For seasoned real estate investors and those looking to scale their portfolios, traditional financing often becomes a bottleneck. Conventional loans typically rely on Debt-to-Income (DTI) ratios, which measure your personal monthly debt against your gross monthly income. As your portfolio grows, your tax returns often fill with strategic write-offs which can ironically make it harder to qualify for new financing, despite your actual wealth.

Enter the Debt Service Coverage Ratio (DSCR) loan. This is a specialized mortgage product designed specifically for investment properties. Unlike a standard refinance, which scrutinizes your W-2s, pay stubs, and personal tax history, a DSCR loan focuses almost exclusively on the Rental Income generated by the property itself.

Essentially, a DSCR loan asks one primary question: Does the property’s cash flow cover its own debt? If the property generates enough revenue to pay the mortgage, taxes, insurance, and association fees, the lender views the investment as viable, regardless of the borrower’s personal employment status. This "asset-based" approach allows investors to bypass the rigorous income verification of Conventional Loans, making it an ideal path for entrepreneurs, freelancers, or retired investors seeking to tap into their Home Equity. By decoupling your personal financial profile from the property’s performance, DSCR refinancing offers a streamlined, business-minded alternative to traditional lending.

The Mechanics of DSCR Loan Qualification: How Lenders View Your Portfolio

To successfully refinance a rental property using a DSCR program, you must understand the lens through which a lender evaluates your "deal." In traditional lending, the borrower is the primary security; in DSCR lending, the property is the security. The qualification hinges on a single, vital metric: the ratio between the property’s income and its total debt obligations.

The DSCR Formula

Lenders calculate this ratio by dividing the property’s Net Operating Income (NOI)—or more commonly in residential DSCR, the Gross Monthly Rent—by the Principal, Interest, Taxes, Insurance (PITI) and any applicable Association Fees (HOA).

The standard mathematical formula used by mortgage consultants is:

DSCR =Gross Monthly Rent / Total Monthly Debt Service (PITIA)

Interpreting the Ratios: 1.0x to 1.5x

When a lender reviews your application, the resulting number tells them how much "cushion" exists in your cash flow. Here is how those tiers typically impact your qualification odds:

1.0x Ratio (The Break-Even Point): A 1.0x ratio means the property generates exactly enough income to cover the debt. While some lenders offer "No Ratio" or "Low Ratio" programs, qualifying at 1.0x often requires a higher credit score or a lower Loan-to-Value (LTV) ratio. It signals a tighter risk profile.

1.2x to 1.25x Ratio (The Standard Benchmark): This is the "sweet spot" for most DSCR lenders. A 1.25x ratio indicates that the property produces 25% more income than the debt requires. This provides a safety net for maintenance and vacancies, making you eligible for more competitive interest rates and higher leverage.

1.5x Ratio and Above (The High-Performance Tier): A ratio of 1.5x or higher represents a "cash cow" in the eyes of a lender. Properties with this level of coverage signal very low risk, often unlocking the most aggressive pricing and smoothest underwriting paths available in the market.

What Lenders Verify

To verify these numbers, lenders don't just take your word for it. They utilize a Form 1007 (Rent Schedule) during the appraisal process. This independent report confirms the "Fair Market Rent" for your specific area. If your actual lease is higher than the market average, the lender may use the lower of the two values to remain conservative. Understanding these mechanics allows you to position your portfolio strategically before beginning the refinance process.

Why Refinance Your Rental Property with a DSCR Loan Now?

The real estate market in the USA has seen significant shifts in property valuations over the last several years, leaving many investors sitting on a goldmine of untapped Home Equity. For a savvy landlord, equity is more than just a number on a balance sheet; it is stagnant capital that could be put to work. A DSCR Cash-out Refinance is the primary tool used to convert that equity into Liquidity without the red tape of traditional bank financing.

Fueling Portfolio Expansion

The most compelling reason to refinance now is to facilitate Portfolio Expansion. By leveraging the increased value of a single high-performing rental, you can extract cash to fund down payments on additional properties. Because DSCR loans do not limit the number of properties you can finance—unlike conventional loans which often cap at ten—they provide an infinite runway for growth. This allows you to scale your real estate empire based on the merits of your investments rather than the limitations of your personal debt-to-income ratio.

Strategic Financial Flexibility

Beyond expansion, refinancing into a DSCR loan provides a shield against personal financial volatility. Since the loan is tied to the property’s performance, it keeps your personal credit profile "cleaner" for non-investment needs. Additionally, in a fluctuating interest rate environment, securing a DSCR loan can help consolidate high-interest business debt or provide the necessary capital for property renovations that increase the rental value, further improving your future DSCR.

