-Conforming: These are units that were legal when built, but zoning laws have since changed ("Grandfathered"). Most lenders will accept these, provided the appraiser confirms the unit could be rebuilt if destroyed.

Ensuring your documentation is in order before the appraisal is ordered is the best way to prevent delays. If your unit meets these physical and legal benchmarks, you are well on your way to a successful qualification.

How Appraisers Calculate ADU Value and Market Rent

When you apply for a mortgage that includes ADU income, the appraiser plays a dual role: they must determine the fair market value of the entire property and establish a credible market rent for the accessory unit. For many lenders, this is the "make or break" moment of the loan process.

The "Comparable Sales" Challenge

The most difficult hurdle in an ADU appraisal is finding comparable sales. In many suburban markets, homes with legal, permitted ADUs are relatively rare.

The Rule of Three: Appraisers typically look for at least three closed sales of similar properties within the last 6–12 months.

Adjustments: If there aren't enough "ADU-to-ADU" matches, the appraiser must use homes without ADUs and apply a "contributory value" adjustment. This is where your E-E-A-T as a homeowner comes in—providing the appraiser with a list of nearby ADU properties or even a copy of your permits can help justify a higher valuation.

Market Rent Analysis: Form 1007 vs. 1025

To verify the income you plan to use for qualification, the lender will require a specific rental analysis:

Form 1007 (Single-Family Comparable Rent Schedule): This is the standard form used for 1-unit properties with an ADU. The appraiser identifies three local rentals that are similar to your ADU and determines the "Indicated Monthly Market Rent."

Form 1025 (Small Residential Income Property Report): Used if the property is technically a multi-unit (like a duplex) with an additional ADU.

The Appraisal Logic: The bank will generally use the lesser of the actual rent on your lease agreement or the market rent determined by the appraiser. This ensures the income is sustainable for the local market.

The 25% "Vacancy Factor" Explained

One of the most common surprises for borrowers is that they cannot use 100% of the rent to qualify. Lenders automatically apply a 25% deduction from the gross monthly rent.

Why the haircut? This 25% "vacancy and maintenance factor" accounts for times when the unit might be empty between tenants, as well as the costs of repairs, insurance, and property management.

The Math: If your ADU appraises for $2,000/month, the lender will only credit you with $1,500/month toward your income qualification ($2,000 x 0.75).

Understanding that the bank views your income through this conservative lens is vital. As your consultant, I help you run these numbers early so we know exactly how much "buying power" your ADU provides before the appraiser even sets foot on the property.

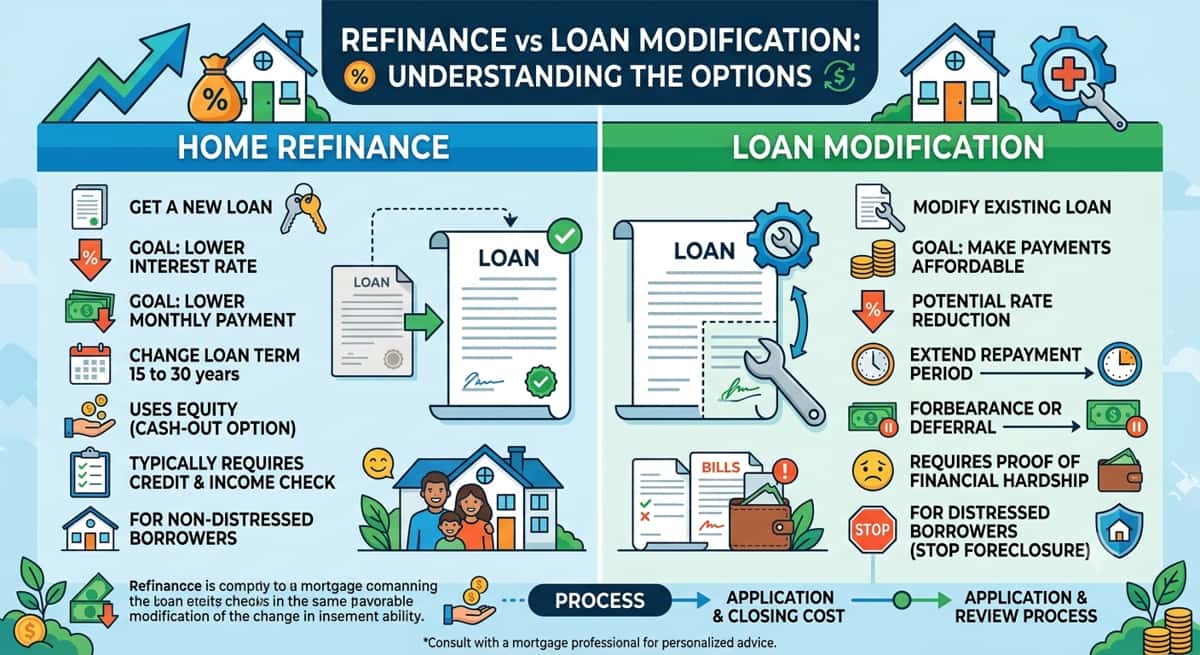

Refinancing with an ADU: Cash-Out vs. Rate-and-Term

If you already own a property with a secondary unit, or you are planning to build one, refinancing is a strategic way to optimize your monthly cash flow. As a mortgage expert, I often see homeowners overlook how an ADU can be the key to unlocking a lower interest rate or accessing significant capital.

Lowering Your DTI with ADU Income

In a standard rate-and-term refinance, the goal is usually to lower your interest rate or change your loan term (e.g., moving from a 30-year to a 15-year mortgage). However, if your income has fluctuated or your debt has increased since you first bought the home, you might find it difficult to meet the Debt-to-Income (DTI) requirements.