Expert Tip from a Mortgage Consultant: Many investors wait until they find their next deal before looking for cash. Instead, consider a "delayed financing" strategy or a proactive cash-out refinance. By unlocking your equity now, you position yourself as a "cash buyer" in the eyes of sellers. This liquidity gives you the power to negotiate lower purchase prices on new acquisitions, often saving you more than the cost of the refinance itself.

By focusing on the property’s ability to generate income, you bypass the friction of proving personal Capital Gains or income fluctuations, allowing you to move at the speed of the market.

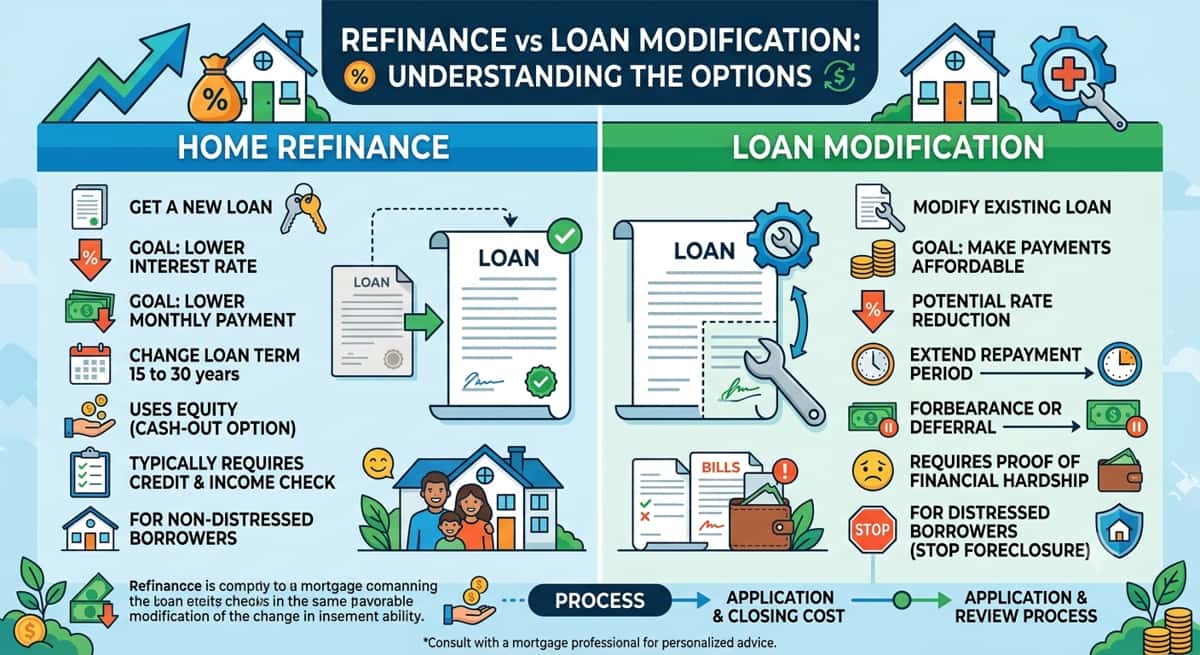

DSCR vs. Conventional Refinancing: Which is Right for You?

Choosing between a DSCR loan and a conventional refinance is often a decision between speed and scalability versus lower long-term costs. While both paths lead to refinancing your rental property, the "engine" under the hood of each loan is fundamentally different.

The Conventional Path (Fannie Mae & Freddie Mac)

Conventional loans are governed by Fannie Mae and Freddie Mac guidelines. These agencies require a deep dive into your personal financial life. Lenders will perform a comprehensive Employment Verification and require multiple years of Tax Returns to ensure your personal debt-to-income ratio (DTI) remains within strict limits. While this path usually offers the lowest interest rates, it can be a slow process with more "red tape."

The DSCR Path (The Investor’s Choice)

DSCR loans are "Non-Qualified Mortgages" (Non-QM), meaning they don't have to follow the rigid agency rules. They prioritize the asset’s performance. Because they bypass personal income hurdles, Closing Speeds are significantly faster—often 20–30 days compared to 45–60 days for a bank loan. Furthermore, DSCR loans allow you to close in the name of an LLC, protecting your personal credit and providing better liability shielding for your real estate business.

Comparison at a Glance

Feature | Conventional Refinance | DSCR Refinance |

Primary Approval Factor | Personal Income / DTI | Property Rental Income (DSCR) |

Income Documentation | Full (W2s, 1040s, Pay Stubs) | None (No Tax Returns Required) |

Closing Speed | Average 45–60 Days | Average 21–30 Days |

Ownership | Personal Name Only | Personal or LLC/Entity |

Loan Limits | Capped (Max 10 properties) | Unlimited Portfolio Scaling |

Interest Rates | Generally Lower | Generally 0.5% – 1.5% Higher |

Seasoning Requirement | Usually 12 Months for Cash-out | Often 0–6 Months |

The Bottom Line: If you have a high W-2 income and only own one or two rentals, a conventional loan is a cost-effective choice. However, if you are self-employed, have a complex tax profile, or are looking for rapid Portfolio Expansion, the DSCR loan is the superior tool for professional growth.