By including your ADU rental income in the application, we can effectively "raise" your qualifying income. This lowers your DTI ratio, which can result in better pricing on your interest rate or allow you to qualify for a loan that would otherwise be out of reach.

Financing the Build: Cash-Out Refi vs. Alternatives

For those who don't have an ADU yet but want to build one, a cash-out refinance is a popular path. This allows you to tap into your existing home equity to fund construction.

Cash-Out Refinance: You replace your current mortgage with a larger one, taking the difference in cash. This is ideal if current market rates are lower than your existing rate.

HELOCs vs. Construction-to-Perm: If you have a very low interest rate on your primary mortgage that you don't want to lose, a Home Equity Line of Credit (HELOC) might be better. However, for major builds, a Construction-to-Permanent loan can be advantageous because it allows you to borrow against the "as-completed" value of the home.

Consolidating Debt Using "Future Value"

One of the most powerful moves for a homeowner is using the "future value" or "subject-to" appraisal. When we refinance to build or renovate an ADU, the appraiser estimates what the home will be worth after the unit is finished.

This increased value often provides enough equity to not only fund the ADU construction but also to consolidate high-interest credit card debt or auto loans into one low-interest mortgage payment. By the time the project is finished, you have a higher property value, less high-interest debt, and a new stream of rental income to cover the mortgage—a triple win for your long-term wealth.

Overcoming Common Challenges: DTI and Credit Score

Even with a high-functioning ADU, the path to mortgage approval can have hurdles. As a consultant, my job is to help you navigate the "grey areas" of underwriting where many applications stall. Understanding the strict limits on debt and the necessity of liquid assets is the first step toward a successful closing.

Navigating the DTI Ceiling

In the world of conforming loans, the Debt-to-Income (DTI) ratio is king. For most conventional programs, the ceiling is generally 43% to 45%, though some Automated Underwriting Systems (AUS) may allow up to 50% if you have "compensating factors" like a high credit score or significant cash reserves.

If your ADU rental income is lower than anticipated, your DTI might spike above these limits. If the appraiser’s Form 1007 comes back with a lower market rent than your lease suggests, the lender must use the lower of the two figures. To mitigate this risk, I recommend keeping your other debts (credit cards, car payments) as low as possible during the application phase to provide a "buffer" for your DTI.

Reserve Requirements for Rental Properties

Lenders view properties with rental units as slightly higher risk than pure single-family homes. Consequently, they often require cash reserves. Reserves are liquid assets (savings, 401k, or brokerage accounts) that remain in your account after the down payment and closing costs are paid.

The Standard: Lenders typically look for 2 to 6 months of PITI (Principal, Interest, Taxes, and Insurance) payments in reserve.

Why it matters: If your total monthly mortgage is $3,000, the lender may want to see at least $6,000 to $18,000 sitting in your accounts.

What If the Appraisal Falls Short?

If the appraiser determines the ADU rent is significantly below your expectations, we have a few "Expert Level" options:

Rebuttal: We can provide the appraiser with better rental "comps" if they missed a nearby legal ADU rental.

Co-borrower: Adding a family member to the loan can help dilute the DTI ratio.

Down Payment Adjustment: If you are refinancing, a slight reduction in the loan amount can bring your DTI back into the "green zone."

Case Study: Turning a "No" Into a "Yes" With ADU Income

To illustrate the tangible impact of these guidelines, let’s look at a recent scenario involving a client in a high-cost housing market. "Mark" was a first-time homebuyer looking to purchase a property for $650,000 with a $500,000 loan amount. Mark had a solid job earning $6,500 per month, but with a $500 car payment and $300 in student loans, his Debt-to-Income (DTI) ratio was the primary obstacle.

Without any additional income, Mark’s projected monthly mortgage payment (including taxes and insurance) was approximately $3,600. When combined with his other debts, his DTI sat at 67% well above the maximum threshold for any conventional loan.

However, the property Mark wanted featured a legal, detached garage apartment. We ordered an appraisal with a Form 1007 Rental Addendum, which confirmed that the unit could command $1,600 per month in rent.

Applying the standard 25% vacancy factor, we were able to add $1,200 of effective income to Mark’s application. By increasing his qualifying monthly income from $6,500 to $7,700, his DTI dropped from a disqualifying 67% to a manageable 44%. This single adjustment allowed Mark to secure a conventional loan at a competitive rate. This case study demonstrates that for many Americans, the ADU isn't just an "extra" feature it is the very engine that makes homeownership a reality.

Conclusion & The "Next Steps" Roadmap

The landscape of American homeownership is shifting toward greater flexibility and density. In 2026, states like California and Washington are leading the way with landmark legislation such as California’s AB 1033, which allows for the separate sale of ADUs as condos, and AB 2533, which provides a streamlined path to legalize unpermitted units. For homeowners, these shifts represent a once-in-a-generation opportunity to transform a backyard into a primary engine for wealth and stability.

As federal lending guidelines from Fannie Mae and Freddie Mac continue to evolve, the ability to qualify for a mortgage using ADU rental income is becoming a standard tool for the modern borrower. Whether you are battling high interest rates or navigating a tight DTI ratio, your property’s secondary unit is often the missing piece of the puzzle.

Your Roadmap to Qualification:

Verify Legal Status: Check your local zoning or look into new "amnesty" programs for older, unpermitted units.

Estimate Market Rent: Research local "comps" to see what similar ADUs are earning in your neighborhood.

Consult a Professional: Get a pre-qualification analysis that factors in your specific ADU scenario.

Ready to see how much your ADU can increase your borrowing power? [Click here to schedule a personalized ADU Mortgage Strategy Session.]