Step-by-Step: Navigating the DSCR Refinance Process in the USA

Navigating a DSCR refinance is notably more streamlined than a traditional mortgage, but it still requires a strategic approach to ensure you secure the highest Loan-to-Value (LTV) and the best possible terms. As your Mortgage Advisor, I guide you through this four-stage journey to move from application to funding.

Step 1: The Initial Portfolio Review

The process begins with an analysis of your property’s current performance. We calculate your estimated ratio by comparing your gross monthly rents against the anticipated mortgage payment (PITI). During this phase, we also confirm your Credit Score Requirements. While DSCR loans are flexible, a score of 680 or higher typically unlocks the most aggressive LTV tiers, sometimes allowing you to pull out up to 75% or 80% of the home's equity.

Step 2: The Appraisal and Form 1007

Once the application is submitted, the lender will order a specialized Appraisal. Unlike a standard home appraisal, this includes a Rent Schedule (Form 1007). This document is the linchpin of your loan; it is an independent data set that confirms the "Fair Market Rent" for your property. The lender will use the lower of your actual lease agreement or the 1007's market rent to finalize your DSCR calculation.

Step 3: Underwriting and Entity Verification

Because DSCR loans are "business-purpose" loans, the underwriting focus shifts away from your pay stubs and toward the property’s viability. If you are closing in an LLC, the lender will review your Operating Agreement and EIN. They will also verify "reserves"—typically 3 to 6 months of mortgage payments held in a liquid account—to ensure the property can handle a temporary vacancy.

Step 4: Clear to Close and Funding

Once the appraisal and title work are approved, you receive the "Clear to Close." At the closing table, you’ll sign the final documents, and the funds are typically disbursed within a few days. For those performing a cash-out refinance, this is the moment your equity is converted into liquid capital, ready to be reinvested into your next acquisition.

Crucial Considerations: Risks and Compliance in Rental Refinancing

While DSCR loans offer a powerful avenue for portfolio growth, they operate within a unique regulatory and risk framework. Because these are "business-purpose" loans, they are not subject to the same Federal Housing Finance Agency (FHFA) oversight as consumer mortgages. However, this freedom comes with specific responsibilities for the investor.

Understanding Prepayment Penalties

The most significant "hidden" cost in DSCR refinancing is the Prepayment Penalty. Since lenders do not collect the high upfront fees common in traditional banking, they protect their yield through a "step-down" penalty structure (e.g., a 5-4-3-2-1 or 3-2-1 schedule). If you sell or refinance the property within the first few years, you may owe a fee ranging from 1% to 5% of the loan balance.

Interest Rate Volatility

Interest Rates for DSCR products are typically 0.5% to 1.5% higher than conventional rates. It is vital to ensure your cash flow remains resilient even with these higher costs. A thin margin today could become a liability tomorrow if property taxes or insurance premiums increase.

The Role of Professional Guidance

In the world of YMYL (Your Money Your Life) financial decisions, a generic online calculator is no substitute for a licensed Mortgage Advisor. My role is to provide full Disclosure on all loan terms, ensuring that the debt structure aligns with your 5-year and 10-year wealth goals. Working with an expert helps you navigate the "fine print" of Non-QM lending, ensuring your liquidity doesn't come at the expense of your long-term financial health.

Expert Tip: Always ask for a "Par Rate" comparison. Sometimes, paying a slightly higher interest rate in exchange for a shorter (or zero) prepayment penalty is the smarter strategic move if you plan to flip or re-leverage the property in the near future.

Conclusion: Maximizing Your Real Estate ROI through Strategic Refinancing

Refinancing via a DSCR loan is more than a simple debt exchange; it is a sophisticated Investment Strategy designed to unlock the true potential of your rental portfolio. By shifting the focus from your personal income to the property’s performance, you gain the agility needed to thrive in a competitive market. Whether you are looking to lower your monthly obligations or harvest equity for your next acquisition, the right loan structure is the foundation of long-term Wealth Management.

The complexities of Non-QM lending require a nuanced approach that aligns with your specific financial trajectory. As an expert Mortgage Consultant, I specialize in helping investors navigate these specialized products to ensure every refinance serves their broader goals. Don't leave your portfolio's growth to chance—professional guidance can be the difference between a stagnant asset and a scalable empire.